So, you’re looking at the stock price for BRK B and wondering if you missed the boat or if the ship is just getting started. It’s a weird time for Berkshire Hathaway. We’re officially in the "post-Buffett" era as of January 1, 2026, and the market is acting... well, a little jittery. Honestly, it’s understandable. For sixty years, the strategy was "What would Warren do?" and now we’re finding out what Greg Abel actually will do.

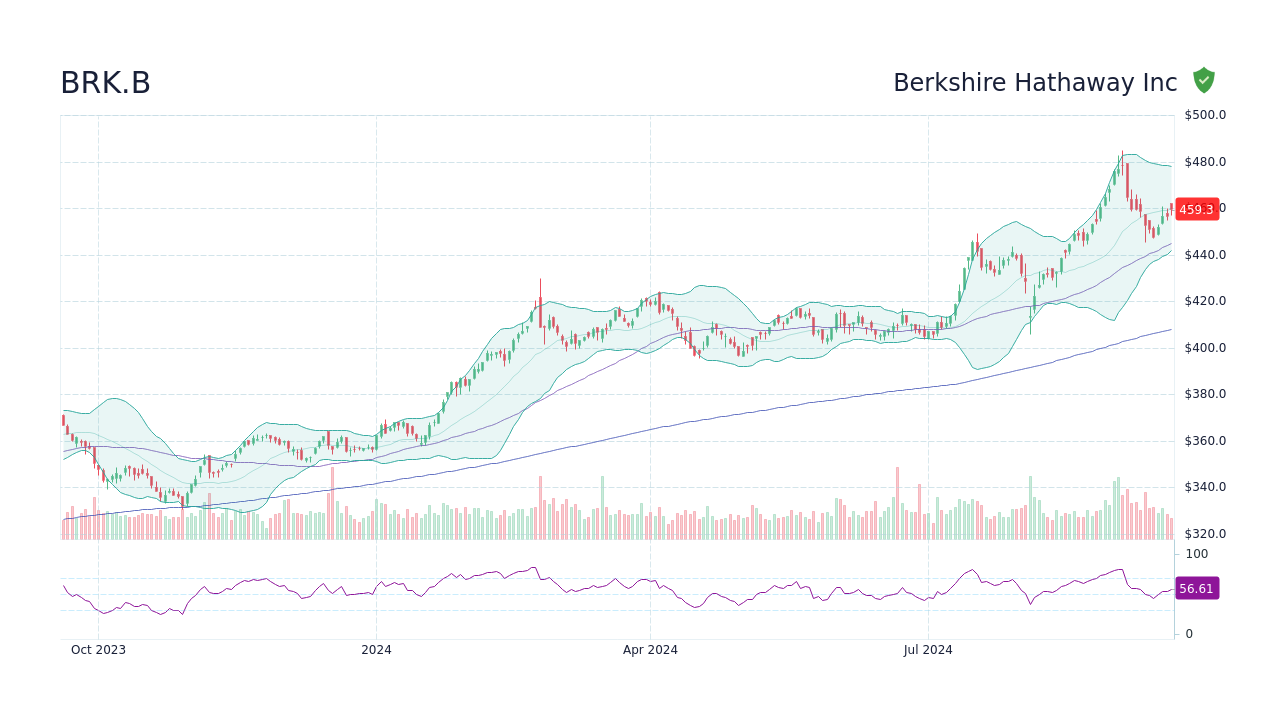

Right now, as of mid-January 2026, the stock price for BRK B is hovering around $491. It’s been a bit of a bumpy ride since the start of the year. We saw it flirt with $500 back in early January, but it’s pulled back about 1.2% recently. If you look at the 52-week high, we’re down from that peak of $542.

But here’s the thing: most people just look at that ticker and see a "boring" conglomerate. They see a price that doesn't move like a tech rocket. What they’re missing is the massive, almost terrifying, mountain of cash sitting in the basement in Omaha.

The $382 Billion Elephant in the Room

Berkshire is sitting on a record cash pile of roughly $381.7 billion. To put that in perspective, that’s more than the entire market cap of most companies in the S&P 500. For years, Buffett was waiting for an "elephant-sized" acquisition. He didn't find many. He spent the last few years being a net seller of stocks—basically trimming Apple and others because he thought valuations were getting too frothy.

Now, Greg Abel is the guy with the checkbook. He’s already made a move, closing the $9.7 billion acquisition of Occidental Petroleum’s chemical unit, OxyChem, just a couple of weeks ago on January 2nd. It’s a classic Berkshire move—industrial, cash-generative, and boring. But is it enough to move the needle on a trillion-dollar company? Probably not.

Why the Price Is Doing What It's Doing

Investors are currently weighing three big things that are tugging at the stock price for BRK B:

- The Succession "Discount": Even though Greg Abel has been the heir apparent for years, there’s still a psychological gap. Buffett was the "Oracle." Abel is a highly competent operations guy. The market is waiting to see if he has the same "capital allocation magic."

- The Dividend Debate: This is the big rumor for 2026. Buffett hated dividends; he wanted to reinvest every penny. But with $380 billion and a falling interest rate environment making those T-bills less attractive, pressure is mounting for Berkshire to finally start paying out. If a dividend is announced, expect the stock price for BRK B to react violently (likely to the upside).

- The Tech Shift: We saw Berkshire pick up $4.9 billion in Alphabet (Google) recently. It’s a signal. The old guard preferred railroads and insurance, but the new guard knows they can't ignore the AI-driven economy forever.

Is BRK.B Actually Undervalued?

If you talk to the analysts at Simply Wall St, they’ll tell you the stock is actually "on sale." Their Discounted Cash Flow (DCF) models suggest an intrinsic value closer to $785 per share. That would mean the current stock price for BRK B is about 36% undervalued.

Why the gap? It’s the "conglomerate discount." The market often struggles to value a company that owns everything from See's Candies to BNSF Railway and a massive slice of American Express.

💡 You might also like: Spread Charge on Credit Cards: Why Your Bank Is Taking More Than You Think

The Real Numbers (No Fluff)

- Current Price: ~$491

- 52-Week Range: $454.60 – $542.07

- P/E Ratio: ~15.9x (Compare that to the S&P 500 average which is often much higher).

- Operating Earnings: Surged 34% in the last reported quarter (Q3 2025) to $13.5 billion.

The insurance side of the business is still the heartbeat. Geico and the reinsurance arms are printing money because premiums have stayed high while catastrophe losses (thankfully) haven't spiked as badly as feared in late 2025. This "float"—the money they hold between collecting premiums and paying claims—is what funds the rest of the empire.

What Most People Get Wrong About the "B" Shares

I still hear people asking if they should buy the "A" shares instead. Unless you have about $735,000 (the current price for BRK.A) lying around under your mattress, the answer is no.

The Class B shares were literally created so regular people could own a piece of the pie. One Class A share is convertible into 1,500 Class B shares. The price stays in lockstep because of arbitrage. If the stock price for BRK B ever gets too cheap compared to the A shares, institutional investors just buy the B, convert, and profit. So don't worry—you aren't getting a "lesser" version of the company. You just have 1/1,500th of the economic interest and 1/10,000th of the voting rights.

The 2026 Outlook: What to Watch

If you’re holding BRK.B or thinking about jumping in, the next six months are going to be telling.

First, watch the 100-day Moving Average (SMA), which is sitting right around $496. Technically, the stock is trying to find its footing after a brief dip below its pivot point of $502. If it breaks back above $515, we could see a run toward the old highs. If it slips below $489, it might get ugly for a minute as short-term traders bail.

📖 Related: Why 12 weeks to 12 hours is changing how we think about efficiency

But you shouldn't be a short-term trader in Berkshire. That’s like buying a 100-year-old oak tree because you hope the leaves turn green by Thursday.

The Greg Abel Era Strategy

Abel’s base salary was recently bumped to $25 million. That’s a massive jump from Buffett’s legendary $100,000 salary, which has some purists grumbling. But Abel is running a more traditional corporate structure now. He’s already signaled that he’s going to keep the "hands-off" approach with subsidiary managers.

The real test is what he does with that $382 billion. If he lets it sit and rot while inflation eats it, the stock price for BRK B will stagnate. If he buys a massive tech company or initiates a 1% dividend, the narrative changes instantly.

Actionable Insights for Your Portfolio

Don't treat Berkshire like a tech stock. It’s a defensive play. It’s the stock you buy when you’re worried the rest of the market is crazy.

- Check your allocation: If you’re heavy on AI and "Magnificent Seven" stocks, BRK.B is a great hedge. It’s basically a private equity fund that trades on the NYSE.

- Watch the "Earnings Beat": Berkshire’s operating earnings are often more important than the "net earnings." Net earnings include the fluctuating value of their stock portfolio (like Apple), which makes the bottom line look like a heart monitor. Look at the operating earnings to see how the actual businesses—the railroads and energy plants—are doing.

- The "Buffett Premium": Acknowledge that a small part of the price was always "Warren magic." That's gone now. We’re trading on fundamentals, which, honestly, might make the stock more predictable.

The stock price for BRK B isn't going to make you a millionaire overnight. It’s not meant to. It’s meant to keep you a millionaire once you get there. If you can handle a little bit of post-succession volatility, the underlying value of the businesses Greg Abel just inherited is arguably stronger than it’s ever been.

Next Steps for Investors:

- Monitor the $490 support level: If the price holds here, it’s a strong signal that the "succession dip" is over.

- Review the Q4 2025 earnings report: Expected in February 2026, this will be the first full look at the company's health as the transition finalized.

- Calculate your "Look-Through" Earnings: Don't just look at the dividend Berkshire pays (zero). Look at the earnings the companies they own are making. That's your real return.

The era of the Oracle is over, but the era of the Machine is just starting.