It is early 2026, and the conversation around the stock price for bmy has taken a turn that few analysts predicted eighteen months ago. If you’ve been watching Bristol Myers Squibb (BMY), you know the drill. For years, the narrative was a slow-motion car crash—patents for blockbuster drugs were expiring, and the "patent cliff" felt more like a vertical drop into a ravine.

But look at the charts lately.

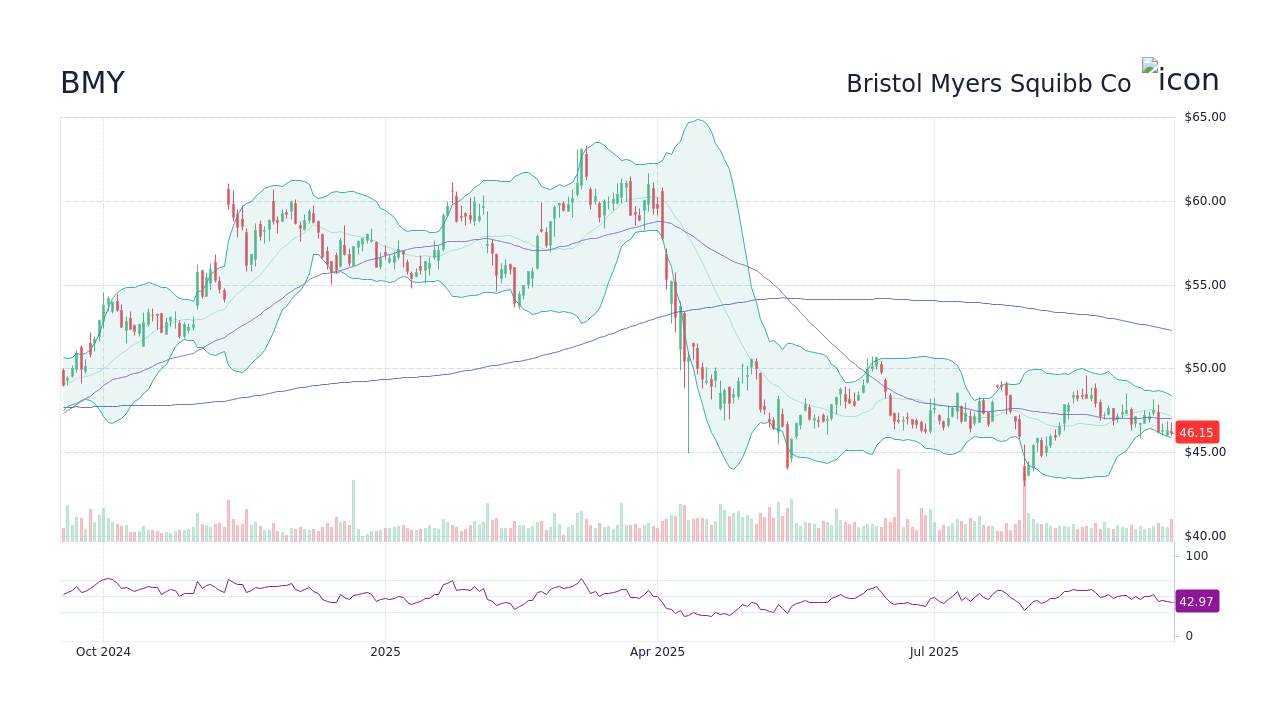

As of mid-January 2026, the stock has been hovering around the $55 to $57 range. Just this past Friday, January 16, it closed at $55.26. That might not sound like a moonshot if you bought in during the 2022 highs, but considering it bottomed out near $42.52 within the last 52 weeks, we are seeing a massive shift in sentiment. People are starting to wonder if the worst is actually over.

The 2026 Reality Check

Honestly, the reason the stock price for bmy is showing signs of life isn't because the problems went away. The "Big Three"—Eliquis, Opdivo, and Revlimid—are still facing or approaching generic competition. That hasn't changed. What has changed is the Growth Portfolio.

In the most recent reports from late 2025, the growth side of the house finally started to carry its own weight. We're talking about a 18% jump in revenue from the new stuff, hitting $6.9 billion. When the "new" part of a company starts making up more than half of the total revenue, the "old" part's decline doesn't hurt quite as much. It’s basic math, but the market took its sweet time believing it.

📖 Related: Influence: The Psychology of Persuasion Book and Why It Still Actually Works

What is actually moving the needle?

- Cobenfy (KarXT): This is the schizophrenia drug they got from the $14 billion Karuna deal. It’s huge. Not just for the patients, but for the stock. Early 2025 launch data showed doctors are actually prescribing it, and 2026 is the year we see if it can become a multi-billion dollar pillar.

- The Opdivo "Refresh": They didn't just let Opdivo die. The approval of the subcutaneous version—basically a shot instead of an IV drip—is a brilliant tactical move to keep patients and extend the life of the franchise.

- The Dividend Factor: You can't talk about BMY without the 4.5% yield. In a market where people are getting twitchy about tech valuations, a safe, growing dividend is like a warm blanket.

Why Analysts are Raising Price Targets

Recently, Scotiabank and Leerink Partners both pushed their targets up to $60. UBS went even further, hitting $65. Why? Because they think the market has been "pricing in" a disaster that might not be as bad as feared.

There's this thing called "multiple expansion." Basically, it's when investors decide a company isn't a "dying business" anymore and is instead a "recovery story." If BMY moves from trading at 9x earnings to 11x or 12x, the stock price for bmy moves up even if earnings stay flat. It's all about perception.

But it's not all sunshine. We have to be real about the risks. The Inflation Reduction Act (IRA) is hitting Eliquis pricing hard starting this year. That is a direct hit to the bottom line. Plus, BMY has a debt-to-equity ratio of about 2.39, which is... let's just say it's something they need to keep an eye on. They’ve been spending a lot of money to buy growth, and now they have to pay for it.

The J.P. Morgan Healthcare Conference Impact

At the big San Francisco conference earlier this month, CEO Christopher Boerner was basically on a mission to convince everyone that the 2030 patent cliff is manageable. He’s promising 12 major trial readouts this year. That’s a lot of "binary events." If those trials go well, $60 looks cheap. If they fail, like some of the Milvexian trials did, we could be heading back to the $40s.

👉 See also: How to make a living selling on eBay: What actually works in 2026

Breaking Down the Numbers

Let's look at what the "smart money" is seeing right now:

- EPS Projections: Analysts are looking for an adjusted EPS around $6.50 for the full year 2025/2026.

- Support Levels: The 200-day moving average is sitting around $48.13. As long as we stay above that, the "trend is your friend."

- Volume: We're seeing roughly 13 million shares trade a day. That’s healthy liquidity. It means big institutional players are moving in and out, not just retail traders.

It's kinda funny how the narrative shifts. A year ago, BMY was the "value trap" no one wanted to touch. Now, it's the "defensive yield play" that everyone is adding to their "recession-proof" list.

Actionable Insights for Investors

If you're looking at the stock price for bmy as a potential entry point, don't just look at the price. Look at the calendar.

Watch the February 5th Earnings Call. This is the big one. They will give the official 2026 guidance. If they forecast better-than-expected margins despite the Eliquis price cuts, the stock could break through that $58 resistance level.

✨ Don't miss: How Much Followers on TikTok to Get Paid: What Really Matters in 2026

Check the Pipeline Readouts. Keep a Google Alert on names like "admilparant" and "milvexian." These are the drugs that will replace the lost revenue. A "win" in these Phase III trials is worth more than any dividend hike.

Mind the P/E Ratio. Right now it's around 18.6 based on current GAAP earnings. That sounds high for pharma, but if you look at non-GAAP (which strips out the one-time costs of buying those smaller companies), it's much lower. Make sure you're looking at the right numbers before you pull the trigger.

The bottom line is that Bristol Myers is currently a bet on management's ability to execute a very difficult transition. They aren't just a pill company anymore; they are trying to become a cell therapy and neuropsychiatry powerhouse. It’s risky, but for the first time in a long time, the market is actually giving them a chance.

Next Steps for You:

Check your current portfolio's exposure to the healthcare sector and see if a 4.5% yield fits your risk profile. You might also want to compare BMY's 2026 guidance against competitors like Pfizer or Merck to see who is handling the patent cliff more effectively.