You’ve probably heard the rumors that the government is coming for your retirement check. It’s a common fear. You work forty years, pay into the system, and then—poof—the taxman wants a second helping. But honestly, the "tax-free" dream isn't as rare as you might think. Most people are shocked to find out that as of 2026, the vast majority of the United States actually leaves your Social Security check alone.

There are currently 42 states without social security tax (plus the District of Columbia).

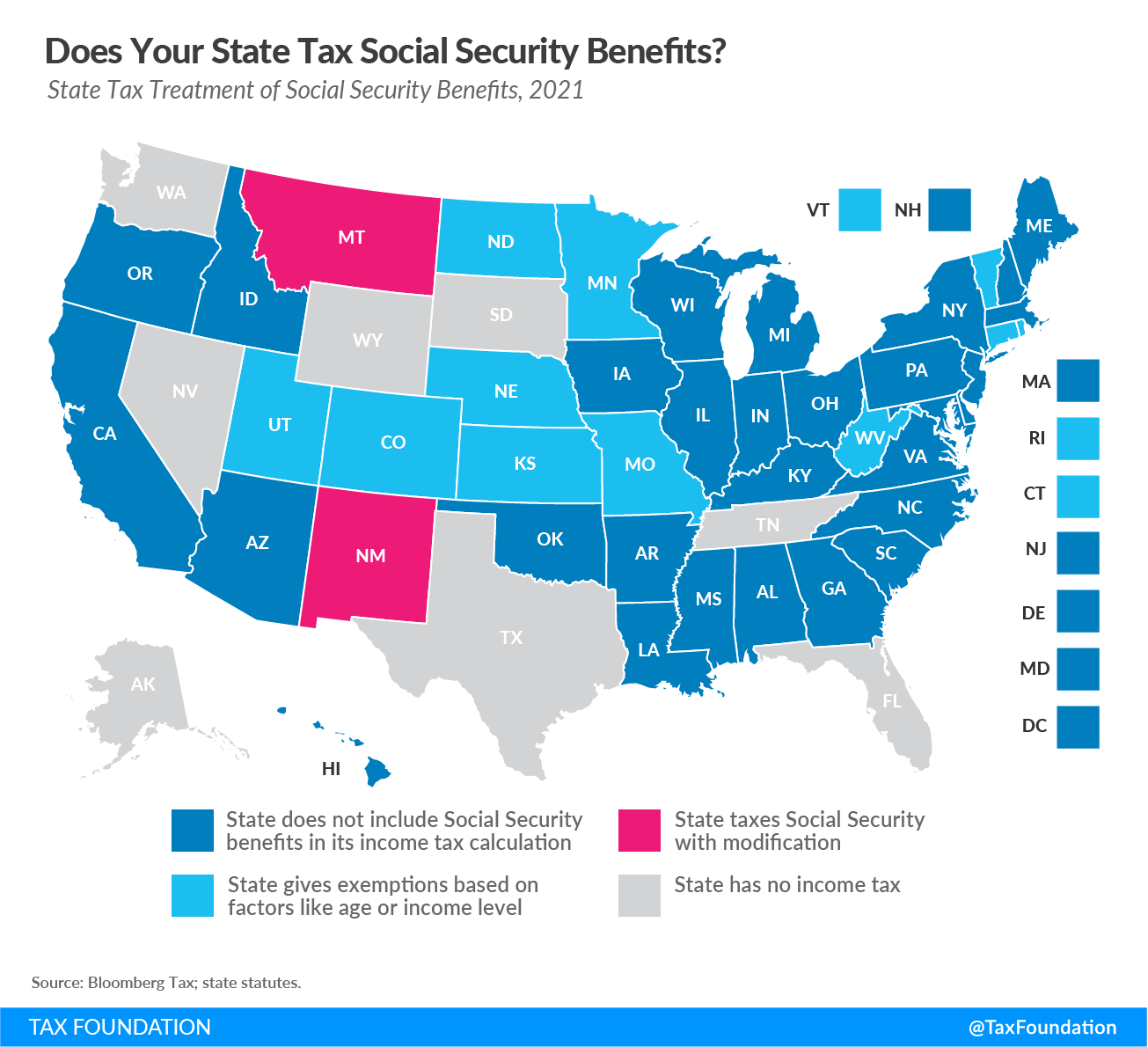

That’s the good news. The bad news? If you live in one of the "Elite Eight" states that still take a cut, you could be losing thousands of dollars a year just because of your zip code. It's kinda wild how much your location dictates your net worth in retirement. Let’s get into the weeds of who is actually taxing you and where you can hide your hard-earned benefits.

👉 See also: Amazon stock today price: Why the Jan 14 dip is a massive distractor

The Shrinking List of States That Still Tax You

It used to be a lot worse. A few years ago, double-digit states were dipping into Social Security pots. But politicians realized that taxing grandma isn't a great way to get re-elected. In 2026, West Virginia officially crossed the finish line of its multi-year phase-out. Now, Mountaineers can keep every cent of their benefits at the state level.

They joined the ranks of Kansas, Missouri, and Nebraska, all of which recently axed their benefit taxes. It’s a massive trend.

If you're still in one of these eight states, you might want to look at the math:

- Colorado: They’re actually pretty decent about it if you’re older. If you are 65 or plus, you can deduct all your taxable Social Security. If you're 55 to 64? Not so much. You only get a $20,000 deduction.

- Connecticut: This one is strictly for the "wealthy" (by their definition). If you're single and make under $75,000, or married making under $100,000, you're safe. Cross that line, and they start nibbling.

- Minnesota: Often cited as the least tax-friendly for retirees. While they have a "subtraction" rule that helps middle-income folks, higher earners get hit hard here.

- Montana: They follow the federal lead mostly. If the IRS says it's taxable, Montana usually agrees, though they have a small $5,500 subtraction for those over 65.

- New Mexico: They have some of the most generous thresholds. Single filers can make up to $100,000 before the state asks for a portion of that Social Security check.

- Rhode Island: You basically have to reach Full Retirement Age (FRA) to get the exemption, and even then, there are income caps.

- Utah: They use a tax credit system. It’s complicated. You have to fill out a worksheet to see if you actually owe.

- Vermont: Like Minnesota, they have a "sliding scale." If you make over $60,000 as a single person, expect to pay up.

Why 2026 Is a Weird Year for Your Wallet

The rules just changed again. The Social Security Administration announced a 2.8% Cost-of-Living Adjustment (COLA) for 2026. While that's extra cash in your pocket, it can actually backfire.

It’s called "bracket creep."

If your benefits go up by $100 a month, that might be enough to push your total income over the thresholds in states like Connecticut or Vermont. Suddenly, you aren't just paying tax on that extra $100—you're paying tax on a huge chunk of your entire benefit because you crossed an arbitrary line.

Also, the federal wage base for those still working increased to $184,500. If you're a high-earner "working retiree," your payroll taxes just went up, even if your state doesn't tax the benefits themselves.

The "No Income Tax" Trap

Don't just pack your bags for Florida yet.

Yes, Florida, Texas, Nevada, and Washington are famous for being states without social security tax because they don't have any state income tax at all. Zero. Zilch. It sounds like a paradise. But states have to pay for roads and schools somehow.

In Texas, you might not pay income tax, but the property taxes can be absolutely brutal. I’ve seen retirees move from New York to Austin thinking they’d save a fortune, only to find their property tax bill doubled. Washington state doesn't have income tax, but they have some of the highest sales taxes in the country.

You’ve gotta look at the "Total Tax Burden."

Take a state like Pennsylvania. They do have an income tax, but they are incredibly generous to seniors. They don't tax Social Security, and they don't tax most private or public pensions. It’s often cheaper to live there than in a "no tax" state where the sales tax at the grocery store eats your lunch.

Dealing With the Federal Elephant in the Room

Even if you live in a state without social security tax, the IRS is still lurking. This is what trips people up the most. The federal government uses something called "provisional income" to decide if they want a cut.

The formula is basically: Adjusted Gross Income + Tax-Exempt Interest + 50% of your Social Security benefits.

- If that number is over $25,000 (single) or $32,000 (joint), up to 50% of your benefits are taxable.

- If it’s over $34,000 (single) or $44,000 (joint), up to 85% is taxable.

These thresholds haven't been adjusted for inflation since the 1980s. It’s essentially a stealth tax that hits more people every single year as inflation drives up nominal income.

Actionable Steps to Protect Your Check

If you’re worried about losing your benefits to taxes, you aren't stuck.

First, look into a Roth Conversion before you retire. Since Roth IRA withdrawals aren't counted as "provisional income," they don't trigger the tax on your Social Security. It’s a way to lower your "on-paper" income while keeping your actual spending power high.

Second, if you live in one of those eight taxing states, check if you’re near the "cliff." If making $1,000 less in a side hustle saves you $3,000 in state taxes because you stayed under the threshold, it’s a no-brainer.

Third, consider your timing. If you’re in a state that is phasing out the tax (like West Virginia just finished doing), waiting a year to claim or move could save you a bundle.

Ultimately, being in one of the states without social security tax is a great head start, but it's only one piece of the puzzle. You have to look at the property tax, the sales tax, and how the federal IRS rules play with your specific income mix.

Your 2026 Tax Checklist:

- Check your 2026 COLA: That 2.8% bump is nice, but calculate if it pushes you over your state's tax-free threshold.

- Verify your state's "subtraction" rules: States like Colorado and Minnesota have specific forms to claim your exemption—don't assume it's automatic.

- Review your "Provisional Income": Even in a tax-free state, your federal bill depends on this specific calculation.

- Audit your property tax: If moving to a "no-tax" state, compare the property tax rate of your current home vs. your target destination.

Moving for taxes is a big deal. Make sure the math actually works before you call the movers.