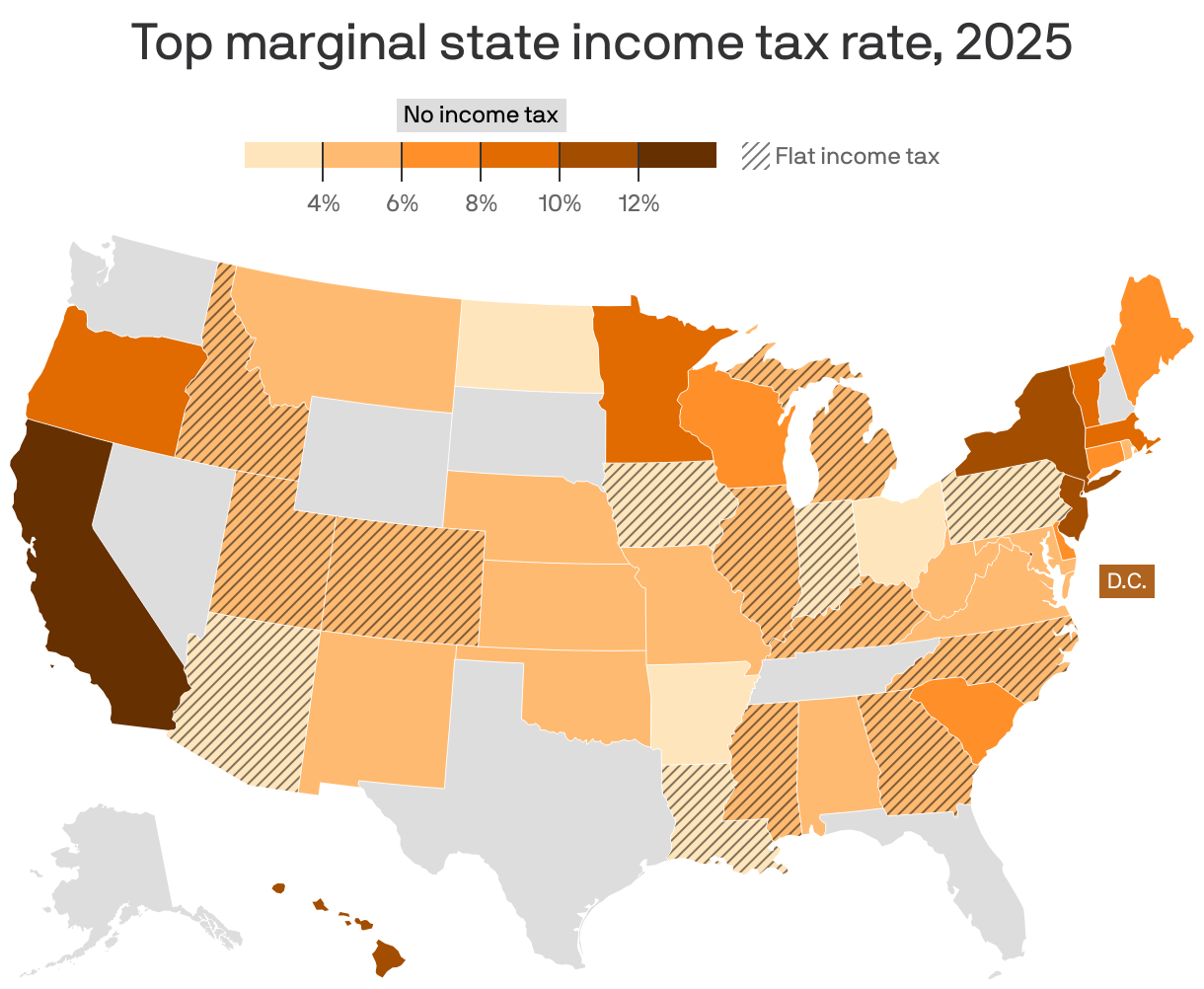

You’re staring at your paycheck. The gross amount looks great, almost heroic. Then you see the "Net" and it feels like someone mugged your bank account. If you live in a place like California or New York, that feeling is a daily reality. But if you're in Florida or Texas? Different story. Looking at a state income tax by state map isn't just a fun geography exercise—it’s actually a look at how much of your life you’re giving away to the government just for the "privilege" of standing on their dirt.

Taxes are weirdly personal.

Some people think the states with no income tax are paradise. Others argue you get what you pay for. Honestly, the truth is buried somewhere under a pile of property tax bills and sales tax receipts. It's not just about that one big number on your return.

The "Big Zero" club and why it's complicated

Right now, there are eight states that don't take a single dime from your paycheck. Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming. Wyoming is basically the holy grail for tax avoidance if you can handle the wind. New Hampshire is the ninth member, sorta. They don't tax earned income, but they’ve been phasing out their tax on interest and dividends, aiming to hit total zero by 2025 or 2026.

It sounds amazing. Zero. Zilch.

But here is the catch. These states still need to pave the roads. They still need to pay cops and fix schools. So, they get their pound of flesh elsewhere. Take Texas. You don't pay state income tax, but have you seen their property taxes? They’re brutal. You might save $5,000 on income tax and then hand $7,000 to the county assessor. Washington State doesn’t tax your salary, but they have some of the highest sales taxes in the country. You’re paying for it every time you buy a toothbrush or a toaster.

Alaska is the true outlier. They have no income tax and no state sales tax. They literally pay you to live there via the Permanent Fund Dividend. Of course, you have to survive an Alaskan winter, which is a tax of a different kind.

What a state income tax by state map tells us about the coast

If you look at a map of the US colored by tax rates, the coasts are usually glowing bright red. California is the heavyweight champion here. Their top bracket hits $13.3%$. That is wild. If you’re a high earner in San Francisco, between federal, state, and local taxes, you’re basically a 50/50 partner with the government.

New York isn’t far behind. New Jersey loves a good tax hike too.

👉 See also: Why It Worked for Me by Colin Powell is Still the Best Leadership Manual You Aren’t Reading

The interesting trend lately isn't just the high rates, but the "millionaire taxes." States like Massachusetts recently passed the "Fair Share Amendment," adding a $4%$ surcharge on income over $1$ million. It sounds like it only hits the ultra-rich, but it’s causing a massive migration of wealth. People aren't just moving for the weather anymore. They’re moving for the math.

Then you have the flat-tax rebels.

States like Arizona, Utah, and North Carolina have moved or are moving toward a flat tax system. Instead of the "progressive" brackets where you pay more as you earn more, everyone pays the same percentage. Usually around $3%$ to $5%$. It’s simple. It’s predictable. And it's driving some states absolutely crazy because they can't compete with the simplicity.

The hidden "double whammy" in the Midwest

Don't sleep on the Midwest. Places like Ohio and Pennsylvania have relatively low state rates, but they let their cities and school districts tack on their own income taxes. You might look at Pennsylvania’s flat rate of $3.07%$ and think, "Hey, that’s a bargain!" Then you move to Philadelphia and realize the city takes another $3.75%$ roughly for the Wage Tax.

Suddenly, your "low tax" state is more expensive than some "high tax" ones.

It’s a shell game. States like Illinois are struggling with massive pension debt, which keeps their rates high despite a flat-tax structure. They tried to change to a graduated system a few years ago, but voters shot it down. People are skeptical. They know that once you give the government a "progressive" ladder, they just keep adding rungs.

How to actually use this information

If you're planning a move, don't just look at the top-line percentage. You have to look at the "Effective Tax Rate." This is what you actually pay after deductions and credits.

- The Retirement Factor: If you’re retiring, look at states like Pennsylvania or Mississippi. They don’t tax most retirement income, including 401(k)s or private pensions. Even though PA has that local tax issue, for a senior, it’s actually a tax haven.

- The Remote Work Trap: This is the big one for 2026. If you live in a low-tax state but work for a company in New York, New York might still try to tax you. It’s called the "Convenience of the Employer" rule. It’s a legal mess that is currently being fought in courts across the country.

- The Cost of Living Offset: If you move from NYC to Florida to save $10%$ in taxes, but your insurance premiums triple and your commute doubles, did you actually win? Probably not.

The state income tax by state map is changing every year. We are seeing a "race to the bottom" in the South and Midwest as states compete for residents. It’s a buyer’s market for taxpayers right now, provided you’re willing to pack a U-Haul.

Actionable Next Steps

Stop looking at the gross number on your job offer. Before you sign anything or buy a house in a new state, run your specific salary through a multi-state tax calculator like the ones provided by SmartAsset or the Tax Foundation. Specifically, check the local "occupational" or "city" taxes that don't show up on the state-level maps.

Next, call a local insurance agent in the new state. If you're moving to a "no-tax" state like Florida or Texas, the spike in homeowners and auto insurance might completely wipe out your tax savings. You need the "all-in" cost of living, not just the IRS version.

Finally, if you're a business owner or high-net-worth individual, look into "statutory residency" rules. Just spending winters in Nevada isn't enough to dodge California taxes. You usually need to prove you've actually moved your life—voter registration, driver's license, and where your "near and dear" items (like family photos or pets) live. The "tax man" is getting way more aggressive about checking your cell phone pings to see where you actually sleep at night.