Tax season usually feels like a giant headache. Most people just click through their software, hoping the "standard deduction" covers everything. But if you’re 65 or older and filing as a single person, you’re in a unique spot. You get a "bonus." IRS rules actually allow for an additional amount on top of the regular deduction, and honestly, it’s one of the few times the tax code works in your favor.

Let’s get into the weeds.

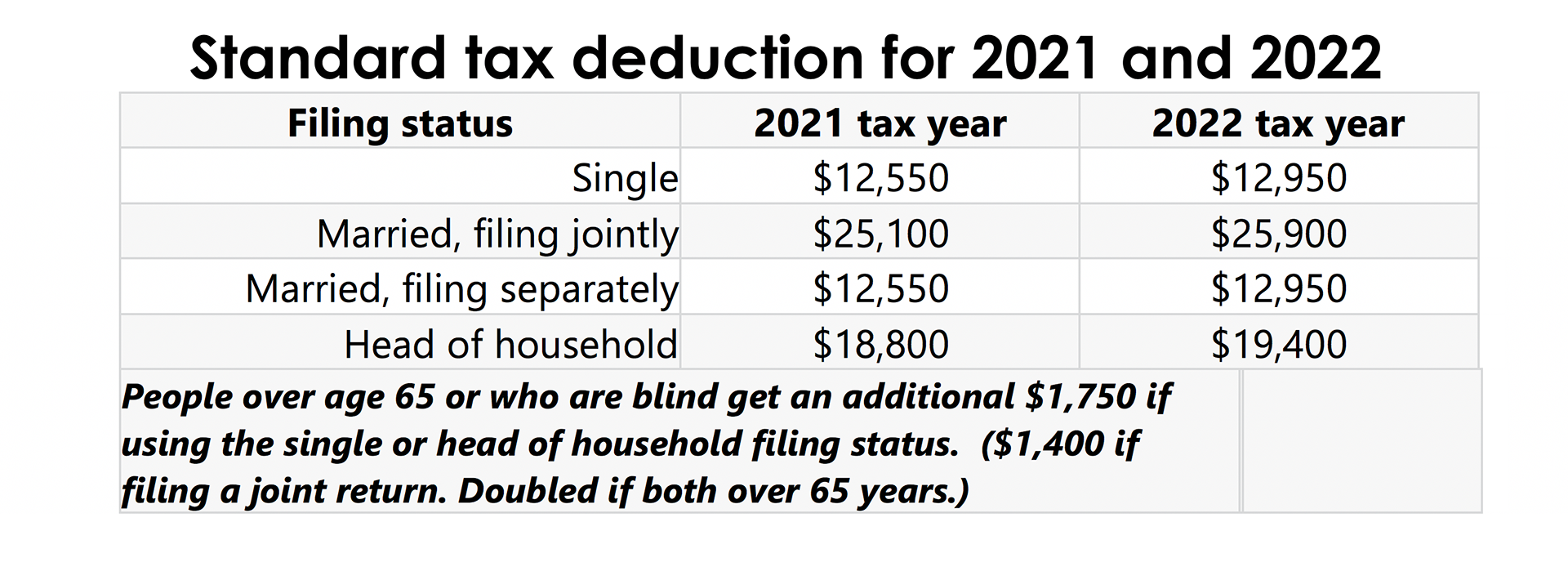

Most taxpayers know the standard deduction is a fixed dollar amount that reduces the income you’re taxed on. It’s the "floor." If your itemized deductions—like mortgage interest or massive medical bills—don't beat that floor, you take the standard. It’s easier. It’s faster. But for seniors, the floor is higher.

How the Standard Deduction Single Over 65 Actually Works

The IRS doesn’t just give you one number. They give you a base, then they add a "bump" for your age. For the 2025 tax year (the ones you file in early 2026), the standard deduction for a single filer is $15,000. However, if you are 65 or older by December 31, 2025, you get an additional $2,000.

That brings your total standard deduction single over 65 to $17,000.

Think about that. That is $17,000 of your income that the federal government cannot touch. If you earned $20,000 in taxable income, you’re only actually paying taxes on $3,000. It’s a huge deal.

Wait, there’s a catch about your birthday. The IRS has this weird rule. If you were born on January 1, 1961, the IRS considers you to be 65 at the end of 2025. You technically turn 65 on the day before your birthday in their eyes. It’s a small quirk, but if you’re a New Year’s baby, it means you get the higher deduction a full year earlier than you might expect.

What if you’re blind?

The IRS groups age and blindness together for these "additional" deductions. If you are single, over 65, and legally blind, you get two additions. You’d take the base $15,000, add $2,000 for age, and add another $2,000 for blindness. Suddenly, your deduction is $19,000.

Most people miss this. They check the "65 or older" box but forget that "legally blind" has a specific IRS definition. You don’t have to be totally without sight. If your field of vision is no more than 20 degrees, or if your vision is 20/200 or less in your better eye with glasses, you qualify. You just need a statement from your eye doctor. Keep it in your records. Don't mail it with the return, but have it ready if they ask.

📖 Related: Dollar to Lira Syrian Explained: Why Everything Just Changed in 2026

Why This Number Changes Every Year

Inflation.

The IRS adjusts these numbers annually to keep up with the cost of living. Back in 2024, the base was $14,600 and the senior bump was $1,950. It’s creeping up. This is why looking at old tax forms is dangerous. You’ll leave money on the table.

For 2026 filings (tax year 2025), that $17,000 total for a single senior is the benchmark. If you’re a Head of Household—maybe you’re single but you support a grandchild or a sibling—your base is higher ($22,500), but your "over 65" bump is the same $2,000.

It’s about simplicity versus savings.

When Should You Stop Taking the Standard Deduction?

This is where people get confused. They think because they have the "senior bump," they must take the standard deduction. Not true.

You should itemize if your specific expenses are higher than $17,000. For a single senior, the most common "itemization killers" are:

- Medical Expenses: This is the big one. If you had a major surgery, long-term care costs, or expensive dental work, and those costs exceed 7.5% of your Adjusted Gross Income (AGI), you might be better off itemizing.

- State and Local Taxes (SALT): You can deduct up to $10,000 of your state income tax and property taxes combined.

- Charitable Donations: If you’re incredibly generous to your church or a nonprofit, and those gifts plus your medical/taxes beat $17,000, stop taking the standard deduction.

But honestly? Most single seniors find the $17,000 threshold hard to beat. Especially since the 2017 Tax Cuts and Jobs Act nearly doubled the standard deduction, itemizing has become a rarity. Roughly 90% of taxpayers now just take the "easy" route.

The "Standard Deduction Single Over 65" and Social Security

Does this deduction affect your Social Security? Sorta.

✨ Don't miss: Daymond John Worth: Why Most Net Worth Sites Get It Wrong

It doesn't change how much you receive from the Social Security Administration, but it definitely changes how much of that money you keep. If your total income (including half of your Social Security) stays below certain thresholds, and then you apply that $17,000 deduction, you might end up owing $0 in federal taxes.

Many seniors live in fear of the "tax torpedo." This is when an extra dollar of income (like a 401k withdrawal) suddenly makes more of their Social Security taxable. Having a larger standard deduction acts as a buffer. It pushes that "torpedo" further away.

Real World Example: Meet Martha

Martha is 72. She lives alone in a small condo in Florida. Her income looks like this:

- Social Security: $24,000

- Part-time job at a library: $12,000

- Small pension: $5,000

Her total income is $41,000. But for tax purposes, not all of that Social Security is counted. After some math, let’s say her AGI is $30,000.

Because Martha uses the standard deduction single over 65, she subtracts $17,000 right off the top. Now her taxable income is $13,000. She’s only paying taxes on that $13,000, mostly at the 10% bracket.

If Martha were 64, her deduction would only be $15,000. Being 72 saves her the tax on an extra $2,000 of income. That’s a few hundred dollars back in her pocket for groceries or the electric bill. It matters.

Common Mistakes to Avoid

- Forgetting the box: On Form 1040, there are checkboxes for "Age/Blindness." If you use software like TurboTax or H&R Block, it usually asks your birthdate and does it for you. But if you’re doing a paper return or using a local "tax guy" who is rushing, make sure that box is checked.

- The "65" timing: You don't have to be 65 for the whole year. If your 65th birthday is December 31, you get the full extra deduction for that entire tax year.

- Filing Status Errors: If you are a widow or widower, you might qualify for "Qualifying Surviving Spouse" status for two years after your spouse’s death, which gives you an even higher deduction. Don’t just file as "Single" out of habit if you recently lost a spouse.

Beyond the Federal Return

Don't forget that your state might do things differently.

States like Georgia, South Carolina, and Colorado have very generous retirement income exclusions. While the federal standard deduction single over 65 helps with your US taxes, you should check your state's "Senior Homestead Exemption" or "Retirement Income Tax Credit."

Often, the federal deduction is just the beginning of the savings.

Actionable Next Steps

To make sure you aren't leaving money on the table this year, follow this checklist:

- Verify your 2025 AGI: Gather your 1099s from Social Security, pensions, and any part-time work.

- Total your medical out-of-pocket costs: If they are more than $10,000 or $12,000, you might want to see if itemizing is worth it. If they are just a few thousand, stick to the standard deduction.

- Check the Age Box: Ensure your tax preparer or software has flagged you as 65+. Confirm the deduction total is at least $17,000 (for 2025 tax year).

- Look into "Qualified Charitable Distributions" (QCDs): If you are over 70.5 and take the standard deduction, you can't deduct your church tithe. But, you can send money directly from your IRA to the charity. This lowers your income before you even take the standard deduction. It’s a "double win."

- Review State Benefits: Visit your state's Department of Revenue website to see if they offer an additional senior deduction on top of the federal one. Many states "decouple" from federal rules and offer their own perks for retirees.

Taking the standard deduction isn't "lazy"—for most single seniors, it's the smartest financial move. Just make sure you're taking the correct version of it. Get every dollar that $2,000 age bump allows. You earned it.