Checking your brokerage account lately feels a bit like riding a roller coaster that only goes up, doesn't it? Well, mostly. If you’re looking at the s&p 500 rate of return ytd, you’re seeing the heartbeat of the American economy in real-time. It’s the number everyone obsessively refreshes. It's the benchmark that fund managers sweat over and retirees bank on.

But here’s the thing. That percentage you see on Yahoo Finance or CNBC isn’t just a static digit. It’s a messy, loud, and incredibly complex reflection of everything from AI hype to the Federal Reserve's mood swings.

Honestly, it’s easy to get lost in the green.

As of mid-January 2026, the market is grappling with some serious baggage from the previous year. We aren't just looking at price appreciation. We're looking at a market that is trying to figure out if the massive gains of 2024 and 2025 were a fluke or the new normal. If you've been sitting on the sidelines, that "year-to-date" figure might look intimidating. If you're all in, it might look like a reason to buy a boat.

Let's get into the weeds of what is actually driving these returns.

Why the s&p 500 rate of return ytd feels different this year

Market cycles are weird.

Usually, when we talk about the S&P 500, we’re talking about a market-cap-weighted index. That’s a fancy way of saying the big guys—Apple, Microsoft, Nvidia, Alphabet—pull all the weight. If Nvidia has a bad Tuesday, the whole index catches a cold.

This year, the s&p 500 rate of return ytd has been heavily influenced by the "Second Wave" of AI implementation. It’s no longer just about who makes the chips. Now, the market is rewarding companies that are actually showing profit from using that tech. We’re talking about logistics firms using autonomous routing and healthcare giants slashing drug discovery times.

It’s not just tech, though.

✨ Don't miss: Rough Tax Return Calculator: How to Estimate Your Refund Without Losing Your Mind

Energy has been a wild card. With geopolitical tensions in the Middle East and shifting trade routes in the Indo-Pacific, oil prices have been swinging like a pendulum. That fluctuates the energy sector's contribution to your total return. You might see a 2% jump one week because of a supply chain disruption and a 3% drop the next because of a new trade agreement. It’s exhausting to watch, but it’s the reality of the index.

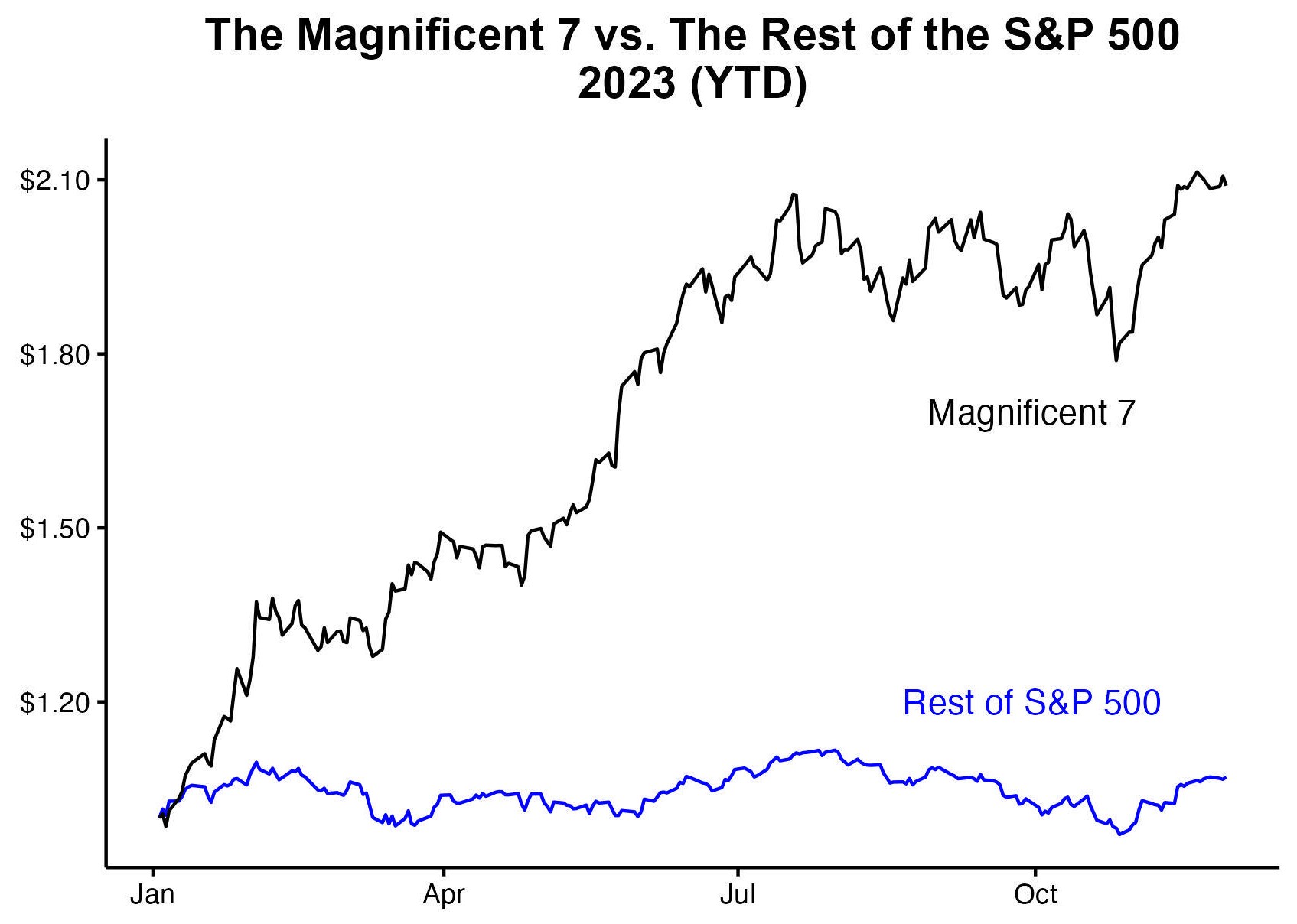

The "Magnificent" weight problem

You've probably heard of the "Magnificent Seven." In previous years, these few stocks were responsible for nearly the entire return of the index.

Is that still true?

Sorta. We are seeing a bit more "breadth" now. That’s investor-speak for "more companies are participating in the rally." When the s&p 500 rate of return ytd is driven by 400 companies instead of just seven, the rally is much healthier. It means if one tech giant gets hit with an antitrust lawsuit, the whole index doesn't crumble.

I was looking at some data from Howard Silverblatt, a senior index analyst at S&P Dow Jones Indices. He often points out how concentration risk is the invisible boogeyman of passive investing. If you own an S&P 500 index fund, you aren't as diversified as you think. You’re basically betting on Silicon Valley with a little bit of banking and retail sprinkled on top.

Inflation and the Fed's shadow

Interest rates are the gravity of the financial world.

When rates are high, stocks struggle to jump. When rates are low, they fly. Right now, the Federal Reserve is playing a delicate game of "will they or won't they" with rate cuts. Every time Jerome Powell speaks, the s&p 500 rate of return ytd jitters.

If the Fed signals a "hawkish" stance—meaning they want to keep rates high to fight inflation—investors get spooked. Money moves out of "risky" stocks and into "safe" bonds. But if they hint at a "dovish" turn, the S&P 500 usually takes off.

🔗 Read more: Replacement Walk In Cooler Doors: What Most People Get Wrong About Efficiency

We also have to talk about earnings season. Companies don't just need to make money; they need to beat expectations. A company could report a billion dollars in profit, but if the "whisper number" on Wall Street was 1.1 billion, the stock price might tank. This psychological game is what creates the daily volatility in your YTD returns.

Total Return vs. Price Return: Don't miss the dividends

Most people look at the price chart. That’s a mistake.

The s&p 500 rate of return ytd is actually composed of two things:

- Price Appreciation: The stock price going from $100 to $110.

- Dividends: The cash the companies pay you just for owning the stock.

Over long periods, dividends make up a massive chunk of your total wealth. Even if the price of the S&P 500 is flat for a few months, those dividend payouts are still trickling in. If you aren't reinvesting them, you’re leaving money on the table. Think of it like a snowball. A small snowball at the top of a hill (your initial investment) needs that extra moisture (dividends) to really grow into an avalanche by the time it hits the bottom.

How to use this data without going crazy

Watching the market daily is a great way to develop an ulcer.

The YTD return is a snapshot. It’s a "you are here" marker on a map that stretches for decades. If you’re 25, the return so far in 2026 matters very little. If you’re 64 and retiring in six months, it matters a lot.

One thing people get wrong is "timing the market." They see the s&p 500 rate of return ytd hitting a new high and think, "I'll wait for a dip." Then the dip never comes, or it comes after another 10% gain. You end up buying back in at a higher price than where you started.

It’s frustrating.

💡 You might also like: Share Market Today Closed: Why the Benchmarks Slipped and What You Should Do Now

Instead, most pros suggest Dollar Cost Averaging (DCA). You put in the same amount of money every month regardless of whether the YTD return is up 20% or down 10%. You buy more shares when they're cheap and fewer when they're expensive. It takes the emotion out of it.

Common misconceptions about index returns

- The S&P 500 is the "whole market": It isn't. It's 500 of the largest U.S. companies. It misses small-cap companies, which often grow much faster (but are riskier).

- A "good" year is 10%: People say 10% is the average. But the S&P rarely actually returns 10% in a single year. It usually returns +25% or -12%. "Average" is just the middle point of a very bumpy ride.

- YTD reflects the economy: Not exactly. The stock market is forward-looking. The s&p 500 rate of return ytd is reflecting what investors think will happen in six to nine months, not what is happening at the grocery store today.

Real-world impact: What now?

So, the numbers are what they are. What do you actually do with this information?

First, check your asset allocation. If the S&P 500 has been on a tear, your portfolio might now be 80% stocks when you intended it to be 60%. This is called "style drift." When the market eventually corrects—and it always does—you'll get hit harder than you planned.

Second, look at your fees. If you're paying a 1% management fee to a broker just to track the S&P 500, you're getting robbed. There are ETFs (Exchange Traded Funds) like VOO or SPY that do the same thing for a fraction of a percent.

Lastly, keep an eye on the "Real Return." If the s&p 500 rate of return ytd is 5% but inflation is 4%, you’ve only really gained 1% in purchasing power. That’s the number that actually determines if you can afford that beach house in twenty years.

Actionable steps for your portfolio

Don't just stare at the chart. Take these steps to ensure your strategy aligns with the current market reality.

- Rebalance your winners: If tech has ballooned to half your portfolio because of the recent YTD surge, sell some and move it into "boring" sectors like utilities or consumer staples. It feels counterintuitive to sell what's winning, but it's how you lock in gains.

- Audit your expense ratios: Ensure your S&P 500 exposure is costing you less than 0.05% annually. Anything more is unnecessary in 2026.

- Automate your contributions: Set up your bank to transfer funds to your brokerage the day after payday. This removes the temptation to "wait for a better entry point" based on the YTD fluctuations.

- Ignore the "noise" of daily headlines: Focus on the quarterly earnings reports of the top 10 holdings in the index. These are the true engines of the s&p 500 rate of return ytd. If their fundamentals are solid, the short-term price swings are just distractions.

Investing is a marathon, not a sprint. The YTD return is just one mile marker. Treat it as a data point, not a prophecy. By staying disciplined and focusing on long-term growth rather than short-term spikes, you position yourself to actually benefit from the compounding power of the American economy.

Keep your head down, keep your costs low, and stay invested. That’s the only "secret" that actually works.

Next Steps for Investors:

Review your current brokerage statement and identify the "Top 10 Holdings" in your primary index fund. Check the "Total Return" (including dividends) rather than just the price change to see the true performance of your capital since January 1st. If your portfolio has become overweight in a specific sector due to recent gains, schedule a rebalancing trade for the upcoming month to manage your risk exposure effectively.