It's 2026. You just opened your first paycheck of the year, and if you’re like most of us, you probably noticed the numbers look a little different. Maybe the "net pay" is a tiny bit lower than you expected. You aren’t imagining it. While the headline tax percentages usually stay the same, the actual amount of money the government can take from you often changes every single January.

Honestly, taxes are confusing. Most people just see "FICA" on their stub and ignore it. But understanding the social security tax rate is the only way to make sure your payroll department—or your own quarterly estimates—aren't messing up your bank account.

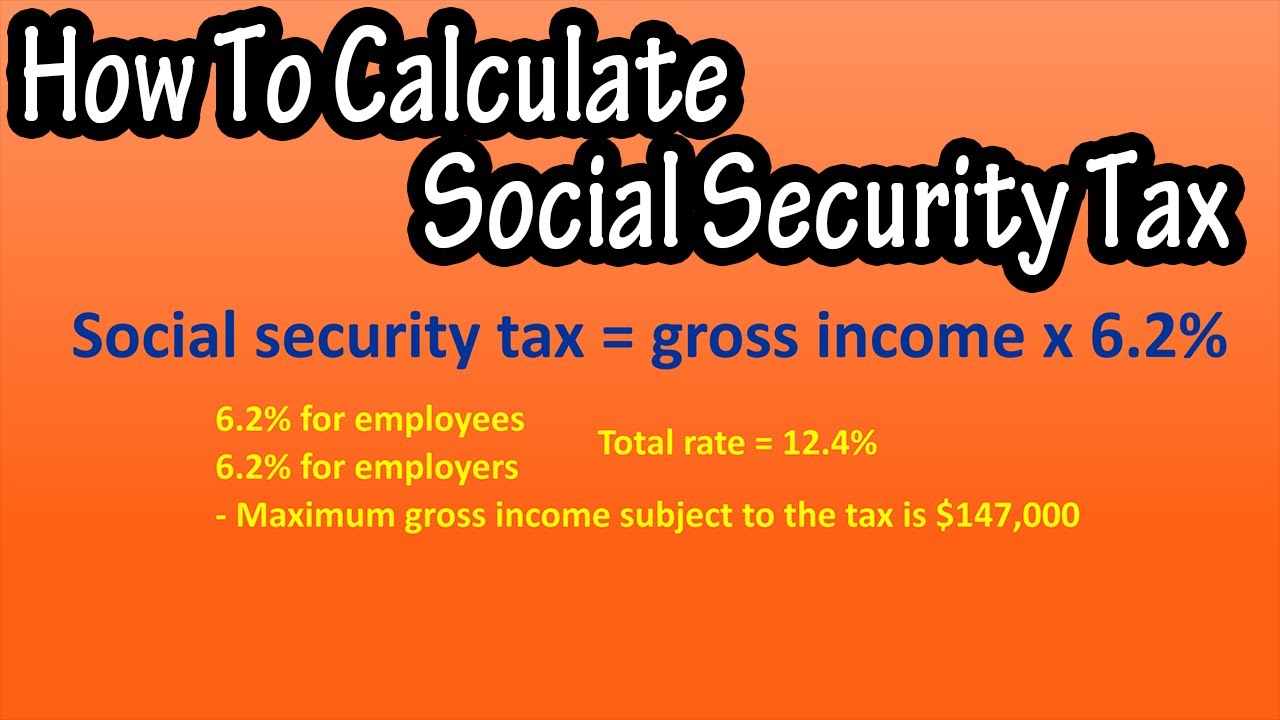

The Raw Numbers: What is the Social Security Tax Rate?

Let’s get the math out of the way first. For 2026, the Social Security tax rate is 6.2% for employees.

If you work for a boss, they also pay 6.2% on your behalf. That’s a total of 12.4% going into the system to fund retirement and disability benefits for about 75 million people. You don't see the employer's half, but it's there, quietly adding up behind the scenes.

But here is the catch. You don't pay that 6.2% on every single dollar you make. There is a "cap" or a ceiling.

The 2026 Wage Base Limit

The Social Security Administration (SSA) just bumped the taxable maximum. In 2026, the Social Security wage base is $184,500.

If you earn $200,000 this year, you only pay Social Security tax on the first $184,500. Everything above that is "Social Security tax-free." This is a pretty significant jump from the 2025 limit, which was $176,100. Because the wage base went up by $8,400, high earners will pay about $520.80 more in taxes this year than they did last year.

It's a weird system. It basically means the more you make above that cap, the lower your effective Social Security tax rate becomes.

The "Self-Employed" Shock

If you’re a freelancer, a consultant, or you run a small shop, the news is a bit tougher. You are both the employer and the employee.

You pay the whole 12.4%.

✨ Don't miss: 800 Pesos in US Dollars: Why the Math Might Surprise You

When you add in the Medicare portion (which is 2.9% for the self-employed), you’re looking at a 15.3% self-employment tax. It hurts. Trust me. You’ll be calculating this on Schedule SE when you file your 1040.

One small silver lining? The IRS lets you deduct the "employer" half of that tax (7.65%) from your gross income when calculating your income tax. It doesn't lower the self-employment tax itself, but it does lower your overall income tax bill.

Wait, What About Medicare?

People often lump Social Security and Medicare together because they both fall under FICA (Federal Insurance Contributions Act). But they behave very differently.

- Social Security: Has a cap ($184,500). Once you hit it, the tax stops for the year.

- Medicare: Has no cap. You pay 1.45% on every dollar, forever.

- The Surcharge: If you earn more than $200,000 (or $250,000 for married couples), there is an Additional Medicare Tax of 0.9%.

So, while your Social Security tax might stop once you're a high earner, your Medicare tax actually gets more expensive.

Why Does the Rate Keep Changing?

Technically, the 6.2% rate hasn't moved in decades. What changes is the "wage base."

The SSA uses something called the National Average Wage Index to decide how much of your income is "fair game" for taxing. As average wages across the country go up, the cap goes up. It’s a bit of a treadmill. If your salary stays the same while the cap goes up, you might actually see your take-home pay dip slightly because you're being taxed on a larger slice of your pie.

What Most People Get Wrong

A common myth is that you stop paying all payroll taxes once you hit the cap. Nope. You only stop paying the 6.2% portion.

Another big misconception is that this money is sitting in a personal "vault" with your name on it. It isn't. The 12.4% collected from your check today is immediately sent out to pay for your grandmother’s (or your neighbor’s) current retirement benefits. The system is "pay-as-you-go."

Real-World Example: The "Tax Holiday"

Let’s say you’re a software engineer making $220,000.

👉 See also: Converting Guineas to US Dollars: Why This Dead Currency Still Controls High-End Auctions

Throughout the year, your employer takes out that 6.2%. But around late October or November, you’ll likely hit that $184,500 mark. Suddenly, your November and December paychecks will look a few hundred dollars bigger.

Workers call this a "Social Security tax holiday." It feels like a raise, but it’s just the tax hitting its legal limit for the year. Just don't get too used to it—it resets every January 1st.

Actionable Steps for 2026

If you want to stay ahead of the IRS and keep your finances clean, here is what you need to do right now:

- Check your first 2026 paystub. Make sure the Social Security withholding is exactly 6.2% of your gross pay (before 401k or health insurance deductions). If it's not, talk to HR.

- Adjust your 401(k) contributions. If you are a high earner and expect to hit the cap late in the year, you might want to front-load or back-load your retirement savings to balance out your cash flow.

- Freelancers: Update your "Tax Bucket." If you were setting aside 15% of your income for taxes in 2025, you need to account for the new 2026 wage base. Move 25-30% of every check into a separate savings account so you aren't scrambling on April 15th.

- Watch the "Additional Medicare Tax." If you have two jobs or a working spouse, your employers might not know you’ve collectively crossed the $250,000 threshold. You might need to ask for extra withholding (Form W-4) to avoid a surprise bill at the end of the year.

The social security tax rate is a fixed percentage, but its impact on your life depends entirely on how much you earn and how you earn it. Staying on top of these annual shifts is the difference between a boring tax season and a very expensive surprise.