Tax season is usually a headache. Most of us just click through the software, hope the "refund" number goes up, and dread the "amount you owe" line. For a lot of folks, the standard deduction is the easiest route. But honestly, if you own a home, live in a high-tax state, or had a rough year with medical bills, you're probably leaving money on the table. That’s where Schedule A comes in. It’s the form you use to itemize. It’s the way you tell the IRS, "Actually, my life costs a lot more than your basic deduction allows for."

Don't let the technical jargon scare you off.

Back in 2017, the Tax Cuts and Jobs Act (TCJA) basically nuked the popularity of itemizing. By nearly doubling the standard deduction, it made it so about 90% of taxpayers didn't need to touch Schedule A anymore. But for that remaining 10%? It’s a goldmine. We’re talking about real people like Sarah, a hypothetical freelancer in California, who pays a fortune in state taxes and mortgage interest. For her, the standard deduction is a joke compared to what she can claim on Schedule A.

What is Schedule A and Why Should You Care?

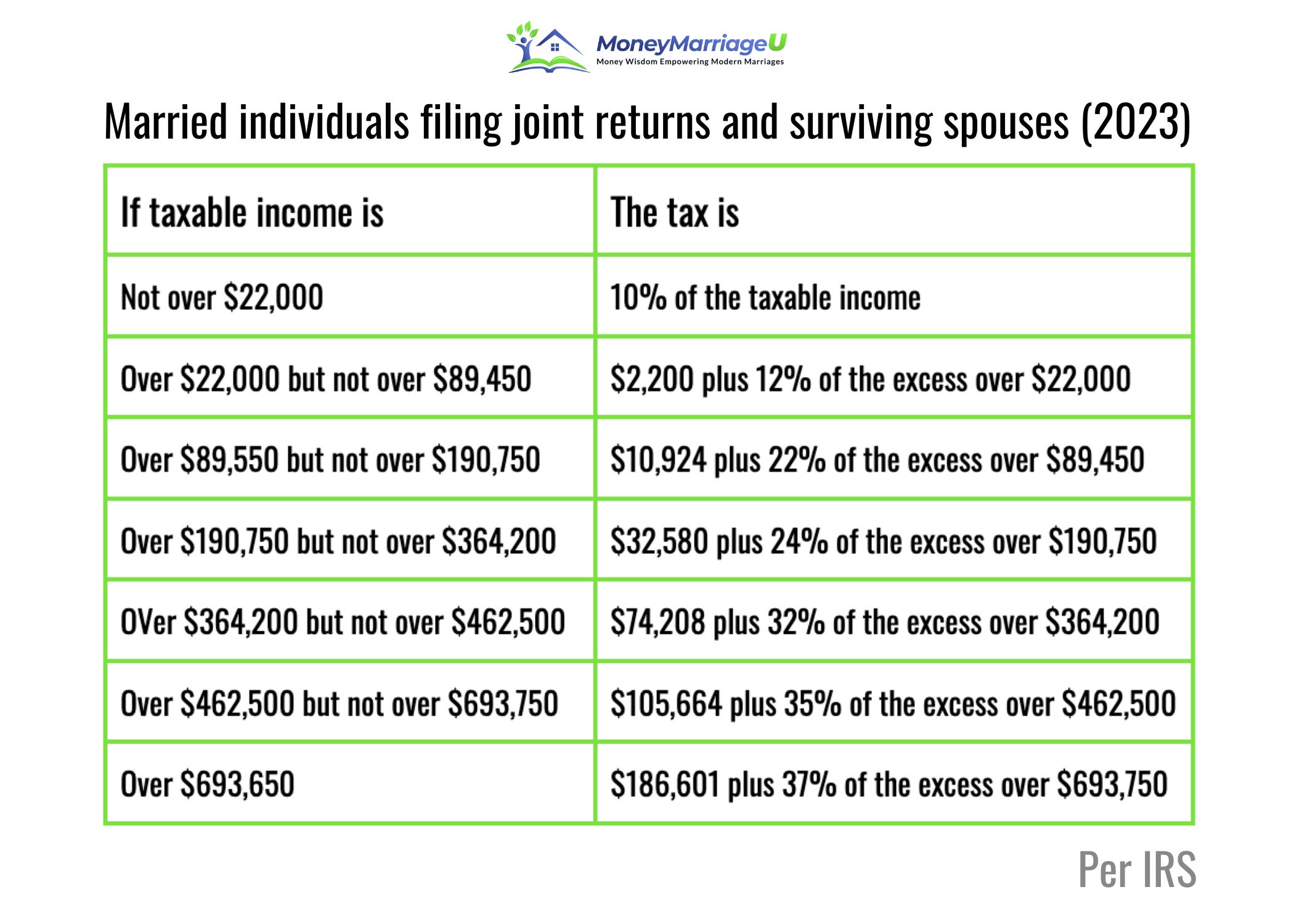

Basically, Schedule A is an optional form. You don't have to use it. You use it when the sum of your individual deductible expenses—stuff like mortgage interest, state and local taxes, and charity—is higher than the standard deduction the IRS gives everyone. For the 2024 tax year, the standard deduction for single filers is $14,600. For married couples filing jointly, it’s $29,200. If your list of expenses is $30,000 and you’re married, you’d be crazy not to itemize.

The goal is simple. Lower your taxable income.

The lower that number goes, the less you pay in tax. It’s not cheating; it’s just following the rules the government wrote. But the rules have "ceilings" and "floors." Some expenses you can only deduct if they’re huge, while others are capped at a specific dollar amount regardless of how much you actually spent. This is where people get tripped up. They think they can deduct every penny. You can't.

The Medical Expense Floor

Medical bills are the biggest "maybe" on the form. To even list them on Schedule A, your unreimbursed medical and dental expenses have to exceed 7.5% of your Adjusted Gross Income (AGI). This is what tax pros call a "floor."

If you make $100,000, that floor is $7,500. If you spent $8,000 on a surgery that insurance didn't cover, you don't get an $8,000 deduction. You get $500. It’s frustrating. But if you had a year with major dental work, fertility treatments, or long-term care, those numbers add up fast. You can even include things like travel costs for medical care or the cost of glasses and hearing aids. Honestly, most people miss the travel part—miles driven for doctor visits count at 21 cents per mile for 2024.

The SALT Cap: A Major Pain Point

State and Local Taxes, or SALT. This is the part of Schedule A that gets the most political heat. You’re allowed to deduct what you paid in state and local income taxes (or sales taxes, but usually not both) plus your property taxes.

There’s a massive catch.

The TCJA capped this deduction at $10,000. It doesn't matter if you live in New Jersey and pay $15,000 in property taxes and another $8,000 in state income tax. You get $10,000. Period. For people in high-tax states, this was a gut punch. Before 2018, you could deduct the whole thing. Now, it’s a bottleneck. However, if you're a homeowner in a state like Florida or Texas with no state income tax, you’ll likely choose to deduct your sales tax instead. The IRS has a handy table that estimates how much sales tax you probably paid based on your income, so you don't have to save every single receipt from the grocery store.

Interest You Paid

Mortgage interest is usually the heavy lifter on Schedule A. For most homeowners, this is the number that pushes them over the standard deduction threshold. But there are limits here too. If you took out your mortgage after December 15, 2017, you can only deduct interest on up to $750,000 of mortgage debt. If your house was bought before that date, you’re likely grandfathered in at the old $1 million limit.

🔗 Read more: Why that image of a coke bottle is the most studied design in history

What about home equity loans?

Kinda tricky. You can only deduct interest on a home equity loan if the money was used to "buy, build, or substantially improve" the home that secures the loan. If you used that money to pay off credit cards or buy a boat, that interest isn't deductible on your Schedule A. The IRS is pretty strict about tracing where that money went.

Charitable Contributions and the "Bunching" Strategy

Giving to charity is great for the soul, and it’s pretty good for your taxes too. You can generally deduct cash contributions up to 60% of your AGI. If you're giving away old clothes or furniture to Goodwill, you deduct the "fair market value," which is basically what a thrift store would sell it for, not what you paid for it three years ago at the mall.

Since the standard deduction is so high now, a lot of savvy taxpayers use a strategy called "bunching."

Instead of giving $5,000 to your favorite non-profit every year, you give $10,000 every other year. By "bunching" two years of donations into one, you’re more likely to exceed the standard deduction threshold in that "on" year, maximizing your Schedule A benefits. In the "off" year, you just take the standard deduction. It’s a smart way to play the system legally. Just make sure you get receipts. If you give more than $250, you need a written acknowledgment from the charity. No receipt, no deduction. Simple as that.

Casualties, Thefts, and the "Fine Print"

You might see a section for casualty and theft losses. Don't get too excited. Unless your loss was caused by a federally declared disaster, you probably can't claim it. This was another big change from the 2017 tax law. If someone stole your laptop out of your car, it’s a bummer, but it’s not a tax deduction anymore. If your house was destroyed by a wildfire in an area the President declared a disaster zone? Then yes, you’re looking at a potential deduction on your Schedule A, but only for the amount not covered by insurance and only after it exceeds 10% of your AGI.

Common Myths and Mistakes

People often think they can deduct their commuting costs or their work clothes. Unless you’re a clown who needs a specific costume or a nurse who needs scrubs that aren't wearable outside of work, the answer is usually no.

Unreimbursed employee expenses used to be a thing on Schedule A, but they’re gone for most people until at least 2026. Only certain professionals—like armed forces reservists, qualified performing artists, and fee-basis state or local government officials—can still claim these. If you're a regular W-2 employee, you can't deduct your home office or your new monitors on Schedule A. That’s a common point of confusion.

📖 Related: Euro Sun Mining Stock Explained: Why the Rovina Valley Project is a Binary Bet in 2026

Another big one? Investment interest. You can deduct interest paid on money borrowed to buy investment property (like stocks on margin), but only up to the amount of your net investment income. It’s complex. It’s messy. But for high-net-worth individuals, it matters.

Does It Actually Make Sense to Itemize?

Determining if you should use Schedule A isn't just about adding up numbers. It’s about timing. If you’re close to the threshold, you might want to "pull forward" some expenses. Maybe you pay your January mortgage payment in late December. Or you move up a planned surgery to the current tax year.

It’s all about the math.

- Gather your 1098 forms (mortgage interest).

- Total your state and local taxes (up to that $10k cap).

- Look at your medical out-of-pocket costs.

- Add up your charitable receipts.

If that total is $14,600 (single) or $29,200 (joint), you’re at the break-even point. Anything above that is a win. Even if you only beat the standard deduction by $100, it might be worth it depending on your tax bracket. If you’re in the 24% bracket, that $100 deduction saves you $24. Not life-changing, but better in your pocket than the government's.

Actionable Steps for Your Next Tax Return

If you think you might be an itemizer, stop throwing away receipts.

- Create a "Tax Box": Physical or digital, it doesn't matter. Just put everything in one place.

- Track Your Miles: Use an app or a simple log for medical and charitable driving.

- Check Your Property Tax Bill: Sometimes people forget the "ad valorem" portion of their car registration—that's often deductible as a personal property tax.

- Review Your Giving: Look at your bank statements for those small $10 or $20 monthly donations to Patreon or local shelters; they add up.

- Talk to a Pro: If your situation involves a home office (for business owners), multiple properties, or huge medical bills, a CPA can find things you’ll miss.

Itemizing isn't for everyone anymore. But for those who fit the profile, Schedule A remains a vital tool for keeping more of what you earn. Taxes are high enough; don't pay more than you legally have to. Keep it simple, keep it documented, and do the math before you just click "Standard Deduction" and move on.

👉 See also: Converting SAR to USD: Why the Rate Never Seems to Change

Practical Resource Checklist

- IRS Interactive Tax Assistant: How do I file Schedule A?

- IRS Publication 502: Medical and Dental Expenses

- IRS Publication 526: Charitable Contributions

Final Thought: If you find that your total itemized deductions are consistently just a few thousand dollars short of the standard deduction, consider the bunching strategy mentioned above. It is one of the most effective ways to legally bypass the limitations of the current tax code.