You’ve hit your 120 payments. You’ve done the time in the non-profit trenches or the government cubicle. You submitted that final form months ago, and yet, here we are in 2026, and your balance hasn't moved an inch. Honestly, it's exhausting.

The PSLF backlog delays loan forgiveness for thousands of public servants right now, and the frustration is real. Between the death of the SAVE plan and the rollout of the new Repayment Assistance Plan (RAP) coming this July, the Department of Education’s processing center looks like a digital traffic jam.

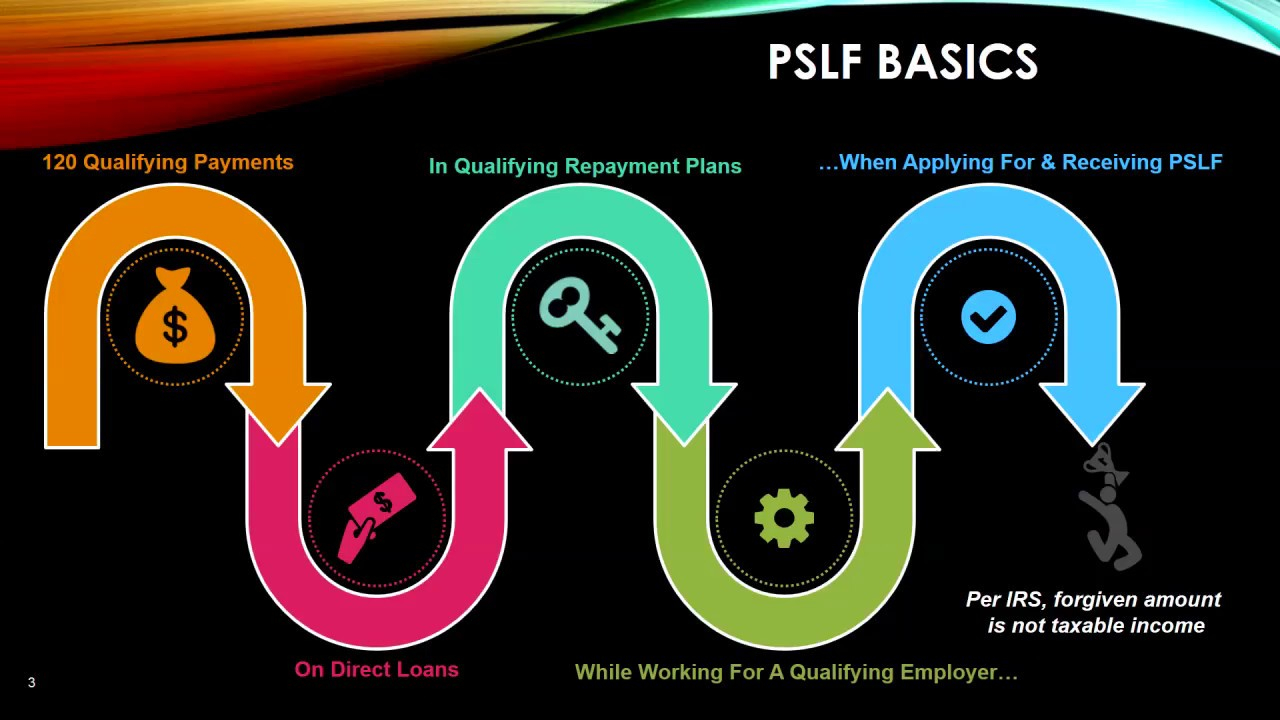

Why is there a PSLF backlog anyway?

Basically, the system is choked. After the 2025 government shutdown and the massive legal battles over income-driven repayment, the Department of Education (ED) ended up with a mountain of paperwork. According to recent court-ordered status reports from January 2026, the backlog for PSLF Buyback applications alone has ballooned to over 80,000 pending requests.

It’s not just the buybacks. Every time a new lawsuit hits or a repayment plan gets scrapped, the servicers like MOHELA have to wait for new "instructions" from the feds. While they wait, your application sits in a virtual pile.

💡 You might also like: Interest Rates Today Cars: What Most People Get Wrong About the 2026 Market

The AFT Lawsuit and Tax Protection

There is a bit of a silver lining if you're worried about the 2026 tax changes. Since January 1, 2026, most student loan forgiveness—specifically through IDR—is technically taxable again at the federal level because the American Rescue Plan's tax-free provision expired.

However, thanks to a preliminary agreement between the Education Department and the American Federation of Teachers (AFT), people caught in the PSLF backlog delays loan forgiveness shouldn't get hit with a surprise tax bill. If you already qualified for forgiveness but the ED just hasn't gotten around to clicking "approve" on your file, they’ve agreed not to file a 1099-C against you.

Plus, PSLF itself remains tax-free at the federal level by law. It’s one of the few things that actually stayed stable while everything else felt like it was falling apart.

The PSLF Buyback Trap

Many people are looking at the PSLF Buyback program as a way to escape. It sounds great on paper: you pay for months you were in a "wrong" forbearance to get to that 120-payment mark faster.

But here’s the kicker. The backlog is so deep that some borrowers have been waiting since October 2024 for a buyback quote. If you’re only three or four months away from 120 through normal payments, it might actually be faster to just keep paying rather than waiting for the ED to process a buyback request.

- Current estimated wait: 12+ months for many buyback applicants.

- The "Top of the Pile" Rumor: Some Reddit users in the r/PSLF community claim that resubmitting forms can help, but honestly, that often just resets your clock. Don't do it unless a representative explicitly tells you to.

- Administrative Forbearance: If you’re at 120 and waiting for the discharge, make sure you checked the box for administrative forbearance on your last ECF. You shouldn't have to keep sending them money while they take their sweet time.

New Rules Coming in July 2026

We have to talk about the One Big Beautiful Bill Act (OBBBA). It's changing the game. Starting July 1, 2026, the Secretary of Education has the power to disqualify certain employers from PSLF if they are deemed to have a "substantial illegal purpose."

This is a huge shift. If your employer gets blacklisted after July, your payments from that point on won't count. The good news? Anything you earned before the determination still counts. But this adds another layer of bureaucracy to an already slow system.

If you are working for a "borderline" organization, you really want to get your paperwork processed before the summer.

Actionable Steps to Beat the Delay

Stop checking your account every hour. It won’t help. Instead, do these things to protect your sanity and your wallet.

1. Download Everything Now

Servicers change. Records get lost. Log into StudentAid.gov and your servicer (MOHELA, etc.) and download your payment history and every "Employment Certification Form" you’ve ever submitted. Do it today.

🔗 Read more: Why USPS ZIP Code Lookup Plus 4 Still Matters More Than You Think

2. Use the "View All Activity" Tool

Don't just look at your balance. Go to your Dashboard on StudentAid.gov and select "View All Activity." This shows you the actual status of your application—whether it’s "Received," "In Review," or "Pending." If it says "Pending" for more than 90 days, it’s time to call.

3. The Ombudsman is Your Friend

If you have been at 120 payments for more than six months and nothing is happening, file a complaint with the FSA Ombudsman. It doesn't guarantee a fix, but it creates a paper trail that often gets eyes on a stuck file.

4. Re-evaluate the Buyback

If you are still in the SAVE plan forbearance (which most are, pending the RAP rollout), remember that those months might not count toward PSLF unless you eventually do a buyback. But if you’re already at 120, submit your final ECF now.

5. Watch the RAP Transition

If you aren't at 120 yet, you’ll likely be moved to the Repayment Assistance Plan (RAP) this July. Make sure your contact info is updated so you don't miss the transition notice. Missing a signature on a transition form could lead to a "gap" month that doesn't count toward your 120.

The PSLF backlog delays loan forgiveness is a mess, no doubt about it. But the law is still on your side. As long as you have the 120 months of qualifying service and the right type of loans, that "zero" balance is coming—eventually.

Keep your records tight. Stay on top of the July deadlines. And whatever you do, don't stop certifying your employment just because the system is slow.

Critical Next Steps

- Verify your employer's status on the FSA Employer Search tool before the July 1, 2026 rule changes take effect.

- Submit a fresh Employment Certification Form (ECF) if it has been more than a year since your last update, as this forces a manual count of your "qualifying payments."

- Check your "Tax Statements" section on your servicer's site by January 31, 2026, to ensure no 1099-C was issued if you are part of the AFT backlog agreement.