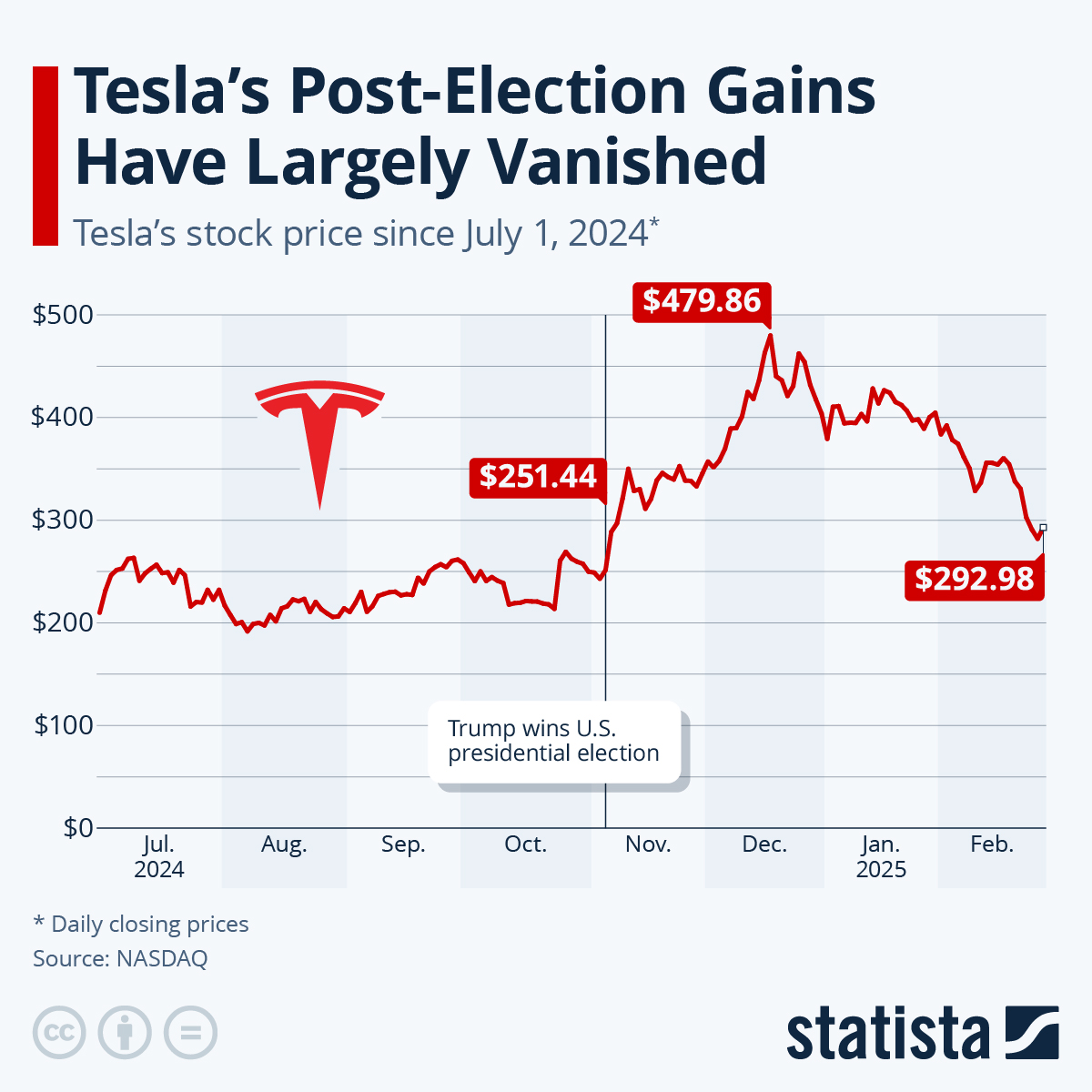

Tesla is never boring. Honestly, if you're looking for a quiet, "set it and forget it" kind of investment, this probably isn't the zip code for you. As of this weekend, Sunday, January 18, 2026, the price of tesla stock today sits at $437.52. That’s where the market hit the "pause" button on Friday afternoon, and it’s where everyone is staring as we wait for the opening bell on Monday.

The stock took a tiny breather at the end of the week, dipping about 0.24%. It's not a crash. It's not a moon-shot. It’s basically the market holding its breath. Why? Because the "Big One" is coming on January 28. That's when Tesla drops its Q4 2025 earnings report, and if you've been around the block with Elon Musk before, you know that report will either be a springboard or a trapdoor.

The Weird Reality of $437

Most people see a number like $437.52 and think it's just a price. It’s not. It’s a battlefield. Right now, Tesla is trading way above where traditional math says it should be. If you look at a Discounted Cash Flow (DCF) model—the kind of stuff buttoned-up analysts at places like Simply Wall St use—they’ll tell you the "fair value" is closer to $171.

That’s a massive gap.

Investors are paying a huge premium. We’re talking about a Forward P/E ratio that has touched 200x recently. To put that in perspective, your average car company like Ford or GM usually trades at a P/E of around 8x. So, why is the price of tesla stock today still holding strong in the $430s?

👉 See also: Why Saying Sorry We Are Closed on Friday is Actually Good for Your Business

It’s because nobody is buying Tesla because they think it's a car company. They're buying the "everything app" of hardware. They’re betting on the Optimus robots, the Dojo supercomputer, and the dream of a world where your car makes you money as a robotaxi while you sleep.

What's Actually Moving the Price of Tesla Stock Today?

If you’re trying to figure out if this is a good entry point, you’ve got to look at the 2025 delivery numbers. They were... well, they were a bit of a gut punch for the bulls.

Tesla delivered about 1.64 million vehicles in 2025. That’s actually down nearly 9% from 2024. For a company that used to promise 50% annual growth, seeing a decline for the second year in a row is a tough pill to swallow. In the fourth quarter alone, deliveries were 418,227. Wall Street wanted more. The fact that the stock hasn't completely collapsed despite these dwindling delivery numbers tells you that the "AI narrative" is doing a lot of heavy lifting.

The Trump Factor and the EV Slump

There's no way to talk about Tesla in 2026 without mentioning the political landscape. With the current administration not exactly making EVs a top priority, the federal tax credits that used to prop up demand are under fire. Some analysts, like the team over at Zacks, have slapped a "Sell" rating on the stock because they're worried about a 15% plunge in deliveries for 2026.

✨ Don't miss: Why A Force of One Still Matters in 2026: The Truth About Solo Success

Competition is also getting mean. Nvidia recently dropped a bombshell at CES 2026 about their own autonomous driving systems for personal cars. Suddenly, Tesla’s "moat" in self-driving tech feels a little less like a deep canyon and more like a backyard fence.

The "Ives" vs. "Bears" Debate

You’ve got guys like Dan Ives at Wedbush who are still banging the drum with a $600 price target. He sees the recent delivery dip as a "short-term noise" event. On the flip side, you have firms like GLJ Research who think the stock is worth $25.

Yes, twenty-five dollars.

The range of expert opinions on the price of tesla stock today is wider than the Grand Canyon. It's essentially a Rorschach test for investors. Do you see a struggling car company or a world-dominating AI powerhouse?

🔗 Read more: Who Bought TikTok After the Ban: What Really Happened

The January 28 Earnings: What to Watch

Since we are only ten days away from the earnings call, the volatility is likely to ramp up. Here is what's actually going to matter:

- Automotive Gross Margins: If these have stabilized, the stock might fly. If they keep slipping because Tesla has to keep cutting prices to sell cars, expect a sell-off.

- The FSD Subscription Pivot: Musk has been pushing the $99 monthly subscription for Full Self-Driving. This is great for long-term cash flow, but it hurts the "big upfront check" revenue that used to juice the quarterly numbers.

- Robotaxi Timelines: If Elon gives a concrete date for a multi-city rollout in 2026, the $437 price will look like a bargain. If he’s vague, the bears will pounce.

Honestly, the energy storage side of the business is the "secret sauce" right now. Tesla deployed 14.2 GWh of energy storage in Q4 alone—a record. It’s the one part of the business that is growing like crazy, even while the car sales are hitting a speed bump.

Actionable Insights for Investors

If you're holding or looking to buy, keep these levels in your head. The 100-day moving average is sitting around $421. If the stock breaks below that, it could head toward $363 pretty fast. On the upside, there’s a lot of resistance at $492. It’s tried to break $500 and failed.

Watch the volume. If the price starts sliding on high volume before Jan 28, it means the "smart money" is getting out of the way. If it stays flat, we're likely in for a massive "coin flip" reaction once the numbers hit the tape.

Check the 14-day RSI (Relative Strength Index). It’s currently hovering around 41, which means the stock isn't "oversold" yet, but it’s leaning that way. There’s room for more downside before it becomes a technical "buy."

Next Steps for Your Portfolio:

- Monitor the $421 support level; a daily close below this could signal a deeper correction toward $400.

- Wait for the January 28 earnings call to confirm if automotive gross margins have bottomed out before adding to a long position.

- Keep an eye on the "Energy Storage" revenue line in the upcoming report, as it may be the primary catalyst for a valuation decoupling from the traditional auto sector.