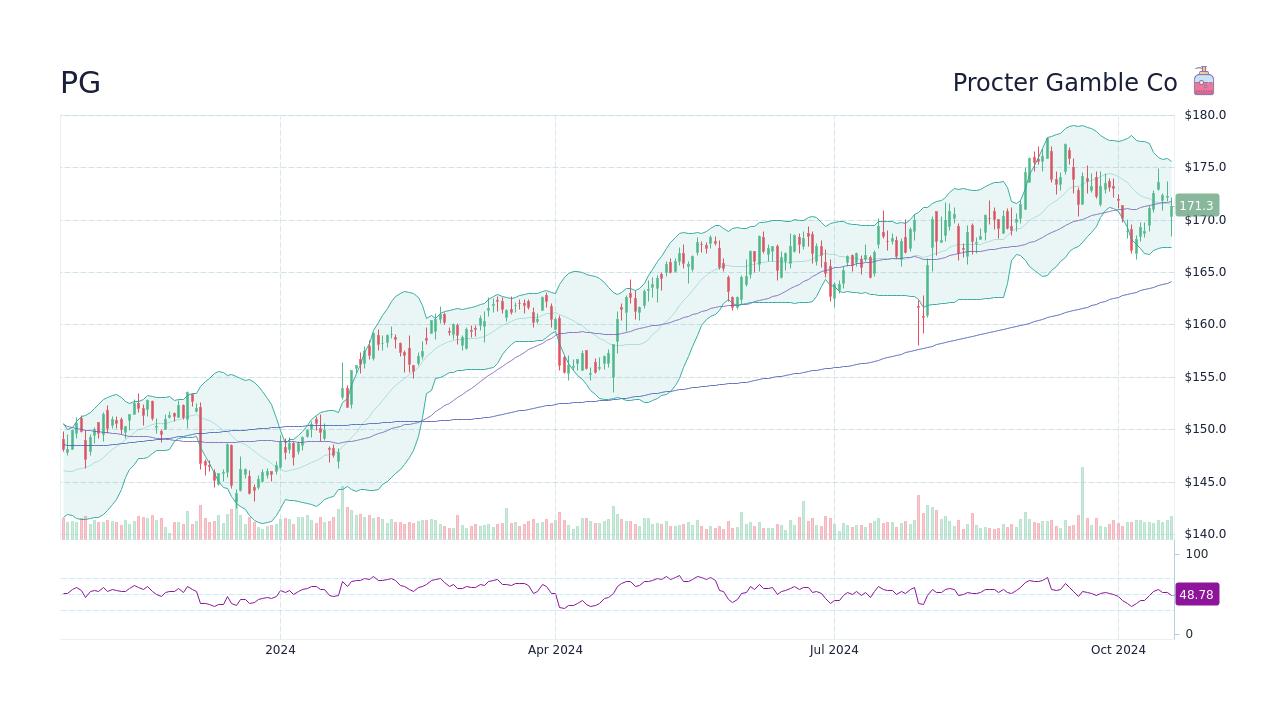

If you’ve been looking at your portfolio today, things might look a little weird for Procter & Gamble (PG). The stock is actually climbing, trading around $146.22 at the time of writing, but there’s a strange "offer" floating around that has some investors scratching their heads. Basically, a firm called Potemkin Limited is trying to buy shares for $100.00 each.

Yes, you read that right.

While the stock is hovering near $146, someone is asking you to sell it to them for a 31% discount. Honestly, it's one of those "mini-tender" offers that pops up every now and then to catch people off guard. P&G officially came out this morning, January 14, 2026, telling everyone to just ignore it. It’s not a hostile takeover; it’s more like someone asking if they can buy your $20 bill for $14.

What’s Actually Moving PG Stock News Today

The real story isn't the low-ball offer. It’s the dividend. Yesterday afternoon, the board declared a quarterly payout of $1.0568 per share. If you own the stock by January 23, 2026, you’re getting paid on February 17.

This is huge because it marks 135 years of consecutive payments. Think about that. They’ve been paying out cash since 1890. They’ve also increased that dividend for 69 straight years. In a market where everything feels shaky, P&G is basically the financial equivalent of a sturdy pair of boots.

🔗 Read more: Jamie Dimon Explained: Why the King of Wall Street Still Matters in 2026

Analysts are all over the place

Wall Street can't seem to agree on what P&G is worth right now. Just this morning, UBS analyst Peter Grom trimmed his price target to $161 from $176. He kept his "Buy" rating, but he’s essentially saying, "Look, things are tough out there."

People are stretched. Inflation isn't the monster it was, but the "value-seeking" behavior—fancy talk for people buying store brands instead of Tide—is real. Piper Sandler recently noted that about half of P&G’s sales come from U.S. consumers who are feeling the pinch.

The Numbers You Need to Care About

P&G is heading into its Q2 2026 earnings report on January 22. That’s only a week away. Last quarter, they actually beat expectations with an EPS of $1.99 on roughly $22.4 billion in revenue.

But investors are nervous about volume.

💡 You might also like: Influence: The Psychology of Persuasion Book and Why It Still Actually Works

- Price vs. Volume: P&G has been raising prices to stay profitable. It’s worked, but eventually, people stop buying the $20 detergent.

- Stock Movement: The stock hit a 52-week low of $137.62 recently, but it’s clawing its way back.

- The "Potemkin" Distraction: This mini-tender for 50,000 shares is a drop in the bucket for a company with a $341 billion market cap.

Investors aren't selling. Institutional heavyweights like Swedbank AB and Farther Finance Advisors actually increased their stakes recently. They see the dip as a chance to grab a 2.9% yield at a "reasonable" price.

The Texas Toothpaste Deal

There was also a weird bit of news involving the Texas Attorney General. P&G had to settle over how much fluoride toothpaste for kids was shown in their ads. They have to make sure the packaging is accurate for the next five years. It doesn’t really hit the bottom line, but it’s a reminder that even the "Dividend Kings" have to deal with red tape.

Is P&G Still a "Safe" Bet?

Kinda. It depends on why you’re buying. If you want a tech-style moonshot, look elsewhere. But if you want a company that plans to return $15 billion to shareholders this year through dividends and buybacks, P&G is the gold standard.

They are forecasting earnings growth of 3% to 4% for fiscal 2026. It’s boring growth, but it’s stable. The stock is currently trading at about 21x forward earnings, which is actually a bit cheaper than its historical average of 22.8x.

📖 Related: How to make a living selling on eBay: What actually works in 2026

Actionable Next Steps for Investors

If you are holding PG shares right now, do not tender them to the Potemkin offer. You would be losing about $46 per share for no reason.

Keep a close eye on the January 22 earnings call. The big thing to watch isn't the profit—it's the volume growth. If P&G reports that they are selling fewer physical bottles of Olay or boxes of Pampers, the stock might retest those $137 lows. However, if you’re a long-term income investor, the January 23 record date is your primary target to lock in that next $1.0568 per share dividend payment.

Ensure your brokerage account is set for DRIP (Dividend Reinvestment Plan) if you want to compound that 2.9% yield automatically. Given the current price action, P&G is behaving more like a defensive bond proxy than a growth engine, making it a "hold" for most and a "buy the dip" candidate for dividend hunters.