You just got that bill from the New York City Department of Finance. It’s sitting on your kitchen counter, probably looking a bit intimidating with all those codes and the "Tax Class" jargon. Dealing with a nyc property tax payment isn’t exactly a fun Saturday afternoon activity, but honestly, it’s one of those things where being even a little bit lazy can cost you a fortune in interest. NYC doesn't play around when it comes to late fees.

New York City operates on a fiscal year that starts on July 1st. It’s a bit weird compared to the calendar year most of us live by. If your property is valued at $250,000 or less, you’re usually paying quarterly. If it’s worth more, you’re on a semi-annual schedule.

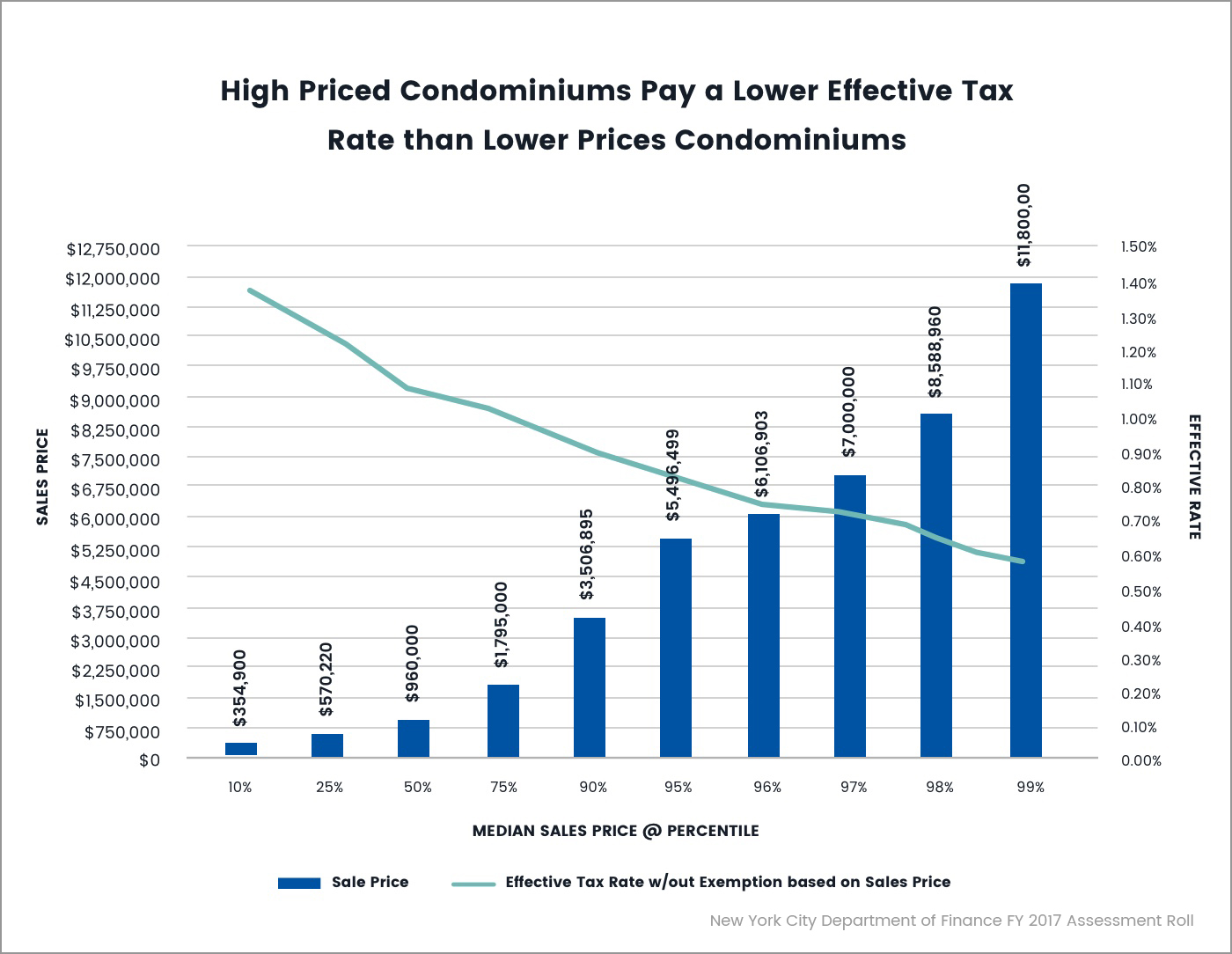

It sounds simple. It isn't.

The city’s property tax system is a beast. It’s divided into four classes, and where you land changes everything. Class 1 is mostly one-to-three-unit residential properties. Class 2 is cooperatives and condominiums. Class 3 is utility property (you probably aren't this), and Class 4 is everything else commercial. Every year, the rates shift slightly, and if you aren't paying attention, your escrow account might not cover the jump, leaving you with a surprise bill.

The Brutal Reality of Interest Rates

If you miss a nyc property tax payment, the city hits you with interest immediately. For the 2024-2025 tax year, the interest rate for late payments on properties with an assessed value of $250,000 or less was roughly 6%. For anything valued higher? It jumps significantly, sometimes as high as 12% or 13% depending on the Council's latest vote.

Think about that.

That is higher than most high-yield savings accounts. You are essentially taking out a very expensive, involuntary loan from the city.

How You Actually Pay This Thing

Most people think they have to mail a check. You can, but it’s 2026—don't. The mail is slow, and if that envelope gets lost or postmarked a day late, you’re on the hook for the penalty.

📖 Related: PDI Stock Price Today: What Most People Get Wrong About This 14% Yield

The NYC CityPay portal is the standard. It’s clunky, sure. It looks like it was designed in 2005. But it works. You can pay via eCheck, which is basically a direct transfer from your bank account. The best part? There’s no fee for eChecks. If you try to use a credit card, they’ll slap a 2% (or higher) convenience fee on top. On a $5,000 tax bill, that’s an extra $100 just for the "privilege" of using your points card. It’s rarely worth it.

If you’re a fan of the old-school way, you can go to a Manhattan Business Center or any of the borough-specific offices. But honestly, who has time to stand in line at 66 John Street?

Why Your Bill Might Be Wrong

Assessments in NYC are notoriously messy. The Department of Finance (DOF) determines your "Market Value," then applies a percentage to get the "Assessed Value." For Class 1 homes, it’s 6%.

But here is the kicker: the "Market Value" the city sees is often totally disconnected from what you could actually sell your house for on Zillow or through a broker. They use a statistical model based on comparable sales in your neighborhood. If a neighbor sold a renovated brownstone for $4 million and you're living in a fixer-upper, the city might think your place is worth more than it is.

You have a window to challenge this. Every year, usually between January and March, you can file an appeal with the NYC Tax Commission. Most people don't bother. They just complain about the bill. If you think your assessment is off by more than 10%, it’s worth looking into a "tax grievance."

The "Escrow" Trap

If you have a mortgage, you probably don't pay the city directly. Your bank does. You pay the bank every month, they hold it in an escrow account, and then they make the nyc property tax payment on your behalf.

This feels safe. It’s often not.

👉 See also: Getting a Mortgage on a 300k Home Without Overpaying

Banks mess up. They might miss a payment, or they might underestimate how much the taxes will go up. I've seen cases where a homeowner gets a "Notice of Property Value" showing a huge spike, the bank doesn't adjust the monthly escrow fast enough, and a year later, the homeowner gets a bill for a $3,000 "escrow shortage." It’s a gut punch.

Check your annual escrow statement. Compare it to the DOF website. It takes ten minutes and can save you from a massive financial headache down the road.

Exemptions You’re Probably Missing

The city isn't going to tap you on the shoulder and offer you a discount. You have to ask for it. The STAR (School Tax Relief) credit is the big one. If you own your home and it's your primary residence, and your income is below a certain threshold (usually $500,000 for the credit), you should be getting this.

Then there is the E-Seniors (SCHE) and Disability (DHE) exemptions. These can cut your bill in half. Literally 50% off. But the paperwork is dense, and you have to renew it. If you’re a veteran or a member of the clergy, there are smaller breaks available too.

The Lien Sale: The Worst Case Scenario

If you ignore your nyc property tax payment for too long, the city doesn't just send mean letters. They sell your debt.

The NYC Tax Lien Sale is a process where the city sells the right to collect your unpaid taxes to a private trust. This trust then charges much higher interest rates and can eventually move to foreclose on your property. It’s a nightmare. The city has faced a lot of political pressure recently to reform or even abolish the lien sale because of how it impacts low-income neighborhoods, but for now, the threat remains. Don't let it get that far.

Deadlines to Tattoo on Your Brain

- July 1: First quarter (or first half) payment due.

- October 1: Second quarter due.

- January 1: Third quarter (or second half) due.

- April 1: Fourth quarter due.

There is a "grace period." If your bill is due on the 1st, you usually have until the 15th to pay without interest. On the 16th? You’re cooked. The interest is backdated to the 1st.

✨ Don't miss: Class A Berkshire Hathaway Stock Price: Why $740,000 Is Only Half the Story

Practical Steps to Take Right Now

First, go to the NYC Department of Finance website and look up your "Property Account." You can search by your address or your BBL (Borough, Block, and Lot) number.

Second, look at the "Account History" tab. Make sure every payment you’ve made—or your bank has made—is actually reflected there. If you see "Open" balances from three years ago, you have a problem that needs a phone call to 311 immediately.

Third, check your exemptions. Look for "STAR," "SCHE," or "VET." If they aren't there and you think they should be, the deadline to apply for the next tax year is usually March 15th.

Fourth, sign up for the DOF's email reminders. It’s a simple way to make sure a bill doesn't get buried under a pile of junk mail.

Fifth, if you are struggling to pay, look into the "Property Tax and Interest Deferral" (PTAID) program. It allows qualifying homeowners to defer their payments or enter a payment plan. It’s not a free pass, but it stops the aggressive collection process.

New York is expensive enough. Don't give the city extra money in interest and penalties just because the system is confusing. Stay on top of the portal, verify your bank is doing its job, and always, always double-check your tax class. It’s your money.