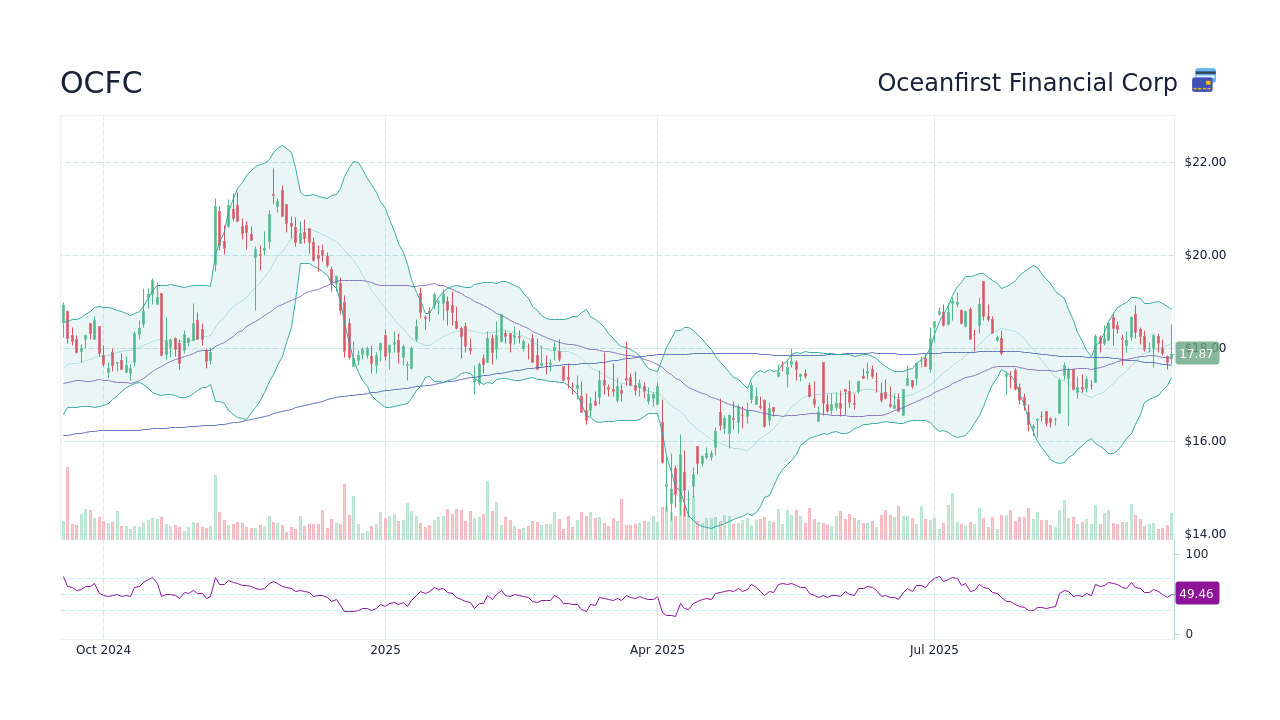

You've probably seen the ticker OCFC flashing on your screen and wondered if it's a hidden gem or just another regional bank struggling to keep its head above water. Honestly, the oceanfirst bank stock price has been on a bit of a rollercoaster lately. As of mid-January 2026, the stock is hovering around $18.33 to $18.40. It’s a weird spot to be in. On one hand, you have a bank that’s been around since 1902, which is practically ancient in the financial world. On the other hand, the market is giving it a bit of a "wait and see" treatment.

Some folks look at the 52-week high of $20.61 and think there’s a massive gap to fill. Others see the 52-week low of $14.29 and get nervous about a potential slide back down. But the real story isn't just in those two numbers. It’s in the $1.05 billion market cap and the fact that the bank is currently trading at a price-to-earnings (P/E) ratio of roughly 14.2. That's actually pretty cheap compared to the broader market, but regional banks always sort of play by their own rules.

The Merger Curveball Everyone's Talking About

Late in December 2025, OceanFirst dropped a bit of a bombshell. They announced an all-stock merger with Flushing Financial. This $579 million deal sent the oceanfirst bank stock price slipping about 6.6% almost immediately. Why? Because investors usually get jittery about "merger math." It’s basically a massive integration task. If you’re holding the stock, you're looking at a bank that’s trying to scale up fast to compete with the big boys, but the market is asking: "At what cost?"

✨ Don't miss: Department of Gains Coin: Is This Actually the Next Big Meme Play?

Christopher D. Maher, the CEO, has been pretty vocal about shifting the business model. They're moving away from doing everything in-house. For instance, they recently partnered with a national mortgage company to handle residential loans. That move was basically a way to slash headcount and operating expenses as they headed into 2026. It's a classic "leaner and meaner" play. Does it work? Sometimes. But in the short term, it usually creates a lot of noise in the stock price.

Why Analysts Are Kinda Split

If you ask seven different Wall Street analysts where this is going, you’ll get seven different shades of "maybe." The consensus right now is a Hold. But look closer at the price targets. The average target is sitting at $21.60. That represents a potential upside of nearly 18%.

- Raymond James has been a cheerleader, sticking with a "Strong Buy."

- Stephens recently lowered their target from $23 to $22 but kept an "Outperform" rating.

- Hovde Group is sitting firmly in the "Hold" camp.

It’s a classic tug-of-war. The bulls see a bank that is undervalued with a tangible book value per share (TBVPS) around $19.43. The bears worry that net interest income is growing too slowly—only about 3.1% annually over the last few years. When the cost of keeping deposits high starts eating into the profit from loans, the stock price feels the squeeze.

What’s Driving the Oceanfirst bank stock price Right Now?

The upcoming earnings report on January 22, 2026, is the next big hurdle. Analysts are looking for earnings of about $0.39 per share. If they beat that, we might see a rally toward that $20 mark. If they miss, or if the management's commentary on the Flushing Financial merger sounds "expensive," we could see it test the $17 support level again.

📖 Related: Top OnlyFans Earners: What Really Happens Behind the Paywall

Earnings growth is projected to be around 28% for the coming year. That’s a big jump from $1.60 to over $2.00 per share. But projections are just that—projections. You've also got to consider the dividend. OceanFirst has been incredibly consistent here. They just declared their 115th consecutive quarterly dividend. At $0.20 per share, you're looking at a yield of about 4.4%. For a lot of income investors, that yield is a "safety net" that keeps the floor from falling out under the stock.

The Real Risks Nobody Mentions

Everyone talks about interest rates, but the real "hidden" risk for OceanFirst is their commercial loan pipeline. It hit a record $790.8 million recently. That sounds great on paper. More loans mean more interest, right? Sorta. It also means more exposure if the commercial real estate market in the Northeast takes a hit.

Institutional ownership is high—about 70%. That’s usually a good sign. It means the "smart money" trusts the management. But it also means that if a couple of big funds decide to exit at the same time, the price can tank fast because there isn't enough retail volume to soak up the selling.

🔗 Read more: California State and Federal Tax Calculator: Why Your Take-Home Pay Feels So Low

Is the Discount Real or a Trap?

Simply Wall St recently argued that the stock might be 20% undervalued based on cash flow models. They put a "fair value" at $21.67. If you believe that, the current oceanfirst bank stock price is a bargain. But "optical cheapness" can be a trap in banking. Sometimes a bank is cheap because its efficiency ratio is climbing—which it has been, hitting over 70% recently. A high efficiency ratio means it costs the bank more to make a dollar. That’s the opposite of what you want to see.

Actionable Insights for Investors

If you're watching this stock, don't just stare at the daily ticker.

- Watch the January 22 Earnings Call: Specifically, listen for "integration costs" related to the Flushing merger. If those numbers are higher than expected, the stock will likely stay sideways.

- Check the Net Interest Margin (NIM): It’s currently around 2.91%. If this starts to dip, it means the bank is paying too much for deposits, which is a red flag for future price growth.

- Use the Dividend as a Gauge: As long as that $0.80 annual dividend remains stable, the stock has a strong support level. A yield above 4.5% usually attracts "buy the dip" investors.

Essentially, OceanFirst is a play on regional consolidation and cost-cutting. It isn't a high-growth tech stock. It’s a slow-and-steady bank trying to navigate a tricky merger and a shifting interest rate environment. If they can execute on the merger without blowing the budget, that $21 price target isn't just a dream—it's a very likely reality by the end of 2026.

Keep an eye on the commercial loan originations in the next quarter. They jumped 74% to over $739 million in late 2025. If that momentum carries into 2026, the revenue growth will eventually force the stock price higher, regardless of the short-term merger jitters.