New York is famous for a lot of things. Pizza. Broadway. The Empire State Building. But if you live or work here, you probably know it for something a bit less glamorous: the tax bill. Honestly, trying to figure out what is NYS income tax can feel like trying to navigate the subway during rush hour without a map. It’s crowded, confusing, and if you make one wrong turn, you’re stuck in a place you didn't want to be.

Most people look at their paystub, see a chunk of money missing, and just shrug. "It's New York," they say. But there is a literal method to the madness. New York State uses a graduated tax system. That basically means the more you earn, the higher the percentage the state takes. It isn't just one flat rate like you might find in places like Pennsylvania or Illinois. Instead, it’s a tiered cake of taxation, and the slices get bigger as you move up the ladder.

How the Brackets Actually Hit Your Wallet

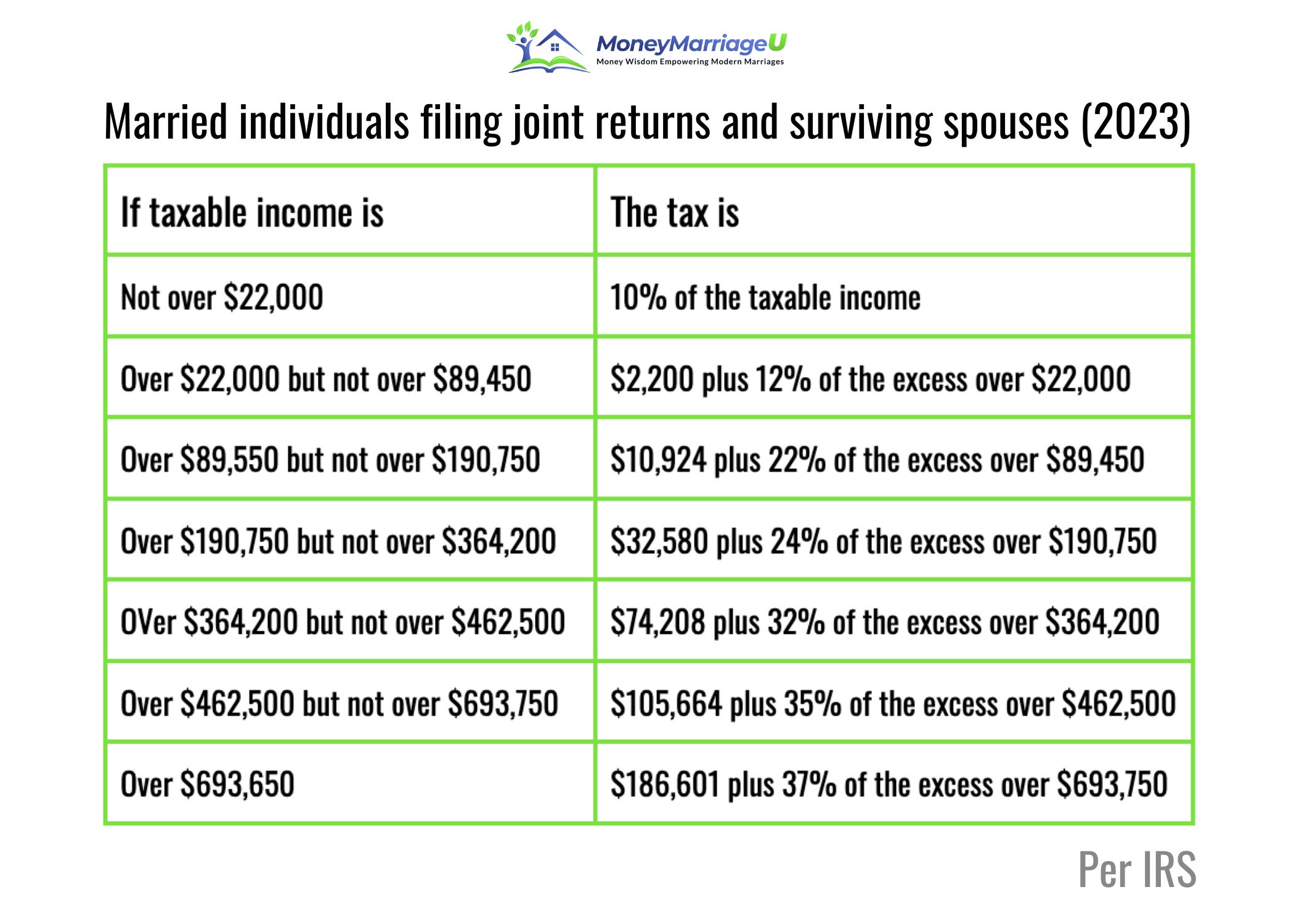

Let’s get real about the numbers. For the 2024 and 2025 tax years, New York has brackets that range from 4% all the way up to 10.9%. That top rate? It’s one of the highest in the country. But don't panic. You aren't paying 10.9% on every single dollar unless you're making millions.

Tax brackets are marginal. If you're a single filer making $50,000, you're not paying the same rate on your first dollar as you are on your last. The first $8,500 is taxed at 4%. The next chunk is taxed at 4.5%, and so on. It’s a common misconception that getting a raise and "moving into a higher bracket" means you lose more money than you gained. That’s just not how the math works. You only pay the higher rate on the dollars that actually fall into that new, higher bucket.

It gets even more interesting—or annoying, depending on your perspective—if you live in the Five Boroughs.

The NYC Surcharge: A City Within a State

If you live in New York City, you’re basically getting hit with a double whammy. On top of what is NYS income tax, you have to pay a separate New York City resident income tax. Yonkers does something similar with a resident income tax surcharge.

✨ Don't miss: Cox Tech Support Business Needs: What Actually Happens When the Internet Quits

Why? Because maintaining a city of 8 million people is expensive. This city tax is also progressive, ranging roughly from 3.078% to 3.876%. When you stack that on top of the state and federal taxes, it’s easy to see why some high earners start looking at Florida real estate listings. It’s a heavy lift. If you work in the city but live in New Jersey or Westchester, the rules change. You generally pay based on where you earned the money, but New York is notoriously aggressive about its "convenience of the employer" rule.

The Convenience of the Employer Rule (The Remote Work Trap)

This is where things get spicy. New York is one of the few states that will tax you even if you aren't physically in the state. If your office is in Manhattan, but you’re working from your couch in Vermont for your own convenience rather than because your boss forced you to, New York wants its cut.

This led to some massive legal headaches during the pandemic. People fled the city, thinking they’d stop paying NYS taxes. They were wrong. Unless your employer has a legitimate business reason for you to be in another state, the New York Department of Taxation and Finance considers you a New Yorker for tax purposes. They are incredibly good at finding this money. They audit more than almost any other state. They track cell phone records. They check social media. If you claim you weren't in the state, you better have the receipts to prove it.

Deductions and Credits: How to Keep More of Your Money

It isn't all bad news. New York offers several credits that can actually put money back in your pocket. The Empire State Child Credit is a big one. There’s also the Earned Income Credit (EIC) for lower-to-moderate-income working individuals and families.

- Standard Deduction: For 2024, if you're single, your standard deduction is $8,000. If you're married filing jointly, it’s $16,050. This is the amount you subtract from your income before you even start calculating tax.

- Itemized Deductions: New York allows you to itemize even if you took the standard deduction on your federal return. This is a huge deal. You can deduct things like property taxes (up to a limit), charitable contributions, and certain medical expenses.

- College Tuition Credit: If you’re paying for school, you might be eligible for a credit or a deduction. Usually, the credit is the better deal because it’s a dollar-for-dollar reduction of your tax bill.

IT-201 vs. IT-203: Knowing Which Form to File

When tax season rolls around, you’ll hear these form numbers tossed around. If you lived in New York for the full year, you file the IT-201. It’s the standard resident return.

🔗 Read more: Canada Tariffs on US Goods Before Trump: What Most People Get Wrong

But what if you moved? Or what if you just commuted in? That’s where the IT-203 comes in. This is for non-residents and part-year residents. You basically have to do a weird math problem where you calculate what your tax would have been if you lived in NY all year, and then you multiply it by the percentage of your income that actually came from New York sources. It’s tedious. It’s also where most people make mistakes that trigger "please explain this" letters from the state.

The Audit Culture in Albany

You really don't want to mess with the NYS Department of Taxation and Finance. They are efficient. They use sophisticated data-matching programs that compare your state return to your federal return. If your numbers don't match, you’ll get a notice.

The biggest red flag? Claiming you moved out of the state when you actually didn't. To "break domicile" in New York, you have to prove that you’ve truly left. This means moving your "near and dear" items—your family photos, your dog, your primary bank account—to the new location. Just buying a house in Florida isn't enough if you still spend 184 days a year in your Brooklyn apartment. That 183-day rule is the golden threshold. Spend one day over half the year in NY, and you’re a resident for tax purposes. Period.

What Is NYS Income Tax for Small Business Owners?

If you run a business, things get even more tangled. Most small businesses in New York are "pass-through" entities. This means the business doesn't pay income tax itself; the income "passes through" to the owners, who pay it on their personal NYS tax returns.

However, New York recently introduced the Pass-Through Entity Tax (PTET). This was a clever workaround for the federal SALT (State and Local Tax) deduction cap. By allowing the business to pay the tax at the entity level, business owners can effectively deduct their state taxes on their federal returns, saving thousands. It’s a move that shows NY actually does try to help its taxpayers—sometimes.

💡 You might also like: Bank of America Orland Park IL: What Most People Get Wrong About Local Banking

Real Talk: Is it Worth It?

People complain about the taxes here constantly. You’ll hear it at every dinner party. But what is NYS income tax really paying for? It funds one of the largest public university systems (SUNY) in the world. It pays for the massive infrastructure required to keep the state running. It funds social programs that are far more robust than what you'd find in the South or the Midwest.

Whether it's "worth it" is a personal call. But understanding the system is the only way to make sure you aren't overpaying. The state isn't going to tap you on the shoulder and say, "Hey, you forgot to take this deduction!" You have to find it yourself.

Practical Steps to Manage Your NYS Tax Burden

Don't wait until April 14th to figure this out. If you're a New Yorker, or even "New York adjacent," you need a strategy.

- Track your days. If you live in two states, use an app like Monaeo or TaxBird to track exactly how many days you spend in New York. If you hit 183, you're a resident. No excuses.

- Adjust your withholding. If you got a massive refund last year, you’re giving the state an interest-free loan. If you owed a lot, you might get hit with underpayment penalties. Use form IT-2104 to change how much your employer takes out.

- Check your credits. Look specifically at the Child and Dependent Care Credit. New York’s version is often more generous than the federal one.

- Keep "The Near and Dear." If you are moving, make the move real. Change your voter registration, your driver’s license, and your library card immediately. New York auditors look for these small details to prove you haven't actually left.

- Contribute to a 529 Plan. New York offers a state tax deduction of up to $5,000 ($10,000 for married couples) for contributions to a NY 529 college savings account. It’s one of the best ways to lower your taxable income while saving for the future.

The system is complex, but it isn't impenetrable. Stay organized, keep your receipts, and remember that in New York, the tax man always has a very long memory.