Honestly, if you ask someone on the street about the ny state income tax percentage, they’ll probably tell you it’s "way too high" and leave it at that. But "high" isn't a number you can put on a return. New York doesn't just have one tax rate; it has a graduated system that can feel like a maze if you aren't looking at the right map.

Most people think they’re paying a flat, massive chunk of their check to Albany. That’s rarely the case. Whether you're living in a quiet Upstate town or a cramped studio in Brooklyn, your actual tax bill is a mix of brackets, deductions, and—if you're unlucky—some local add-ons that can sting.

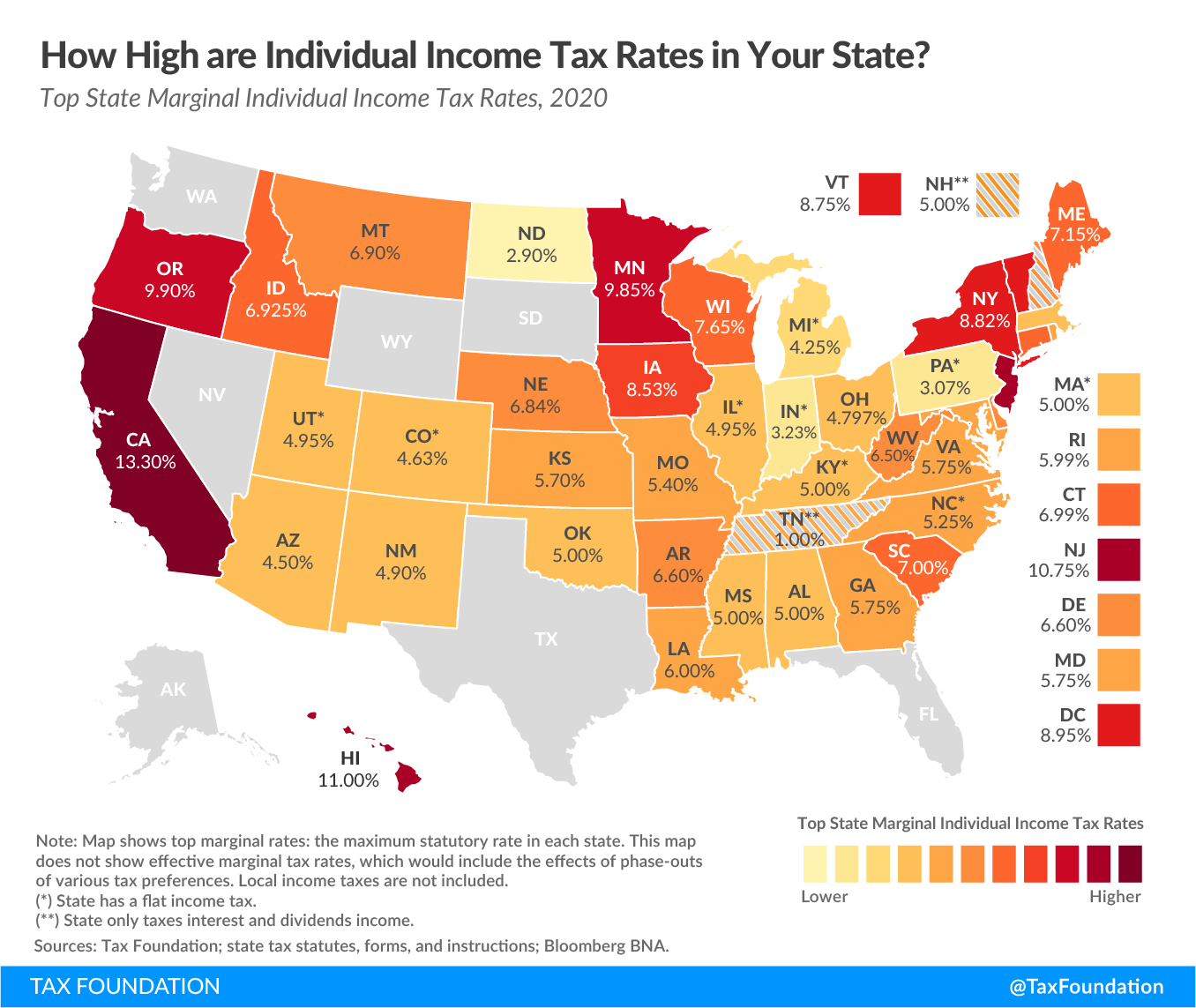

How the NY State Income Tax Percentage Actually Works

New York uses a progressive tax system. This basically means the more you earn, the higher the rate you pay on those "extra" dollars. For the 2025 tax year (the taxes you’ll be settling up in early 2026), the rates start as low as 4% and climb all the way to 10.9%.

It’s a wide range.

If you’re a single filer making under $8,500 in taxable income, you’re at that 4% mark. But as you climb the ladder, the percentages jump. Once you cross the $215,400 mark, you hit 6.85%. And for the true high earners—those bringing in over $25 million—the state takes 10.9%.

📖 Related: Oil Market News Today: Why Prices Are Crashing Despite Middle East Chaos

Here is the kicker: you don't pay that top rate on all your money. If you earn $100,000, only the portion above $80,650 is taxed at 6%. The first few thousand are still taxed at those lower 4% and 4.5% rates.

The NYC and Yonkers "Surprise"

If you live in New York City or Yonkers, you aren't just paying the state. You’re paying the city too. New York City adds its own local income tax on top of the state’s. These city rates generally hover between 3.078% and 3.876%.

When you combine a 6.85% state rate with a 3.876% city rate, you’re suddenly looking at over 10% of your income going to taxes before you even look at federal or FICA. It’s a heavy lift. Yonkers residents pay a "surcharge" which is essentially a percentage of their state tax—usually around 16.75% of whatever their state bill is.

Middle-Class Relief and the 2026 Shift

There is some good news. Governor Kathy Hochul recently signed off on the FY 2026 budget, which fast-tracked some middle-class tax cuts. For tax years starting in 2026, many New Yorkers will see their brackets dip slightly.

👉 See also: Cuanto son 100 dolares en quetzales: Why the Bank Rate Isn't What You Actually Get

For example, married couples filing jointly with income under $323,200 will see rates drop to a range of 3.9% to 5.9%. It’s not a massive drop, but in a state where everything from eggs to rent is rising, every fraction of a percent matters.

The state is also leaning heavily into credits. The Empire State Child Credit is getting a massive boost. For the 2025-2026 cycle, families can get up to $1,000 per child under age four. If your kids are older (4 to 17), that credit is roughly $500. This is a refundable credit, which is basically tax-speak for "money in your pocket even if you don't owe taxes."

Don't Forget the Standard Deduction

Before you apply any percentage, you subtract your standard deduction. For the 2025 tax year, the NY state standard deduction for a single person is $8,000. If you’re married filing jointly, it’s $16,050.

These numbers change slightly for 2026 due to inflation adjustments. Staying on top of these "boring" numbers is actually the best way to lower your effective tax rate.

✨ Don't miss: Dealing With the IRS San Diego CA Office Without Losing Your Mind

Common Misconceptions About NY Taxes

One thing people get wrong is the "Tax Flight" narrative. While some high earners do leave for Florida, the vast majority of New Yorkers stay and navigate these brackets.

Another big one? Thinking that a raise will "put you in a higher bracket and make you take home less money." This is a total myth. Because of how the progressive brackets work, you only pay the higher rate on the money within that new bracket. You never lose money by earning more.

Practical Steps for Your Next Return

Tax planning shouldn't happen in April. It happens now.

- Adjust your withholding: If you got a massive refund last year, you’re basically giving the state an interest-free loan. Use Form IT-2104 to tweak what’s coming out of your check.

- Track your residency: New York is aggressive about auditing people who claim to live elsewhere while spending 184 days or more in the state. If you moved, keep your receipts.

- Look for "Green" credits: The state is offering big breaks for geothermal energy systems (up to $10,000) and solar equipment.

- Check the Inflation Refund: Some households are eligible for a one-time "inflation refund" check of up to $400 depending on their 2023 income levels.

The ny state income tax percentage is a moving target. Between city taxes, state brackets, and the new middle-class cuts, your actual burden is unique to your zip code and your salary. Keep an eye on the 2026 changes, as the threshold for filing estimated taxes is jumping from $1,000 to $5,000, which might save some freelancers a few headaches next year.

To get ahead of your 2026 filing, verify your residency status and check if your household qualifies for the expanded Empire State Child Credit, as these adjustments will likely be the biggest factors in your final tax bill.