You’ve probably heard the rumors that New York is a tough place to die. Well, financially speaking, the rumors are true. While the federal government is out here raising its exemption to a whopping $15 million in 2026—thanks to the "One Big Beautiful Bill Act" passed last summer—Albany hasn't exactly followed suit.

If you live in the Empire State, you’re playing a completely different game. Honestly, it’s a game where the rules are designed to catch you off guard if you’re even a dollar over the limit. We aren't just talking about a slightly higher tax rate. We are talking about the "cliff."

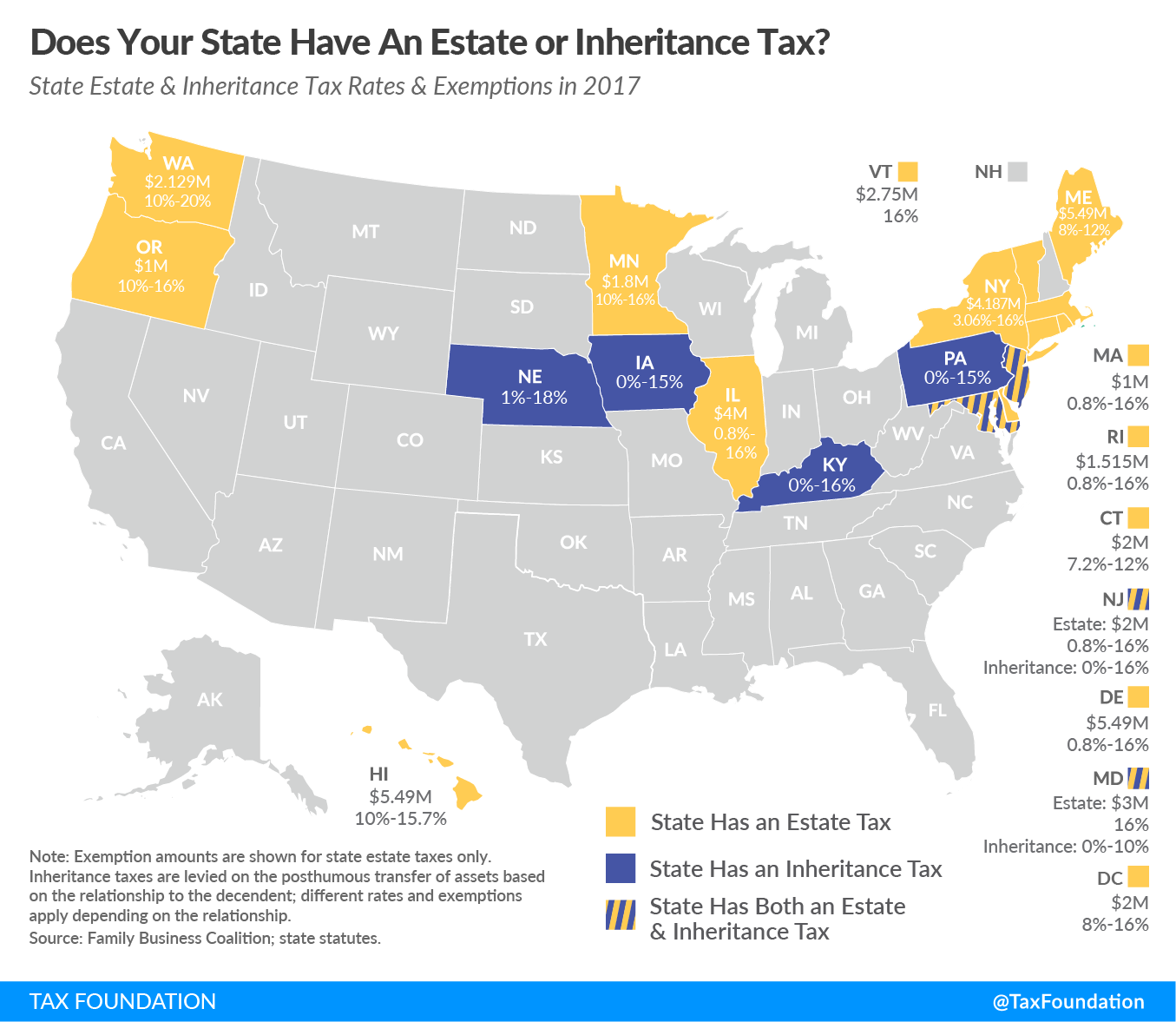

For 2026, the NY state estate tax exclusion is set at $7,350,000.

That sounds like a lot of money, and for most people, it is. But in a world where a modest brownstone in Brooklyn or a family home in Long Island can easily clear $2 million, and your 401(k) has been compounding for thirty years, you might be closer to that line than you think.

The Cliff: New York’s Punitive Mathematical Trap

Most taxes work like a staircase. You pay a little on the first chunk, a bit more on the next, and so on. The federal estate tax works this way; you only pay tax on the amount above the $15 million exemption.

New York doesn't do that.

New York uses a "cliff" provision. If your estate is valued at 105% or less of the exemption, you only pay tax on the excess. But the second you cross that 105% threshold? The entire exemption vanishes. Poof. Gone.

✨ Don't miss: Getting a Mortgage on a 300k Home Without Overpaying

Basically, if you die in 2026 with an estate worth $7,717,500 (which is 105% of $7.35 million), you are in the danger zone. If you have $7,717,501, New York taxes you on the entire amount starting from dollar one.

Think about that. One extra dollar in your savings account could trigger a tax bill of over $600,000. It is quite literally one of the most punitive tax structures in the United States. It's why estate planners in Manhattan and Westchester spend half their lives obsessing over "Santa Claus" clauses and charitable gifts.

Why Your Federal Plan Might Fail You in New York

A lot of people think they’re safe because their lawyer set up a plan based on federal limits. That's a mistake.

A common strategy for married couples is to leave everything to the surviving spouse. Under federal law, this is great because of "portability." If the first spouse doesn't use their $15 million exemption, the second spouse gets to "inherit" it, giving them a $30 million shield.

New York does not have portability.

If you leave everything to your spouse, you effectively waste your $7.35 million New York exemption. When the second spouse dies, they only have their own $7.35 million shield. If the total estate is $12 million, that second spouse’s estate is going to fall right off the cliff. They’ll owe the state a massive check while the federal government looks on and asks for nothing.

🔗 Read more: Class A Berkshire Hathaway Stock Price: Why $740,000 Is Only Half the Story

The Three-Year "Clawback" Rule

New York also doesn't have a gift tax. You can give away $1 million today and New York won't send you a bill.

But there’s a catch.

New York has a three-year "addback" rule. If you make a taxable gift and then die within three years, New York pulls that money back into your estate for tax calculation purposes. This rule was supposed to expire at the beginning of 2026, but the latest state budget extended it.

They know people try to give away their money on their deathbeds to avoid the cliff. The state wants its cut, and they’ve made sure the door stays shut on that particular exit strategy.

Real-World Strategies to Stay Off the Edge

So, what do people actually do to avoid this? It’s not about hiding money; it’s about moving it legally and with precision.

The Credit Shelter Trust (Bypass Trust)

Since you can't "port" your exemption to your spouse, you use it or lose it. Instead of leaving everything to your spouse directly, you put the amount of the NY exemption into a trust. Your spouse can still use the money and get income from it, but technically, it doesn't belong to them. When they pass away, that money goes to the kids tax-free, and the surviving spouse still has their own $7.35 million exemption to use.

💡 You might also like: Getting a music business degree online: What most people get wrong about the industry

The "Santa Claus" Provision

This is a nickname for a conditional charitable bequest. You basically write into your will: "If my estate is over the cliff limit, give the excess to [Charity Name] so I fall back under the line."

It is better to give $100,000 to a hospital or a museum than to let a $700,000 tax bill swallow your heirs' inheritance. It's a "fail-safe" that ensures the state doesn't get a windfall just because your Nvidia stock had a good month before you passed.

The Domicile Shift

We've all seen the headlines about New Yorkers moving to Florida. This is a huge reason why. Florida has no estate tax. Neither does Nevada or Texas.

However, you can’t just buy a condo in Miami and call it a day. The New York Department of Taxation and Finance is legendary for their residency audits. They look at where you spend your time, where you vote, where your "near and dear" items are (like family photos or your dog), and even where your primary doctor is located. If you want to avoid the NY state estate tax by moving, you have to actually leave.

Actionable Steps for 2026

If you’re sitting on assets—including life insurance and retirement accounts—that put you anywhere near the $7 million mark, you need to move.

- Audit your "Gross Estate": This isn't just your bank account. New York counts your house, your business interests, your IRAs, and even life insurance policies where you own the "incidents of ownership."

- Review your Will for "Federal" language: If your will says to fund a trust up to the "federal exemption amount," you are in trouble. In 2026, that would put $15 million into a trust, which is double the New York limit, likely triggering a massive state tax bill immediately.

- Check the 3-year clock: If you’re planning on gifting assets to reduce your estate, do it now. The clock starts the moment the transfer is complete.

- Coordinate with your spouse: Make sure you aren't accidentally "wasting" one of your exemptions by having everything titled as "Joint Tenants with Right of Survivorship."

The math in New York is cold. If you're at $7.3 million, your heirs get almost everything. If you're at $7.8 million, the state of New York becomes your biggest beneficiary. It’s a narrow window, and 2026 is the year to make sure you aren't the one falling through it.

Next Steps for NY Residents:

To protect your assets from the 2026 cliff, start by calculating your "augmented" estate value, which includes the face value of all life insurance policies. Once you have that number, speak with an estate attorney specifically about "New York-only" QTIP elections or Credit Shelter Trusts to ensure you are maximizing both the $15 million federal shield and the $7.35 million state exemption without one triggering the other.