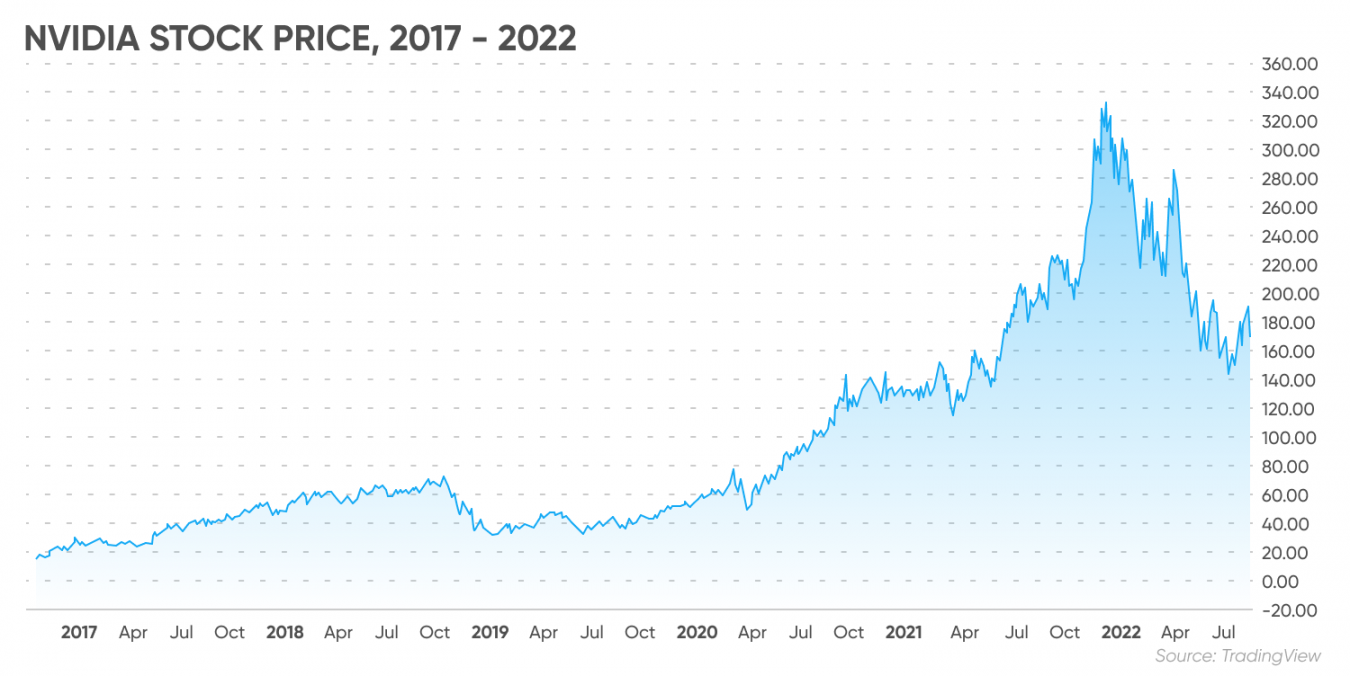

Honestly, if you've been watching the stock price of NVIDIA lately, you’re probably feeling a mix of awe and a tiny bit of vertigo. It’s wild. As of mid-January 2026, we are looking at a company that basically owns the floorboards of the digital world. The stock is hovering around $186, and the market cap is sitting at a mind-numbing $4.5 trillion.

Just think about that.

Three years ago, people were arguing about whether crypto mining was the only thing keeping this company afloat. Now? They are the "tax man" for the entire artificial intelligence revolution. If you want to build a frontier AI model, you pay the NVIDIA tax.

But here’s the thing: most of the chatter you hear on social media or from your cousin who "invests" is sorta missing the real story. Everyone is obsessed with the daily swings, but the real movement is happening in the transition from the Blackwell architecture to the newly announced Rubin platform.

The Blackwell "Speed Bump" and the Rubin Reveal

Back in late 2025, there was all this nervous whispering about Blackwell shipment delays. People thought the party was over. Wrong. By the time Jensen Huang took the stage at CES 2026 earlier this month, it was clear that Blackwell isn't just "ramping up"—it’s essentially sold out for the foreseeable future.

The big shocker, though, was the Rubin platform.

👉 See also: Modern Office Furniture Design: What Most People Get Wrong About Productivity

Named after astronomer Vera Rubin, this new six-chip setup is designed to slash the cost of running AI models by 10x compared to Blackwell. That’s a huge leap. Usually, you see incremental gains, but NVIDIA is moving at a "light speed" cadence now. They aren't releasing new tech every two years anymore; it’s every single year.

This annual release cycle is what keeps the stock price of NVIDIA in that "Strong Buy" territory for analysts like those at Wolfe Research and Jefferies. They see the revenue hitting $170 billion for fiscal 2026. That is a 30% jump over an already record-breaking 2025.

Why $186 Might Actually Be "Cheap"

It sounds crazy to call a $4.5 trillion company cheap.

I get it.

But look at the PEG ratio—price/earnings to growth. It’s sitting around 0.77. In the world of high-growth tech, anything under 1.0 is often considered undervalued. NVIDIA is growing its earnings so fast that the price is actually struggling to keep up with the math.

✨ Don't miss: US Stock Futures Now: Why the Market is Ignoring the Noise

- Data Center Revenue: This is the heart of the beast. It’s about 90% of their business now. In the most recent quarter, they pulled in $51.2 billion just from data centers.

- The China Factor: This has been a massive headache. The U.S. government recently eased up a bit, allowing H200 chips to go to China under "strict conditions." This "thaw" in trade relations is a huge relief for investors who were worried about a $9 billion revenue hole.

- Software Moat: People forget that NVIDIA isn't just a hardware company. Their CUDA software is what developers actually use. You can buy an AMD chip, sure, but if your software doesn't run on it easily, it’s just a paperweight.

The "Other" Guys: Is AMD Catching Up?

You can't talk about the stock price of NVIDIA without mentioning Lisa Su and AMD. At CES 2026, AMD dropped the MI455X, the world’s first 2nm AI GPU. It’s a beast. It has 432GB of HBM4 memory, which is legitimately impressive.

Is it an NVIDIA killer? Probably not. But it’s the first real "open" alternative that hyperscalers like Microsoft and Meta are actually starting to buy in bulk. This competition is healthy, but NVIDIA’s lead in "physical AI" and autonomous robotics is where they are widening the gap.

Jensen Huang is betting the house on "Agentic AI"—AI that doesn't just chat with you but actually does things. We're talking about AI-defined driving in Mercedes-Benz cars and "digital workers" for factories. This isn't science fiction anymore; it’s the Q4 revenue report.

The Risks Nobody Wants to Talk About

Look, it’s not all sunshine and 10x gains.

The lack of diversification is a real "eggs in one basket" situation. If the big cloud players (Microsoft, Google, Amazon) decide they’ve built enough data centers, or if their own custom "in-house" chips finally get good enough, NVIDIA’s growth could hit a wall.

🔗 Read more: TCPA Shadow Creek Ranch: What Homeowners and Marketers Keep Missing

Plus, there's the "DeepSeek" factor. We're seeing more efficient AI models coming out of China that require less compute power. If the world starts needing less hardware to do the same amount of AI work, that’s a direct hit to the stock price of NVIDIA.

Actionable Insights for Your Portfolio

So, what do you actually do with this information?

- Watch the Gross Margins: NVIDIA is aiming for the mid-70% range. If that starts dipping into the 60s, it means they are losing their pricing power to competitors.

- The $250 Target: Most Wall Street analysts have a one-year price target between $250 and $275. If the stock is at $186 now, that’s about a 35-45% upside. But remember, the "low" targets are down around $140.

- Blackwell Shipment Data: Keep an eye on the next two quarterly reports. If they mention any supply chain bottlenecks with TSMC (who makes their chips), expect a short-term pullback.

- Dividends and Buybacks: They just returned $24.3 billion to shareholders. They have plenty of cash to keep the stock price supported even if the market gets shaky.

The bottom line is that the stock price of NVIDIA is no longer just a "tech stock." It's a barometer for the global economy's transition to a compute-based future. Whether you think it's a bubble or the new industrial revolution, you can't afford to ignore it.

Keep an eye on the Rubin ramp-up in the second half of 2026. That will be the moment we know if NVIDIA can maintain its $4 trillion crown or if the gravity of competition finally starts to pull it back to earth.

Next Steps for Investors:

- Review your portfolio's concentration in the "Magnificent Seven" to ensure you aren't over-exposed to a single chip architecture.

- Monitor the upcoming 13F filings to see if institutional giants like BlackRock or Vanguard are increasing or trimming their NVDA positions.

- Set price alerts for the $175 support level, which has historically acted as a strong "buy the dip" floor for institutional buyers.