If you’re running a business in New York, you already know the vibe. It’s expensive. Between the rent in Manhattan and the price of a decent bagel, the "Empire State Tax" is just part of the cost of doing business. But honestly, New York State corporate income tax is a different beast entirely compared to most other states. It’s not just one number. It’s a complex, multi-layered puzzle that catches people off guard every single April.

Most owners think they’ll just pay a flat percentage of their profits. Simple, right? Nope. New York uses a "highest of" system. You basically calculate your tax three different ways, and the state, naturally, takes the biggest slice. It’s like a restaurant that looks at your order and decides to charge you based on the most expensive item on the menu, even if you only ate the salad.

The Three-Headed Monster of New York State Corporate Income Tax

New York doesn't just look at your net income. Under the Article 9-A rules, C-Corporations have to deal with three distinct tax bases. You calculate all of them, and then you pay whichever one is higher.

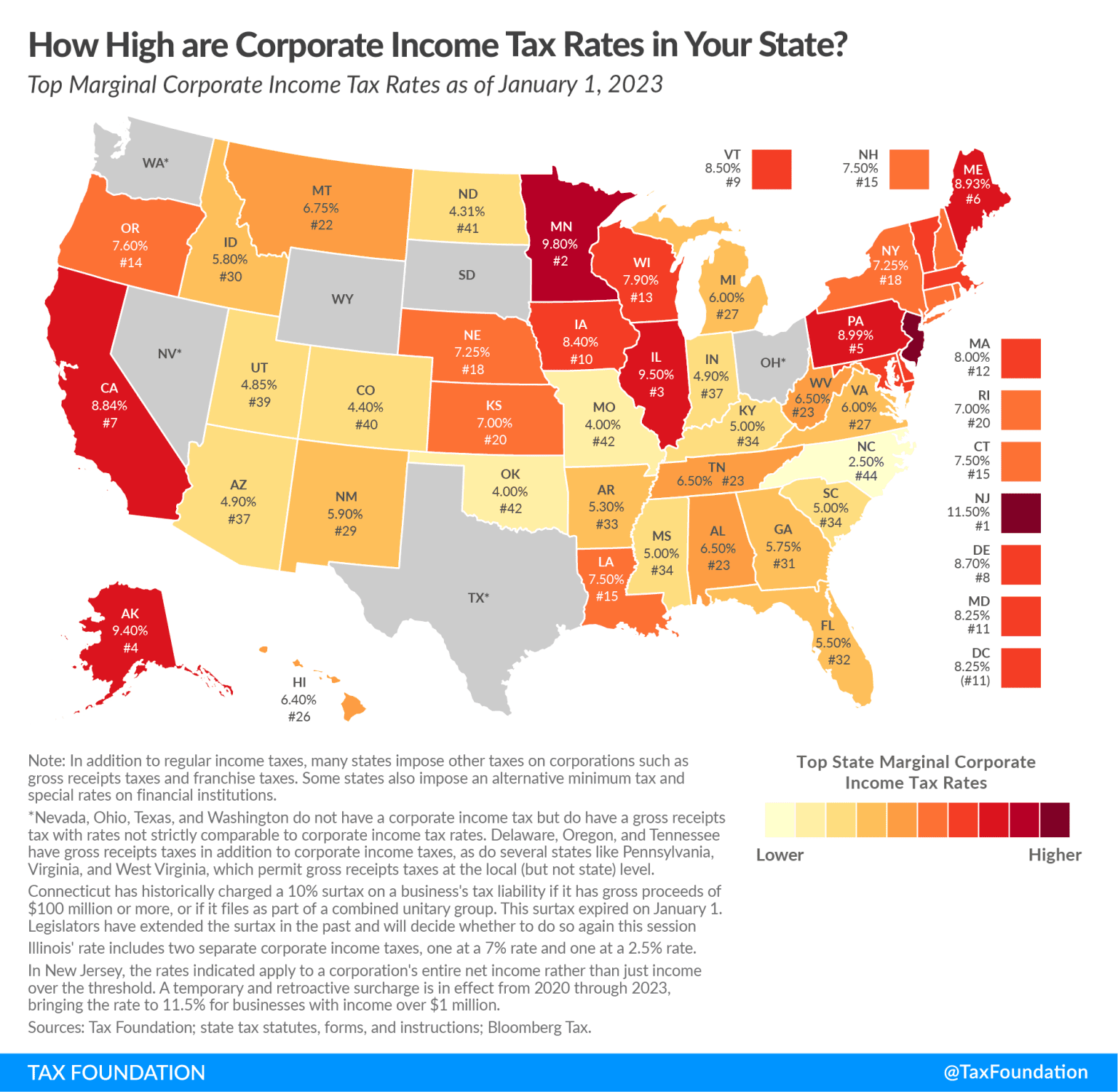

First, there’s the Business Income Base. For most companies, this is the standard 6.5% rate. If you’re a small business with under $5 million in New York income, you might catch a break with a 5% rate, but the rules for qualifying are tighter than a Brooklyn parking spot.

Then you have the Capital Base. This is the one that really stings if you have a lot of assets but didn't make a ton of money this year. It’s a tax on your "business capital"—basically your net worth. The good news? New York has been phasing this out for most non-cooperative housing corporations. The bad news? It’s still there for now, though the rate has been dropping toward zero for many.

Finally, there’s the Fixed Dollar Minimum. Even if your business lost money, even if you didn't sell a single widget, you still owe the state. This amount is based on your New York receipts. If you have over $1 billion in NY receipts, you're looking at a $200,000 bill just for existing. For a small shop with $100,000 in receipts, it's more like $25. It’s a sliding scale that ensures the state gets its cut regardless of your success.

Why the Metropolitan Transportation Business Tax (MTA Surcharge) Ruins Everything

If your business operates in New York City or the surrounding counties like Westchester, Nassau, or Suffolk, you aren't just paying the state. You’re paying the MTA. The Metropolitan Transportation Business Tax Surcharge is essentially a tax on a tax.

🔗 Read more: We Are Legal Revolution: Why the Status Quo is Finally Breaking

It currently sits at 30% of the tax naturally derived from the NYS corporate income tax. So, if your state tax is $10,000, you owe another $3,000 just for the privilege of being near the subway system. This isn't optional. It’s a massive chunk of change that businesses in Buffalo or Albany don't have to worry about.

New York City is a Separate Universe

Here is where it gets truly messy. New York City has its own entirely separate tax department. The NYC General Corporation Tax (GCT) or the Business Corporation Tax (BCT) applies on top of everything else.

If you are a C-Corp in the five boroughs, you are looking at a combined state and city effective rate that can easily hover around 15% to 16%. That is before we even talk about federal taxes. When you see businesses moving to Florida or Texas, it isn’t just the weather. It’s the fact that NYC is one of the few places in America where you are taxed at the federal, state, and city levels simultaneously.

Economic Nexus: You Might Owe Tax Even Without an Office

You don’t need a building in Manhattan to owe New York State corporate income tax. Ever since the Wayfair decision, New York has been aggressive about "Economic Nexus."

Basically, if your business has more than $1.138 million (this number adjusts) in sales to New York customers in a year, you are "in" the system. You have to file. You have to pay. It doesn't matter if you're sitting in a garage in Seattle. If New York residents are buying your software or your handcrafted furniture in large enough quantities, the Department of Taxation and Finance wants their share.

The "Middle-Class" Tax Cut That Actually Happened

Believe it or not, there has been some decent news lately. New York has been slowly lowering the tax rates for "qualified New York manufacturers." If you actually make physical goods in the state, your tax rate on the income base can be as low as 0%.

💡 You might also like: Oil Market News Today: Why Prices Are Crashing Despite Middle East Chaos

Yes, zero.

The state is desperate to keep manufacturing jobs from fleeing to the Rust Belt or overseas. To qualify, you usually need to have property in New York with an adjusted basis of at least $1 million or have all your property and employees located within the state. It’s a huge incentive, but the paperwork to prove you qualify is a nightmare.

Common Mistakes That Trigger Audits

The New York Department of Taxation and Finance is famously efficient. They have some of the most sophisticated data-matching systems in the country.

One big mistake? Inconsistent Apportionment. New York uses a "Single Sales Factor." This means they only care about where your customers are, not where your employees or machines are. If you tell the feds one thing and New York another regarding where your sales are coming from, a red flag goes up immediately.

Another one is the Investment Capital trap. New York changed the rules a few years ago on how investment income is taxed. It used to be much more favorable. Now, unless you meet very specific "referable to" criteria, that passive income is often taxed at the full business rate.

Pass-Through Entities and the SALT Cap Workaround

We can't talk about corporate tax without mentioning the Pass-Through Entity Tax (PTET). This was New York's genius move to help business owners get around the federal $10,000 limit on State and Local Tax (SALT) deductions.

📖 Related: Cuanto son 100 dolares en quetzales: Why the Bank Rate Isn't What You Actually Get

If you run an S-Corp or a Partnership, the entity can choose to pay the tax at the corporate level. The business gets a federal deduction, and the individual partners get a credit on their personal NYS tax returns. It’s a win-win, but it’s an annual election. If you miss the deadline—usually March 15th—you are out of luck for the entire year. Kinda brutal, but that's the law.

The Reality of Credits and Incentives

New York offers a ton of credits, but they are very specific.

- The Film Production Credit (why every movie seems to be shot in Brooklyn now).

- The Excelsior Jobs Program.

- Brownfield Redevelopment credits for cleaning up polluted land.

Most of these require pre-approval. You can't just claim them on your return and hope for the best. You need a certificate from a state agency like Empire State Development.

How to Handle the Paperwork

You’re going to be looking at Form CT-3. It’s the standard return for General Business Corporations. If you're part of a combined group, it's CT-3-A.

The instructions for these forms are hundreds of pages long. Honestly, unless you’re a glutton for punishment, this isn't a DIY project. The way New York handles "Market-Based Sourcing"—determining exactly where a service is "delivered"—is incredibly subjective. If you sell a subscription to a guy in New Jersey who uses the app while commuting into Penn Station, who gets the tax? New York has very specific (and often aggressive) answers to those questions.

Actionable Steps for Business Owners

Don't wait until April to figure this out. The New York State corporate income tax system is built on "estimated" payments. If you haven't been paying in throughout the year, the penalties and interest will eat your lunch.

- Check your Nexus yearly. If your out-of-state sales are creeping toward that $1 million mark, start planning for a New York filing requirement now.

- Evaluate the PTET Election. If you aren't a C-Corp, talk to your CPA about the Pass-Through Entity Tax. It is arguably the biggest tax-saving tool available to New York business owners right now.

- Review your "Sourcing" logic. If you provide services, document why you believe a sale happened in New York or outside of it. If you get audited, the burden of proof is on you, not the state.

- Watch the MTA Surcharge. If you are expanding into the "MCTD" (Metropolitan Commuter Transportation District), factor that 30% surcharge into your overhead. It changes the math on profitability significantly.

- Separate City and State. Remember that NYC and NYS are two different tax collectors. Paying one doesn't mean you've satisfied the other. Double-check your NYC general corporation tax filings if you have a physical presence in the city.