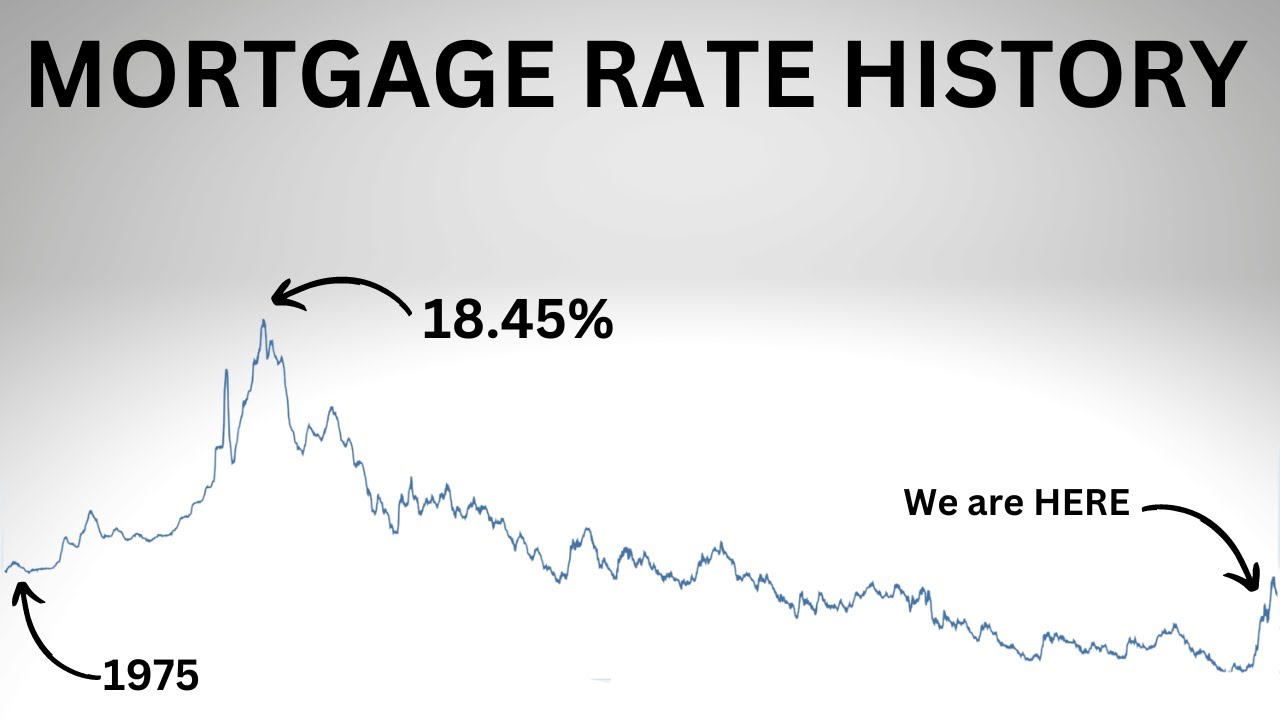

It feels like a lifetime ago, but back in 2016, you could snag a 30-year fixed mortgage for about 3.6%. People complained then. They thought rates were "creeping up" from the record lows of 2012. If only they knew. Looking at mortgage rates past 10 years, we aren’t just looking at a line graph; we are looking at the complete disintegration and subsequent rebuilding of the American dream’s price tag.

Rates are weird. Honestly, they don't always follow the logic we think they should. You’d assume that if the economy is doing great, rates stay low to keep the party going, but it’s usually the exact opposite.

The last decade has been a total fever dream for anyone trying to sign a deed. We went from the "lower for longer" era of the mid-2010s into a pandemic-induced floor where money was basically free, and then slammed into a wall of inflation that sent us spiraling toward 8% in late 2023. It wasn't a slow climb. It was a vertical jump.

The 2015 to 2019 era: The "Normal" we forgot

Before the world turned upside down, mortgage rates were actually pretty boring. In 2015, the average 30-year fixed rate hovered around 3.85%. It was a time of gradual healing. The Great Recession was in the rearview mirror, but the Federal Reserve was terrified of raising rates too fast and breaking the fragile recovery.

Janet Yellen was at the helm of the Fed then. They started "normalizing" interest rates, which pushed mortgage costs up toward 4.5% or even 5% by late 2018. I remember people panicked. 5% felt like an insult after years of 3%. Sellers started getting nervous. But then, 2019 hit, and the economy started showing cracks. The Fed pivoted. They started cutting. By the end of 2019, we were back down in the high 3s. Little did we know, the "floor" was about to fall out entirely.

That 3% mental trap

Then came 2020. Everything stopped.

To prevent a total global collapse, the Federal Reserve started buying Mortgage-Backed Securities (MBS) like crazy. They dumped trillions into the market. By January 2021, the average 30-year fixed rate hit an all-time floor of 2.65% according to Freddie Mac.

2.65 percent.

That single number changed everything. It created a "lock-in" effect that we are still dealing with today. If you bought a house or refinanced in 2021, you are likely sitting on a rate that starts with a 2 or a 3. Why would you ever sell? If you sell that house and buy a new one today, your monthly payment might double for the exact same loan amount. This is why inventory is so low. People are essentially "married" to their 2021 mortgages. It's a golden handcuff.

The Great Spike of 2022-2023

Inflation wasn't "transitory." When the Fed realized they were behind the curve, they started hiking the federal funds rate at the most aggressive pace since the Volcker era of the 1980s. While the Fed doesn't directly set mortgage rates, they influence the 10-year Treasury yield, which is the benchmark mortgage lenders track.

In March 2022, you could still get a rate around 3.8%. By October 2022, we were looking at 7%.

It happened so fast that buyers were getting priced out in the middle of their home searches. You’d get pre-approved for a $500,000 home on a Tuesday, and by the following Monday, your budget had dropped to $420,000 because the rate jumped half a point. It was brutal. By October 2023, the 30-year fixed rate briefly kissed 8% for the first time in two decades.

Why the spread matters more than the rate

If you want to sound smart at a dinner party, talk about "the spread." Usually, mortgage rates stay about 1.7 or 1.8 percentage points above the 10-year Treasury yield. Over the mortgage rates past 10 years, this gap was fairly consistent.

But lately? The spread blew out to nearly 300 basis points (3%).

Lenders became terrified of volatility. If they lend you money at 6% today, but rates jump to 8% tomorrow, the value of that loan on the secondary market drops. To protect themselves, they charged a premium. This means even when Treasury yields started to drop, mortgage rates stayed stubbornly high. We are finally seeing that spread compress a bit in 2025 and 2026, but it's a slow process.

Real talk: The 7% hurdle

We’ve spent the last couple of years oscillating between 6.5% and 7.5%. For a generation of buyers who grew up seeing 3% on TV commercials, 7% feels like a tragedy. But if you look at the 50-year average, it's actually quite normal. The problem isn't just the rate; it's the rate combined with home prices that doubled in some markets during the pandemic.

$400,000 at 3% is a $1,686 monthly payment (principal and interest).

$400,000 at 7% is a $2,661 monthly payment.

That’s a thousand dollars extra every month just to the bank. No extra bedrooms. No bigger backyard. Just interest. This is the reality of the current landscape.

What actually drives these shifts?

It’s not just one thing. It’s a mess of moving parts.

- The Fed's Balance Sheet: When the Fed stops buying mortgage bonds, rates go up. They’ve been in "quantitative tightening" mode for a while now, letting those bonds roll off.

- Inflation Expectations: If investors think inflation is going to stay sticky at 3% or 4%, they demand higher yields on long-term debt.

- Global Instability: Sometimes, when the rest of the world is in chaos, people buy U.S. Treasuries as a "safe haven." This drives prices up and yields down, which can actually help mortgage rates.

- The Job Market: A "too hot" labor market usually means the Fed keeps rates higher for longer to cool things down.

The Refinance Myth

A lot of people bought in 2023 and 2024 with the mantra "Marry the house, date the rate." The idea was that you'd just refinance when rates inevitably dropped back to 4%.

Here is the cold truth: We might not see 4% again for a long time.

The era of 2% and 3% was an anomaly. It was a response to a once-in-a-century pandemic and a decade of sluggish post-2008 growth. In a healthy, growing economy with 2% inflation, a "normal" mortgage rate is likely somewhere between 5.5% and 6.5%. If you are waiting for 3.5% to buy a home, you might be waiting for a decade. Or longer.

Actionable steps for the current market

If you are looking at the history of mortgage rates past 10 years and feeling discouraged, you have to change your strategy. The old rules don't apply.

First, fix your credit score like it’s your job. In a high-rate environment, the "gap" between someone with a 680 score and a 780 score is massive. It can be the difference between a 7.2% and a 6.4%. On a $400,000 loan, that's tens of thousands of dollars over the life of the loan.

Second, look into ARMs (Adjustable-Rate Mortgages). They got a bad rap after 2008, but they aren't the same "exploding" loans they used to be. A 7/1 ARM might offer a rate significantly lower than a 30-year fixed. If you know you’re going to move in five or six years anyway, why pay the premium for a 30-year guarantee?

Third, shop small. Everyone goes to the big national banks or the famous online lenders. Often, local credit unions keep their own loans on their books rather than selling them to Wall Street. Because they aren't as worried about the secondary market, they can sometimes offer rates half a point lower than the big guys.

Finally, negotiate for a seller buy-down. Instead of asking a seller to drop the price by $10,000, ask them to credit you $10,000 to buy down your interest rate. This "2-1 buy-down" can drop your rate by 2% in the first year and 1% in the second year, giving you breathing room while you wait for a permanent refinance opportunity.

🔗 Read more: Tesla Stock: What Most People Get Wrong About the Elon Musk Factor in 2026

The market is volatile. It’s frustrating. But history shows us that while rates change, the best time to buy real estate is usually when you can actually afford the monthly payment—regardless of what the "average" is on the news. Don't try to time the bottom of the rate cycle. Nobody has a crystal ball, and by the time rates drop significantly, competition will skyrocket, and home prices will likely jump again. Focus on the math of today.

Key Takeaways to Remember:

- The 2% rates of 2021 were a historical fluke, not a standard to wait for.

- Credit scores matter more now than they did during the "cheap money" era.

- Seller credits for rate buy-downs are often more valuable than price cuts.

- Inventory remains low because millions of homeowners are "locked in" to low rates from the past decade.

Immediate Next Steps:

- Run a "Rate Sensitivity" check: Calculate your maximum monthly payment at 6.5%, 7%, and 7.5% to see where your breaking point is before you start touring homes.

- Get a "Soft Pull" credit report to identify any errors that could be dragging your score down by 20-30 points.

- Research local credit unions in your specific zip code to compare their portfolio lending rates against national averages.