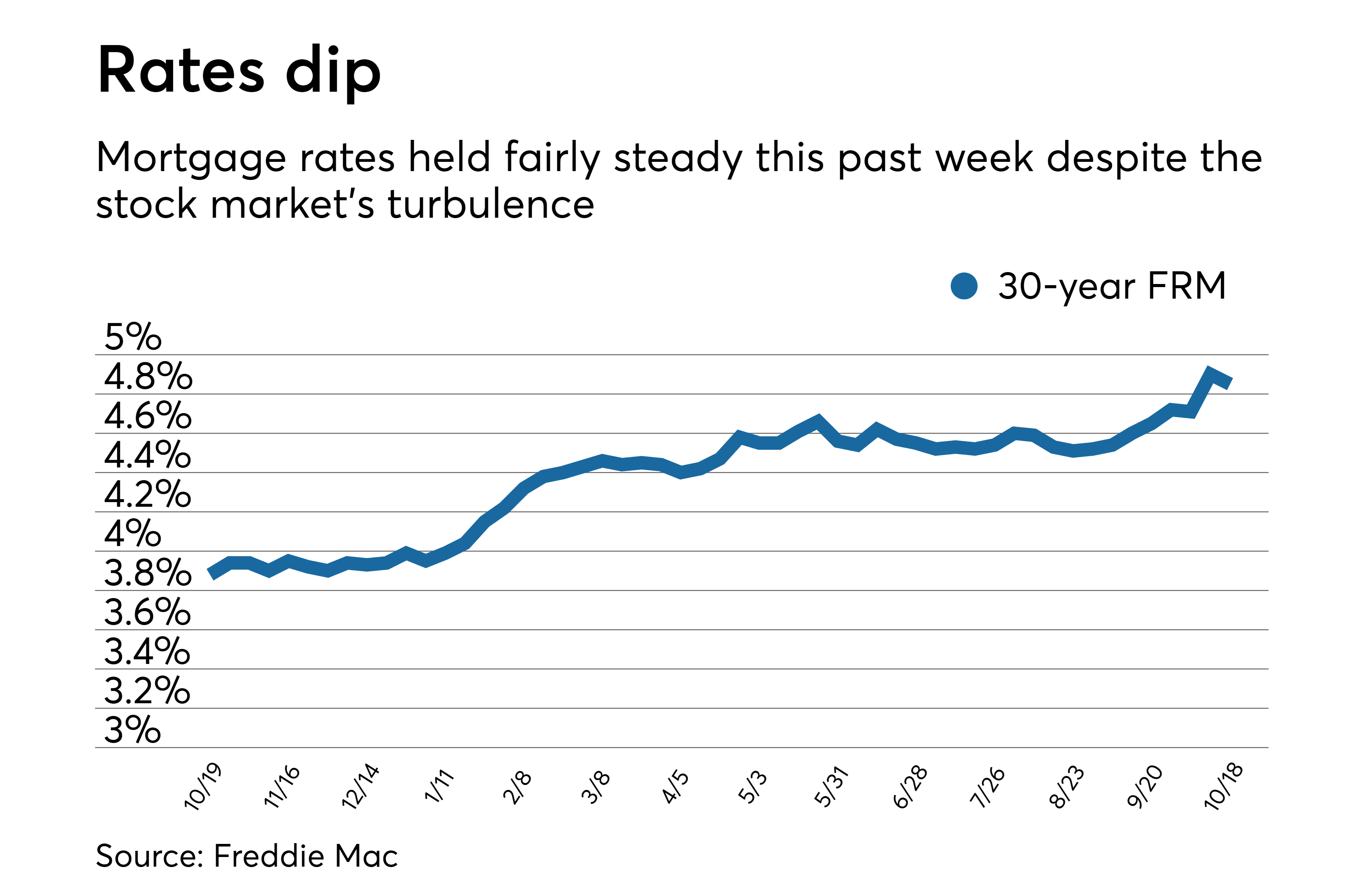

If you’ve been refreshing your browser every ten minutes hoping for a miracle, I have some news. It’s not a miracle, but it’s definitely a shift. Mortgage rate this week has become the obsession of every person with a Zillow tab open, and honestly, the noise is deafening. You hear "rates are dropping" on one news cycle and "inflation is sticky" on the next. It’s exhausting.

The reality? We are seeing a 30-year fixed rate hovering right around the 6.7% to 6.9% mark, depending on who you ask and how much you’re willing to pay in points. Freddie Mac’s latest Primary Mortgage Market Survey shows a slight cooling, but don't go popping the champagne just yet. It’s a game of inches. A few basis points here, a tenth of a percent there. It matters, sure. But it’s not the 3% era coming back to save us.

The Fed and the "Vibe Shift" in Lending

Everyone blames the Federal Reserve. It's the easy thing to do. While Jerome Powell doesn’t sit in a room and manually turn a dial labeled "Mortgage Rates," his words move the 10-year Treasury yield like a marionette. When the 10-year yield climbs, your monthly payment climbs. Simple as that.

The market is currently reacting to the "higher for longer" sentiment that has been echoed by Fed officials like Christopher Waller. He’s been pretty vocal about not rushing into rate cuts. Why? Because the labor market is still weirdly strong. People are still spending money. When people spend, inflation stays stubborn. When inflation stays stubborn, lenders get nervous and keep rates high to protect their margins.

Why the 10-Year Treasury Yield is Your Real North Star

Forget the federal funds rate for a second. If you want to know what’s happening with the mortgage rate this week, look at the 10-year Treasury. There is usually a "spread" or a gap of about 250 to 300 basis points between the 10-year yield and the 30-year fixed mortgage.

Historically, this gap was closer to 170 basis points. It’s wider now because of volatility. Banks are scared of being stuck with low-interest loans if the market shifts again, so they charge you a premium for that risk. If that spread narrows—even if the Fed does nothing—rates could drop. But that requires stability. And stability is currently in short supply.

Stop Waiting for 3% (It's Not Coming)

I see this all the time. People sitting on the sidelines, waiting for the "good old days" of 2021.

That was an anomaly. A black swan event.

The historical average for mortgage rates over the last 50 years is actually closer to 7.7%. In that context, the mortgage rate this week looks... okay? Sorta. It’s definitely better than the 18% people were paying in the early 80s, though that's cold comfort when home prices are at record highs. We are in a "new normal" where 6% is the new 3%. Once you accept that, your house hunting strategy changes completely. You stop looking for a deal on the interest and start looking for a deal on the purchase price.

The Inventory Trap

High rates have created a "lock-in effect." You've probably heard of it. Your neighbor has a 2.75% rate and they aren't moving unless they absolutely have to. This keeps inventory low. Low inventory keeps prices high. It’s a vicious cycle that makes the mortgage rate this week feel even more painful because you're paying a high rate on a high principal.

How to Actually Get a Lower Rate Right Now

You aren't stuck with the headline number you see on the news. Lenders are hungry for business because loan volume is down. This gives you leverage.

- The 2-1 Buydown: This is a killer strategy if you think rates will drop in two years. The seller pays to lower your rate by 2% the first year and 1% the second. It gives you breathing room.

- Adjustable-Rate Mortgages (ARMs): I know, I know. ARMs have a bad reputation from 2008. But a 5/1 or 7/1 ARM can offer a significantly lower rate than a 30-year fixed. If you plan to move or refinance within five years, it's a smart play.

- Credit Score Alchemy: A jump from 680 to 740 can save you half a percent. That's thousands over the life of the loan.

- Local Credit Unions: Often, these smaller institutions keep loans on their own books rather than selling them to Fannie Mae. This means they can be more flexible with the mortgage rate this week than the big national banks.

Is This the Week to Lock?

This is the million-dollar question. If you are under contract, the "lock or float" debate is gut-wrenching.

If you see a dip on Tuesday, take it.

Market volatility means that a "good" rate today could disappear by Thursday afternoon. We saw this recently when a hotter-than-expected Consumer Price Index (CPI) report sent rates soaring in a matter of hours. If the numbers work for your budget today, lock it. Don't gamble your future home on the hope of a 0.125% drop that might never come.

The Role of Servicing Rights

Something most people don't talk about is Mortgage Servicing Rights (MSRs). When a bank gives you a loan, they often sell the right to collect your payments to someone else. The value of these rights fluctuates with interest rates. When rates are expected to stay high, these rights are more valuable. This affects how aggressively a lender will price your loan. It’s a hidden layer of the industry that dictates why one bank might give you 6.625% while another insists on 7%.

Real World Example: The "Cost of Waiting"

Let’s look at a $400,000 home.

If you buy now at 6.8%, your principal and interest is roughly $2,600.

If you wait six months and rates drop to 6.3%, but the home price increases to $420,000 because of increased competition, your payment is... $2,600.

👉 See also: 1 us dollar into ghana cedis: Why the Rate Is Moving So Fast Right Now

You waited, you stressed, and you ended up with the same payment but less equity. This is the trap. The mortgage rate this week is only one part of the math. You have to look at the total cost of acquisition.

Actionable Steps for Borrowers Today

- Get a "Loan Estimate" from at least three lenders. Don't just check the rates; check the "Section A" fees. That's where they hide the profit.

- Ask about "Float Down" options. Some lenders let you lock a rate but "float down" if rates drop significantly before you close. It’s the best of both worlds.

- Ignore the "No Closing Cost" trap. There is no such thing as a free lunch. "No closing cost" usually just means they’ve baked the fees into a higher interest rate. Do the math on how long you plan to stay in the house to see if paying points upfront makes sense.

- Watch the Jobless Claims report. Every Thursday morning, this data comes out. If unemployment starts to tick up, rates usually tick down. It's a grim correlation, but it's the reality of the bond market.

- Clean up your debt-to-income (DTI) ratio. Pay off that credit card or car loan. Lenders are tightening their belts, and a lower DTI can sometimes get you into a better "pricing bucket" for your interest rate.

The bottom line is that the mortgage rate this week is a snapshot in a very long, very complicated movie. It’s not the whole story. You can't control the Fed, and you can't control the global bond market. You can control your credit score, your down payment, and your choice of lender. Focus on those. The market will do what it does, but being prepared means you won't get caught in the rain when the numbers shift again.

Stop overthinking the daily fluctuations and look at the monthly trend. Right now, the trend is sideways. It’s boring, it’s frustrating, but it’s the reality of the 2026 housing market. Get your pre-approval in order, keep your documents ready, and be prepared to move fast when you find the right house, regardless of whether the rate is 6.7% or 6.8%. In five years, that tiny difference won't matter nearly as much as the house you're living in.