You've probably heard the rumors. Maybe you’ve even seen the headlines screaming about a massive crash in borrowing costs. Honestly, if I had a dollar for every time someone told me rates were "guaranteed" to hit 4% by next Tuesday, I’d probably be able to buy a house in cash and skip this whole mess entirely.

But we have to talk about reality.

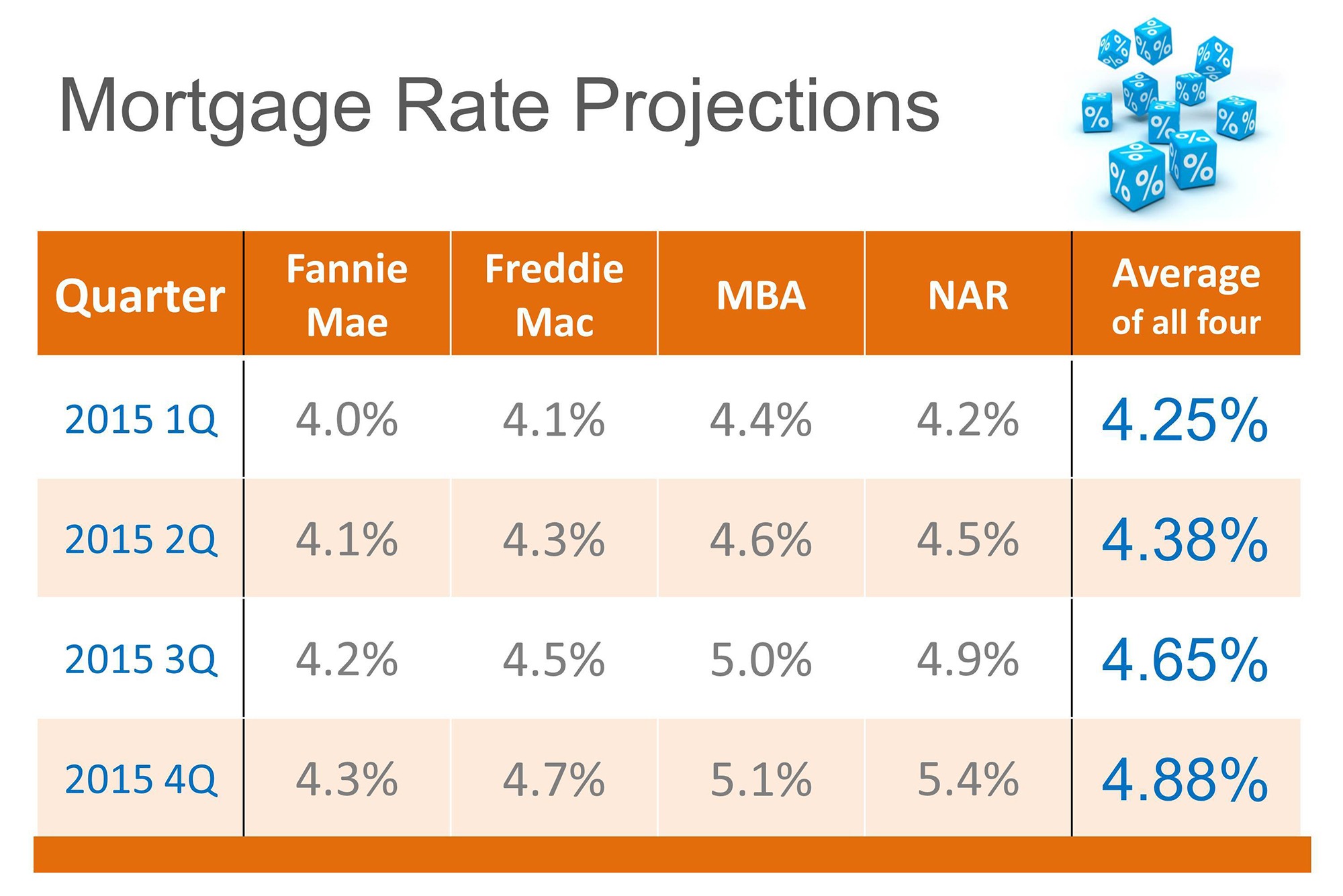

As we move through the early stages of 2026, looking back at the chaos of 2025 gives us a pretty clear roadmap. The truth about mortgage rate predictions 2025 is that they didn't quite deliver the "rescue" many families were praying for, but they didn't leave us stranded in the wilderness either. It’s been a year of "sideways" movement—a sort of financial purgatory where rates aren't high enough to stop all sales, but they aren't low enough to make anyone feel like they're getting a bargain.

The 6% Psychological Barrier

Most experts spent the last twelve months obsessed with the number six. Why? Because for most modern buyers, 6% is the line in the sand. When rates flirted with 7.04% in early 2025, the market basically pulled a disappearing act. Buyers stayed home. Sellers clutched their 3% COVID-era rates like heirlooms.

Then things started to shift.

By the end of 2025, the national average for a 30-year fixed mortgage settled around 6.18%, according to Freddie Mac. It was a victory, sure, but a small one. It felt like winning a participation trophy when you were expecting a gold medal.

Fannie Mae’s Economic and Strategic Research Group has been tracking this trend closely. Their data suggests that while we ended 2025 at that mid-6% range, the actual relief is a slow burn. We are looking at a forecast that suggests 5.9% might be the "new normal" as we head deeper into 2026.

Why the Fed isn't the only boss

There’s this common misconception that Jerome Powell sits at a desk with a giant dial labeled "Mortgage Rates" and just turns it down when he’s feeling generous.

It doesn't work like that.

The Fed controls the federal funds rate—the short-term stuff. Mortgage rates, however, take their cues from the 10-year Treasury yield. And the 10-year Treasury is a nervous creature. It reacts to everything: inflation reports, jobs data, and even the massive amount of federal debt the U.S. is currently carrying.

Brad Hunter from Hunter Housing Economics has been pretty vocal about this. He’s argued that mortgage rates haven't fallen as fast as people wanted because the sheer volume of government debt keeps upward pressure on those long-term yields. Basically, if the government is borrowing trillions, it has to pay a decent interest rate to attract investors, which keeps your home loan rate pinned higher than you'd like.

Who actually won in 2025?

If you were a "rate shopper" in 2025, you probably found some brief windows of opportunity. It wasn't a year of steady decline; it was a year of "dips."

In late October 2025, for example, we saw a brief slide to 6.25%. People who were ready—meaning they had their pre-approvals locked and their paperwork in a neat digital pile—jumped on it. The Mortgage Bankers Association (MBA) reported that refinance applications surged during these tiny windows.

It’s a different game now.

You aren't waiting for a "return to normal" because 3% was never normal. It was an anomaly. A glitch in the matrix caused by a global pandemic. Realistically, an expert like Lawrence Yun from the National Association of Realtors (NAR) points out that we are transitioning into a period where stability matters more than the specific number. If rates stay between 6% and 6.4%, people can finally plan.

The Refinance Trap

I see a lot of people sitting on 7.5% loans from the 2023 peak just waiting for the magic 5% to appear.

🔗 Read more: When Do We Stop Paying Taxes on Overtime: The Truth About Your Extra Hours

Don't wait for perfection.

If you can shave 1% off your rate in the current climate, it’s usually worth running the numbers. The "break-even" point—the moment where the monthly savings cover the closing costs—is coming much faster than it used to because home values have stayed surprisingly high.

The Inventory Problem Nobody Talks About

We can talk about mortgage rate predictions 2025 until we're blue in the face, but rates don't exist in a vacuum. The real story is the "lock-in effect."

Roughly 80% of current mortgage holders have a rate below 5%. Even with rates dipping toward 6%, the math of moving just doesn't add up for a lot of people. Why trade a $2,000 payment for a $3,500 payment just to get an extra bedroom?

This is why existing-home sales hit a 30-year low in 2024 and only crawled back slightly in 2025.

However, we are seeing a shift in new construction. Builders are the ones actually moving the needle. Because they aren't "locked in" to a previous rate, they can offer incentives. Throughout 2025, we saw builders buying down rates into the 5s for their customers. If you're looking for the best "actual" rate, you're often finding it in a new-build community rather than a 1970s ranch house down the street.

🔗 Read more: GSG Dallas TX: What Really Happened to the Graphic Solutions Group

Regional Weirdness

It’s also worth noting that "national averages" are kinda useless if you live in a place like Houston or Raleigh.

In some markets, inventory is actually rising. The MBA notes that as inventory loosens, the pressure on buyers eases. You might be paying 6.2%, but you aren't in a 20-person bidding war that forces you to waive your inspection and offer your firstborn. That’s a trade-off many are finally willing to make.

What should you actually do now?

If you're staring at the market today, the "wait and see" strategy is starting to lose its luster. Here is the move:

First, get a "soft" quote from a couple of lenders to see where you actually stand. National averages are for headlines; your credit score and debt-to-income ratio are for reality.

Second, look at the spread. The gap between the 10-year Treasury and the 30-year mortgage rate has been historically wide (around 250 to 300 basis points). As that spread "compresses" or gets back to the historical average of about 170 basis points, mortgage rates could drop even if the Fed does nothing.

Third, watch the jobs report. Mortgage rates love a "bad" jobs report. If the labor market cools, rates usually follow.

Actionable steps for the next 90 days:

- Check your "Rate-Buy-Down" Math: Sometimes paying points upfront makes sense if you plan to stay in the home for 7+ years. In a 6% environment, a 1-point buy-down can be the difference between "ouch" and "okay."

- Monitor the 10-Year Treasury: You don't need to be a Wall Street trader, but if you see that yield dropping toward 3.75%, call your loan officer immediately.

- Ignore the "Crashed Market" YouTubers: They’ve been predicting a 2008-style collapse for four years. It hasn't happened because lending standards today are infinitely stricter than they were twenty years ago.

The era of easy money is over, but the era of "predictable" money is finally starting. If you can afford the payment at 6.2%, buy the house. You can always marry the house and date the rate—refinancing is a tool, not a myth. Just make sure the math works today, not in some hypothetical 2027 future.

Next Steps for You:

Check your current credit score to see if you qualify for the lowest tier of the forecasted 6% rates. If you're currently in a loan above 7.25%, reach out to a lender to run a "break-even" analysis on a refinance to 6.1%.