The dream of a 3% mortgage is dead. Kinda harsh, right? But if you’re waiting for the pandemic-era basement rates to come back before you buy a house, you might be waiting until your kids are in college. Honestly, the mortgage rate forecast 2026 is looking a lot less like a "crash" and a lot more like a "stretching out" on a very comfortable, albeit slightly higher, couch.

We’ve all spent the last few years watching the Federal Reserve like hawks. Every time Jerome Powell sneezed, the 30-year fixed rate seemed to jump or dive by half a point. It was exhausting. But as we head into 2026, the vibe is shifting. We aren't in the "emergency" phase of the economy anymore. We're in the "settling in" phase.

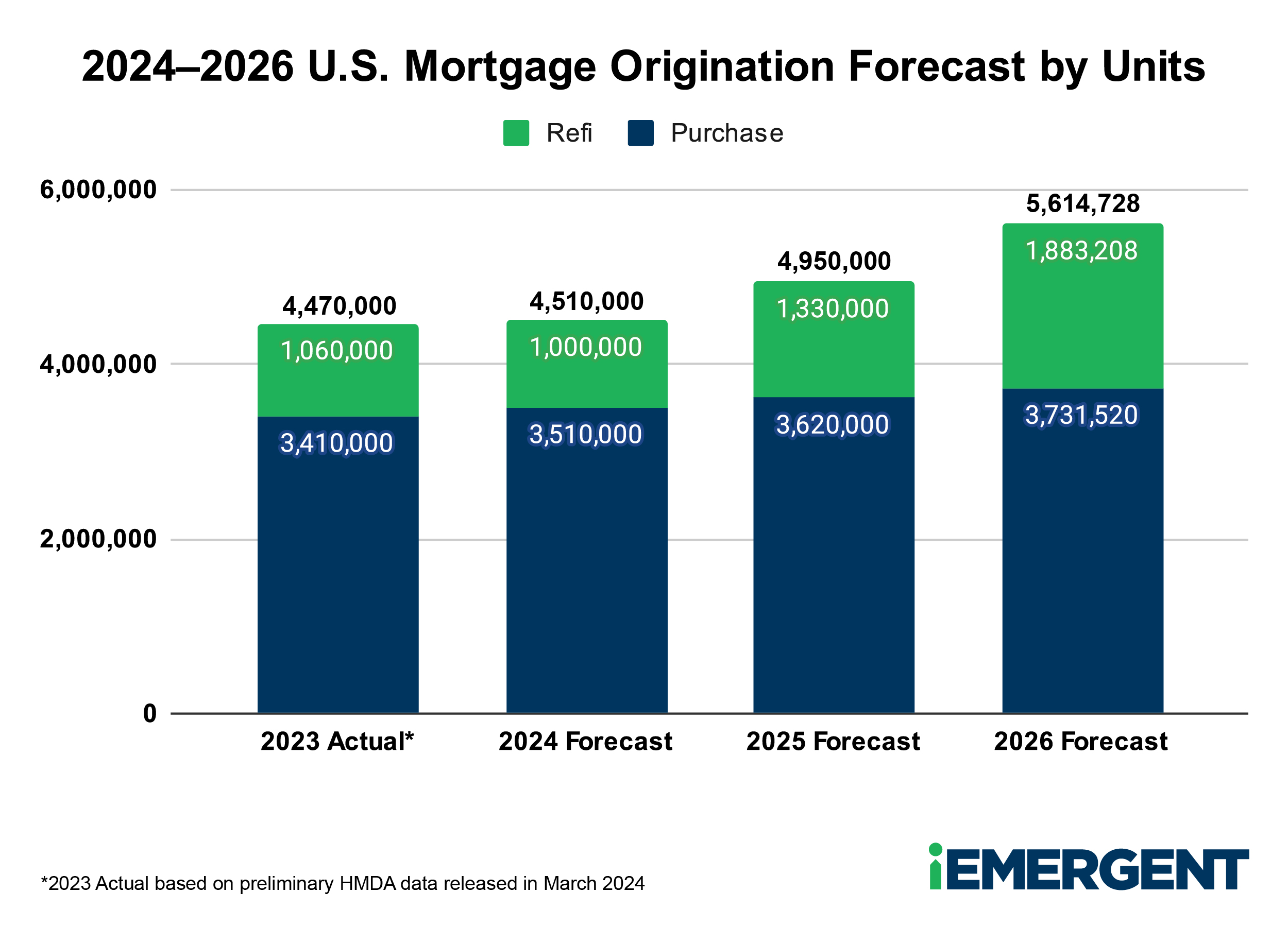

The 6% Floor: Why Rates Aren't Plummeting

Most experts, from the folks at Fannie Mae to the Mortgage Bankers Association (MBA), are clustering their 2026 predictions around the 6% mark. Specifically, Fannie Mae is eyeing a drop to about 5.9% by the end of 2026. Meanwhile, the MBA is a bit more conservative, sticking closer to 6.4%.

Why the gap? It comes down to what people call "the spread."

📖 Related: How Much Do Delivery Drivers Make? The Reality vs the App Screenshots

Usually, mortgage rates track the 10-year Treasury yield with a gap of about 1.7 percentage points. Lately, that gap has been huge—more like 2.5 points—because banks are nervous about volatility. In 2026, if the economy stays boring (which, for once, would be great), that spread should shrink. That's how we get lower rates even if the Fed doesn't slash its own rates to zero.

Basically, 6% is the new 4%.

What Really Happens if Rates Hit 5.8%?

You’d think a drop from 7% to 5.8% would be a victory lap for buyers. Not necessarily.

When rates dip, everyone who was "waiting on the sidelines" suddenly rushes the field at the same time.

💡 You might also like: USD to BDT Exchange Rate Today: Why the Market is Acting So Weird

Rich Martin, a director at Curinos, recently pointed out that lower rates often just drive up competition. If your monthly payment drops by $200 because of a better rate, but the house price jumps $30,000 because ten other people are bidding on it, did you actually win? Probably not.

The Real Numbers for 2026

- National Association of Realtors (NAR): Expecting an average of 6.0%.

- Wells Fargo: Predicting roughly 6.18%.

- Morgan Stanley: The optimists in the room, hinting at 5.75% by mid-year.

- Zillow: Standing firm that we won't see anything below 6.0% all year.

The "Lock-in" Effect is Finally Thawing

For years, people with 3% mortgages refused to move. Why would they? Swapping a 3% loan for a 7% loan is a bad math problem. But by 2026, life happens. People have kids. People get divorced. People retire.

We’re seeing a "structural thaw." The NAR predicts existing home sales could jump as much as 14% in 2026. That’s not because the rates are "low," but because they are "stable." People can finally plan their lives again without worrying that rates will hit 8% by the time they close.

Why the Fed Might Throw a Wrench in the Works

The Federal Reserve is expected to keep trimming rates, but they’re moving like a cautious turtle. Goldman Sachs expects the Fed to hit a "terminal rate" (their stopping point) of around 3.25% in 2026.

But there’s a catch.

If inflation stays "sticky"—meaning the price of eggs and car insurance stays high—the Fed will stop cutting. Or, if the government keeps running massive deficits, bond investors might demand higher yields, which keeps your mortgage rate high even if the Fed is trying to help. It's a tug-of-war where the homeowner is the rope.

Real Talk: Should You Buy Now or Wait for 2026?

If you're looking for a specific "buy" signal, don't look at the mortgage rate forecast 2026. Look at your own bank account.

Waiting for a 5.5% rate that might only last for three weeks in October is a stressful way to live. Plus, Realtor.com expects home prices to keep ticking up—about 2.2% over the year. In many markets, the price growth will eat up any savings you get from a slightly lower interest rate.

💡 You might also like: Same Day Shipping Amazon: Why Your Package Might Not Arrive by Dinner

Actionable Steps for 2026 Borrowers

- Watch the 10-Year Treasury, not just the Fed. If you see that yield dropping toward 3.5%, mortgage rates will follow.

- Focus on the "Monthly Payment" threshold. Most experts say the market "unlocks" when the typical payment falls below 30% of the median income. We’re finally hitting that point in early 2026.

- Check for "Rate Buydowns." Builders are still desperate to move new inventory. Many are offering "2-1 buydowns" that give you a 4% or 5% rate for the first few years, regardless of what the national average is.

- Get your credit score above 760. In a 6% world, the "best" rates are reserved for the cleanest files. A 20-point difference in your score could save you $150 a month in this environment.

The 2026 market is going to be about normalization. It won't be the wild west of 2021, and it won't be the frozen tundra of 2023. It’s just... a market. And for most people, that's actually the best news we've had in years.

Next Steps for You

- Calculate your "Break-even": Use a mortgage calculator to see if a 0.5% rate drop actually saves you more than a 3% price increase would cost you.

- Get a Pre-Approval Refresh: If you haven't talked to a lender since last year, your borrowing power has likely changed significantly due to wage growth and stabilizing rates.

- Monitor Local Inventory: National forecasts are great, but if you're in a high-growth city like Houston or Phoenix, supply is increasing faster than the national average, giving you more leverage as a buyer.