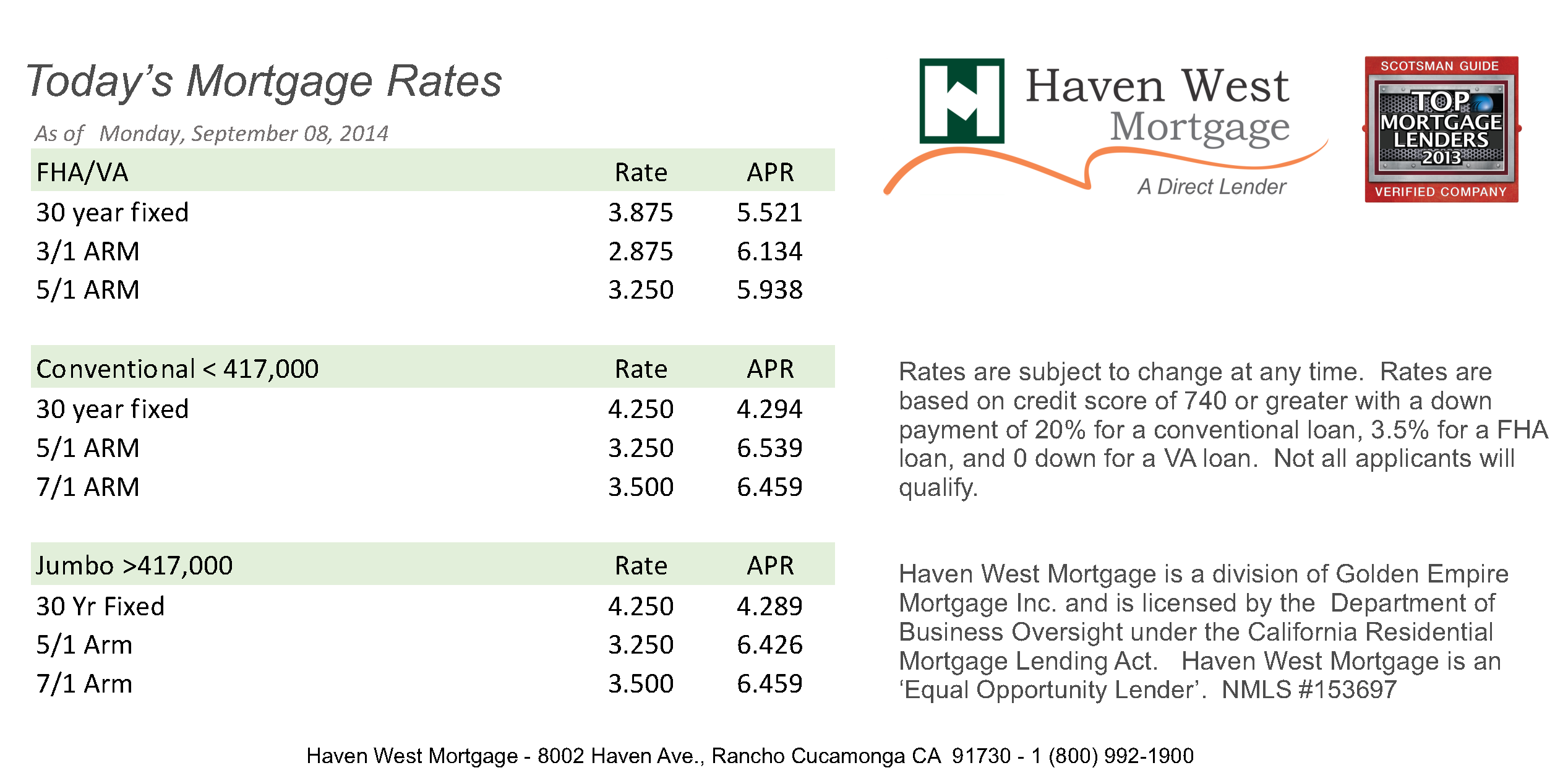

It is Saturday, January 17, 2026. If you woke up this morning and checked your banking app or Zillow, you probably saw a number that felt weirdly familiar yet slightly unsettling.

For the first time in what feels like a decade—but has actually only been about three years—we are staring at a 30-year fixed rate that is flirting with the high 5s.

Honestly, it’s a bit of a mind-bender.

What are mortgage interest rates today?

As of today, January 17, 2026, the national average for a 30-year fixed mortgage is sitting right around 6.11%.

Some lenders, like Zillow, are actually quoting a bit lower at 5.99%, while others are still hovering at 6.18% depending on the fees they’re baking in. If you’re looking at a 15-year fixed mortgage, you’re looking at roughly 5.47%.

It’s the lowest we’ve seen these numbers since the tail end of 2022.

But here’s the kicker: just because the "rate" is 5.99% doesn't mean that's what you pay. You’ve gotta look at the APR, which is closer to 6.14% for most folks right now. That gap is basically the "hidden tax" of loan origination and lender fees that people always forget to budget for until they’re sitting in the lawyer's office.

The 15-year vs. 30-year divide

If you can stomach the higher monthly payment, the 15-year is looking pretty attractive at 5.38% to 5.47%.

You're basically saving nearly a full percentage point over the 30-year. Over the life of a $400,000 loan, that’s not just "coffee money." It’s "early retirement" money. Specifically, the total interest on a 15-year today is about $187,155, compared to a staggering $478,221 on a 30-year.

Math is brutal sometimes.

The "Lock-in Effect" is finally cracking

For the last few years, the housing market has been essentially frozen. People who snagged a 3% rate during the pandemic were basically held hostage by their own good luck. Why would you sell your house and trade a 3% mortgage for an 8% one? You wouldn't.

But something changed this month.

We just crossed a threshold where there are now more Americans with mortgage rates above 6% than there are people with rates below 3%.

This is huge.

🔗 Read more: Why 333 Hudson St New York NY is the Hudson Square Office Building to Watch

Nick Gerli over at Reventure pointed this out recently. It means the "lock-in effect" is losing its grip. When more people are already paying 6%, moving to a new house at 6% doesn't feel like a financial death sentence anymore. It just feels... normal.

What is the Fed doing in 2026?

The Federal Reserve is in a weird spot.

In December 2025, they cut the benchmark rate by 25 basis points, bringing it down to a range of 3.5% to 3.75%. That was the third cut in a row. But don't get too excited.

Jerome Powell and the gang are divided. Some members, like Stephen Miran, wanted deeper cuts because they’re worried about the job market cooling off too much. Others are terrified that inflation—which is currently around 2.7%—will come roaring back if they let off the gas too soon.

There is also a lot of political noise. The Trump administration has been pushing hard for lower rates, even launching investigations into the Fed's leadership.

Most experts, including Michael Feroli at J.P. Morgan, think the Fed might actually pause their cuts in January. They want to see if the economy is actually slowing down or if it’s just having a "soft patch."

Why the numbers you see online might be wrong for you

Let's be real: those "average" rates you see on the news are for people with 780 credit scores and 20% down payments.

If your credit is more "average" (think 680 to 720), your actual rate today is probably going to be 0.5% to 1% higher than the headline number.

And then there's the location factor.

- In Austin, Texas, Wells Fargo is quoting about 6.00% for a 30-year.

- In Michigan, rates might fluctuate based on local credit union competition.

- If you're looking at a Jumbo loan (for those big-ticket houses), you're looking at 6.40%.

The APR Trap

I see people fall for this every single day. A lender advertises 5.75% and you get all excited. Then you read the fine print and realize they’re charging you two "points" upfront to get that rate.

A point is 1% of the loan amount. On a $500,000 mortgage, that’s $5,000 out of your pocket just to lower the rate. Usually, it takes 5 to 7 years of living in the house just to break even on that cost. If you plan to move in three years? You just handed the bank a $5,000 gift.

Is 2026 the year to buy?

It’s a complicated "maybe."

Lawrence Yun, the chief economist at the National Association of Realtors (NAR), is actually pretty optimistic. He expects home sales to jump about 14% this year. Why? Because inventory is finally up—about 20% higher than it was this time last year.

You actually have choices now. You don't have to waive inspections or offer $50,000 over asking price in a blind panic.

But don't expect prices to drop. NAR expects home prices to still grow about 2% to 3% this year. It's not the explosive growth we saw a few years ago, but it’s still growth.

Actionable steps for your mortgage search

If you are shopping for a home this weekend, here is how you should actually handle it:

- Get at least three quotes on the same day. Mortgage rates change by the hour. A quote from Tuesday is useless on Friday.

- Focus on the Monthly Payment, not just the Rate. A 6.1% rate on a cheaper house is better than a 5.5% rate on an overpriced one.

- Check the 5/1 ARM if you’re moving soon. Adjustable-rate mortgages (ARMs) are currently around 5.51%. If you know you're only going to be in that city for three or four years, why pay the premium for a 30-year fixed?

- Ignore the "Wait for 4%" crowd. Most forecasts, including those from Realtor.com, see the 30-year rate averaging 6.3% for the rest of 2026. If you’re waiting for rates to hit 4% again, you might be waiting until 2030.

The housing market in 2026 is finally becoming "boring" again. And honestly, after the chaos of the last five years, boring is exactly what we need. Rates are stable, inventory is returning, and the panic is subsidizing.

If the math works for your budget at 6.11%, it’s a fine time to move. Just don't expect the bank to do you any favors—you've still got to shop around and make them compete for your business.

Compare the total loan estimate documents side-by-side, focusing specifically on Section A (Origination Charges) and Section B (Services You Cannot Shop For). These are the real indicators of how much a lender is charging you to access today's market rates. Keep an eye on the 10-year Treasury yield as well; if that starts to climb above 4.2%, expect these mortgage rates to tick back up toward 6.5% by the end of the month.