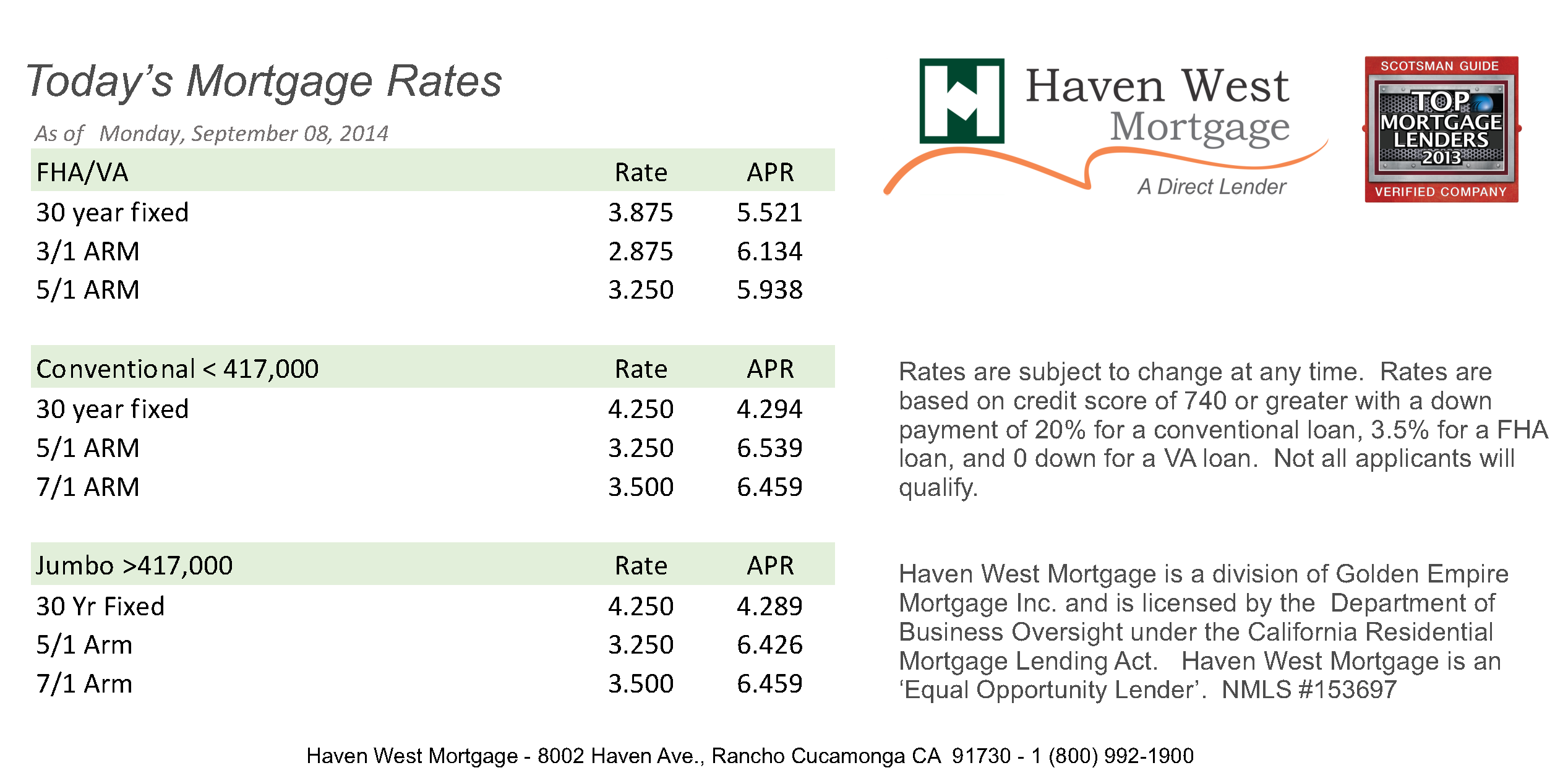

It finally happened. After what felt like an eternity of staring at 7% and 8% stickers on house listings, the psychological wall has cracked. If you're looking at what are the mortgage interest rates today, you’ll see the number 5 leading the pack for the first time in a long time for many borrowers.

As of Wednesday, January 14, 2026, the national average for a 30-year fixed mortgage is hovering right around 5.94% to 5.99%.

Some lenders are a bit higher, some are a bit lower. Bankrate has the APR average slightly higher at 6.20% when you factor in all the fees, but for the raw interest rate? We are officially back in the 5s.

It’s a weird relief.

The Reality of What Are the Mortgage Interest Rates Today

Honestly, the "average" is just a starting point. It's like the MSRP on a car; nobody actually pays exactly that.

If you have a credit score that looks like a high school batting average, you aren't getting 5.9%. But if you've got that 780+ score and a solid down payment, today is a good day. For the 15-year fixed crowd, things look even better. You're looking at an average of 5.25% to 5.53%.

Why the sudden dip?

Basically, the Federal Reserve spent the end of 2025 cutting rates like they were clearing brush. They lopped off 25 basis points in December, marking the third cut in a row. The market is basically betting that they aren't done yet.

Breaking Down the Current Numbers (Jan 14, 2026)

- 30-Year Fixed: 5.99% (Zillow/NerdWallet)

- 15-Year Fixed: 5.25%

- 30-Year FHA: 5.63%

- 30-Year VA: 5.63%

- 30-Year Jumbo: 6.00%

- 5/1 ARM: 6.17% (Yeah, these are weirdly higher than fixed rates right now—don't ask.)

Why the "Inverted" ARM Rate is So Weird

You’d think an Adjustable Rate Mortgage (ARM) would be cheaper because you’re taking on the risk of the rate moving later, right?

Not today.

Right now, a 5/1 ARM is sitting at 6.17%, which is actually higher than a standard 30-year fixed. This happens when the market is "inverted." Lenders are so convinced that rates will stay lower in the long term that they aren't giving you a discount for the short term.

It’s a signal.

🔗 Read more: Who Owns Procter and Gamble: What Most People Get Wrong

The market thinks the "emergency" high-rate era is over.

The Fed, Trump, and Your Monthly Payment

The political landscape is also throwing some spice into the mix. President Trump has been vocal about wanting Fannie Mae and Freddie Mac to start buying up bonds more aggressively.

When that happens, mortgage rates usually drop.

Investors are reacting to those headlines in real-time. Just today, rates jumped about 14 basis points from yesterday's lows, mostly because the market is trying to figure out if the Fed will pause in January or keep the cuts coming.

Jerome Powell’s term as Fed Chair ends in May 2026. The uncertainty about who takes his seat—and whether they’ll be a "hawk" or a "dove"—is making the daily rate charts look like a heart monitor.

Is Now the Time to Refinance?

If you bought a house in 2024 or early 2025, you might be sitting on a rate of 7.2% or higher.

Do the math.

On a $400,000 loan, the difference between 7.2% and 5.9% is roughly **$330 a month**. That’s almost $4,000 a year back in your pocket.

Most experts, including the folks at NerdWallet, suggest that if your current rate is 6.5% or higher, you should at least start talking to a loan officer. You don't want to wait for the "perfect" bottom that might never come, especially since home prices are expected to rise about 2% this year because more buyers are finally entering the market.

What to Do Next

Don't just look at the national average and assume that's your number.

Rates in New York are averaging around 6.25%, while buyers in New Jersey and Texas are seeing closer to 5.87%. It is wildly local right now.

- Check your credit score first. If you’re at 690, spend a month cleaning up small balances to hit 720. It could save you 0.5% on your rate.

- Get three quotes. Seriously. Lenders are hungry for business again after a slow 2025. Make them compete.

- Watch the 10-Year Treasury yield. If you see the 10-year yield dropping on the news, mortgage rates usually follow about 24-48 hours later.

- Consider a "Rate Lock." If you find a lender offering 5.8% or 5.9% today, it might be worth locking it in for 30 or 45 days. The volatility is real, and a single "hot" inflation report could send these numbers back above 6% by Friday.

The window is open. It might not stay open forever, but for the first time in three years, the math actually makes sense for a lot of families again.