Everyone wants a magic number. You're probably sitting there, staring at a Zillow listing or a pile of refinance paperwork, wondering if the mortgage interest rate forecast for 2026 is actually going to save your bank account. Honestly? It's a mess. If you look at what the "big guys" like Fannie Mae and the Mortgage Bankers Association were saying twelve months ago, they didn't see this coming. Not really.

Rates are sticky.

That's the technical term, anyway. It means they aren't dropping as fast as your Uncle Bob promised they would at Thanksgiving. We’ve entered a cycle where the Federal Reserve is playing a high-stakes game of chicken with inflation, and homeowners are caught in the crossfire. You’ve got the 10-year Treasury yield dancing around like a caffeinated toddler, and every time it spikes, your potential monthly payment climbs another hundred bucks. It's frustrating. It's confusing. And if we’re being real, most of the "expert" advice you’re reading online is just recycled press releases from three months ago.

The Fed vs. Your Front Porch

We have to talk about Jerome Powell. He’s the guy holding the steering wheel, but the steering wheel is barely attached to the tires. The Federal Open Market Committee (FOMC) has been trying to stick a "soft landing," which basically means they want to kill inflation without murdering the entire economy. For a while, the mortgage interest rate forecast looked rosy because everyone assumed the Fed would slash rates the second inflation hit 2%.

It didn't happen like that.

Inflation is like that one guest who won't leave the party. It’s lingering in services, insurance costs, and property taxes. Because of that, the Fed has been "higher for longer" than anyone anticipated. When the Fed funds rate stays up, the banks get nervous. When banks get nervous, they pad their margins. You see this in the "spread"—the gap between the 10-year Treasury and the 30-year fixed mortgage. Historically, that gap is about 1.7%, but lately, it’s been hovering much higher.

Why? Because banks are scared of "prepayment risk." They don't want to give you a 6.5% loan today if they think you're just going to refinance it in six months when rates hit 5.5%. They want to make their money. So, they keep your rate higher to protect their own downside. It's not personal; it's just business. But it feels pretty personal when you're looking at a $3,000 mortgage payment for a house that cost half as much five years ago.

Why 3% Rates are a Ghost Story

Stop waiting for 3%. Seriously. Just stop.

Those sub-3% rates we saw during the pandemic were a freak accident of history. They were the result of the government dumping trillions of dollars into the system and the Fed buying up mortgage-backed securities like they were at a garage sale. That era is over. The "new normal" for a mortgage interest rate forecast likely sits somewhere between 5.5% and 6.5%.

Think about it this way: for most of the last 50 years, a 6% interest rate was considered a "good deal." My parents bought their first house at 14% and thought they were winning at life. We've just been spoiled by a decade of free money. Lawrence Yun, the chief economist at the National Association of Realtors, has been saying for a while that we’re looking at a slow grind downward, not a cliff-dive. If you're waiting for 2021 prices and 2021 rates to return, you're going to be renting for a very long time.

The Inventory Trap and the "Lock-In" Effect

Here is something weird. Usually, when rates go up, house prices go down because people can't afford the payments. Demand drops, prices drop. Basic economics, right?

Wrong.

The housing market broke the rules. We have something called the "lock-in effect." Imagine you’re sitting on a 2.75% mortgage. You want a bigger kitchen. You want a shorter commute. But if you move, your new mortgage will be 6.8%. Your payment would double for the exact same loan amount. So, what do you do? You stay put. You renovate the basement. You wait.

👉 See also: Stock Market Live News Today: Why the AI Trade is Getting Weird

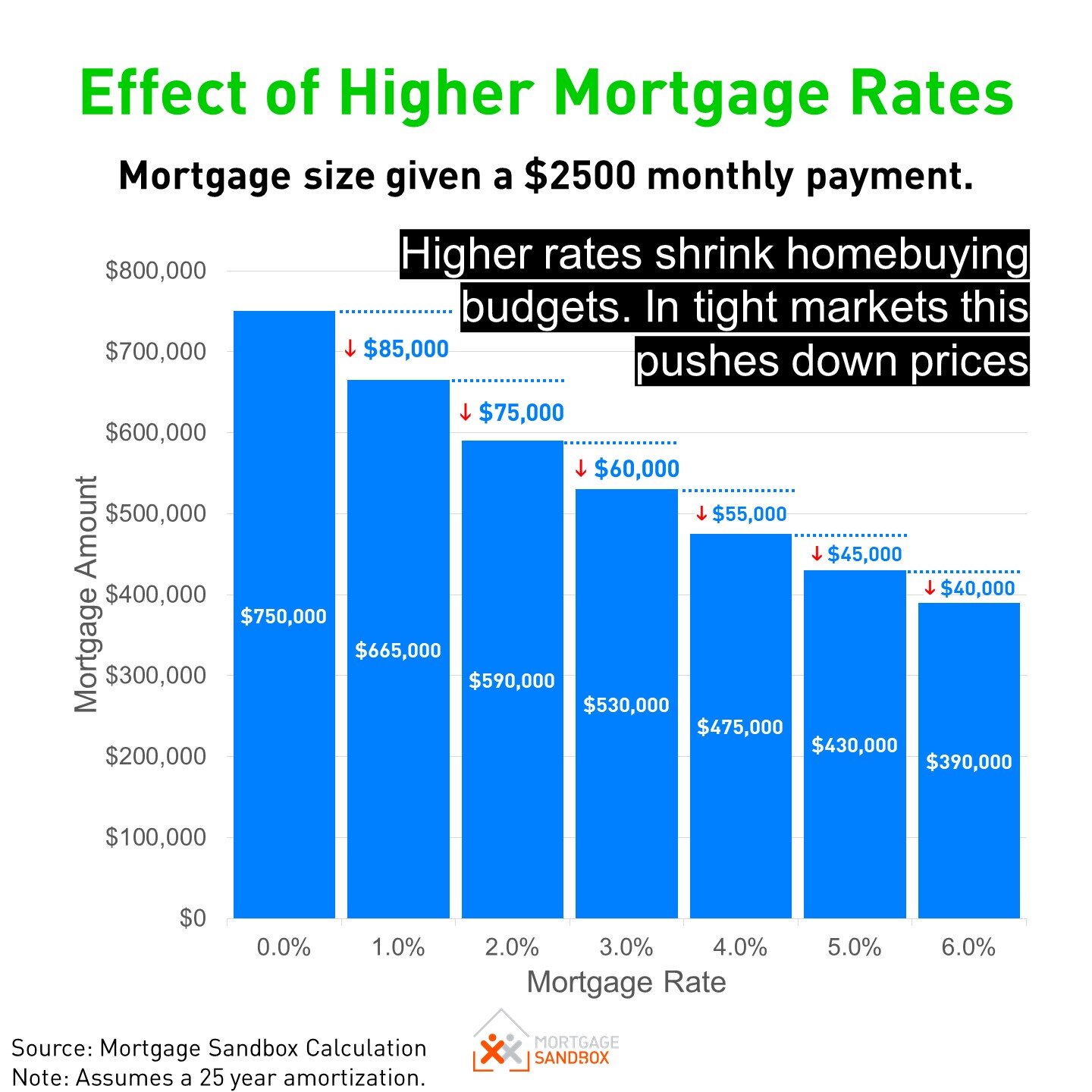

Because nobody is moving, there are no houses for sale. Because there are no houses for sale, the few people who must move (because of jobs, divorce, or babies) are fighting over a tiny pool of inventory. This keeps prices high even while rates suck. It's a double whammy. The mortgage interest rate forecast has to account for this lack of liquidity. Until rates drop enough to make people willing to give up their old "golden" mortgages, the market is going to stay constipated.

What the Data is Actually Saying

If you look at the CME FedWatch Tool—which is basically a way to see what professional traders think the Fed will do—there’s a lot of volatility. One week the market expects three rate cuts, the next week it expects zero.

- The Optimist View: Inflation cools faster than expected, the job market softens, and the Fed gets aggressive. We could see 30-year rates dip into the high 5s by the end of the year.

- The Realist View: The economy stays "too good." People keep spending. The Fed keeps rates right where they are to make sure inflation doesn't roar back. Rates wobble between 6.3% and 6.9%.

- The Pessimist View: A global conflict or energy spike sends inflation back up. The Fed has to hike again. We see 8% on the horizon. (This is unlikely, but hey, 2020 happened, so never say never).

Strategies for a High-Rate World

So, you’re looking at this mortgage interest rate forecast and feeling a bit bleak. What do you actually do? You can't control the Fed, but you can control your "deal."

Some people are turning to ARMs—Adjustable Rate Mortgages. Now, don't freak out. These aren't the "exploding" loans of 2008 that blew up the global economy. Modern ARMs are much more regulated. If you know you're only going to be in a house for five or seven years, a 5/1 ARM might save you a full percentage point over a 30-year fixed. It’s a gamble, sure. But in this market, every penny counts.

Then there’s the "buy-down." You might have heard of a 2-1 buy-down. Basically, the seller pays a lump sum to lower your interest rate for the first two years. It gives you some breathing room. If rates drop in those two years, you refinance. If they don't, you've at least saved some cash upfront. It’s becoming a huge bargaining chip in new construction especially. Builders have deep pockets and they'd rather give you a rate buy-down than lower the "sticker price" of the house, which would piss off the neighbors who just bought.

Misconceptions About the 10-Year Treasury

A lot of folks think mortgage rates follow the Fed Funds Rate exactly. They don't. They follow the 10-year Treasury yield. If the bond market thinks the economy is going to tank, the 10-year yield drops, and mortgage rates usually follow.

But here’s the kicker: the bond market is often wrong.

Bond traders are some of the most reactive people on the planet. One bad jobs report and they start buying bonds, driving yields down. One "hot" CPI report and they sell everything. This is why you’ll see mortgage rates change twice in a single day. If you’re shopping for a loan, don't just check the rate on Monday and assume it’ll be there Friday. When you see a dip, you have to be ready to "lock."

The "Wait and See" Cost

There is a hidden cost to waiting for a better mortgage interest rate forecast. It’s called appreciation.

Let's say you're waiting for rates to drop 1%. On a $400,000 house, that 1% might save you $250 a month. Sounds great. But if it takes 18 months for that drop to happen, and home prices rise by 5% in that time, that same house now costs $420,000. You’ve "saved" on the interest but you’re borrowing more money to buy a more expensive asset.

Sometimes, the "expensive" mortgage is actually the cheaper path if it gets you into a house before the next price surge. You can always change your interest rate later through a refinance. You can never change the price you paid for the house. That's the one number that's set in stone.

Don't Forget the "Hidden" Numbers

When you're obsessing over the mortgage interest rate forecast, it's easy to ignore the other stuff that actually matters. Your credit score is the biggest lever you have. A 760 score vs. a 660 score can be the difference between a 6.2% rate and a 7.5% rate. That’s a way bigger swing than anything Jerome Powell is going to do this month.

Also, look at your Debt-to-Income (DTI) ratio. Lenders are getting pickier. They don't just want to see that you make money; they want to see that you aren't drowning in car payments and credit card debt. If you can clear out a $400 car payment, you might suddenly qualify for $50,000 more in "house," regardless of what the interest rates are doing.

Real Talk: What Happens Next?

Where does that leave us? Honestly, we're in a period of "sideways" movement. The era of rapid changes is likely behind us, replaced by a slow, boring stabilization. We'll probably see the mortgage interest rate forecast hover in the 6s for the foreseeable future.

If you find a house you love and you can afford the payment today, buy it. If you’re stretching your budget to the breaking point hoping you can refinance in six months, stop. Refinancing isn't free. It costs thousands in closing costs. You shouldn't bank on a "future" rate to make a "today" house work.

The market is currently pricing in a lot of uncertainty. There’s an election coming up. There are wars. There’s a weirdly resilient job market. All of these things act like static on a radio, making it hard to hear the actual signal. But the signal is this: housing demand is still higher than housing supply. That’s the "floor" for the market.

Moving Toward Action

Instead of just watching the news and stressing out, take a look at your actual numbers. Talk to a local lender—not just a big national website—and ask about "par rates" and "points." Sometimes paying a little extra upfront to "buy down" the rate permanently makes way more sense than waiting for the market to move.

- Check your credit report for errors that might be dragging your score down by 20 or 30 points.

- Calculate your "break-even" point on a refinance. If rates drop by 0.75%, is that enough to cover the $5,000 in fees?

- Look into local first-time homebuyer programs. Many states have "silent seconds" or grants that effectively lower your entry cost, making a 6.5% rate feel more like a 5% rate.

The mortgage interest rate forecast is a tool, not a crystal ball. Use it to understand the trend, but don't let it paralyze you. The best time to buy a house is usually when you find the right home and your finances are ready, regardless of what the talking heads on TV are screaming about this week. Rates will go up, and they will go down. A house is a place to live first and an investment second. Keep that perspective, and you’ll be fine.