Selling a mobile home isn't like selling a car, but it’s also nothing like selling a traditional "sticks-and-bricks" house. It occupies this weird, middle-ground legal space that catches people off guard. You’re essentially dealing with a piece of personal property that acts like real estate. Because of that, a mobile home bill of sale form is the most important piece of paper you’ll touch during the entire transaction. If you mess it up, you aren't just looking at a headache; you're looking at potential lawsuits or a DMV nightmare that lasts months.

I’ve seen people try to scribble a deal on a napkin. Don’t do that. Honestly, the legalities of manufactured housing are surprisingly picky, and while it feels informal—especially if the home is in a park—the paper trail needs to be ironclad.

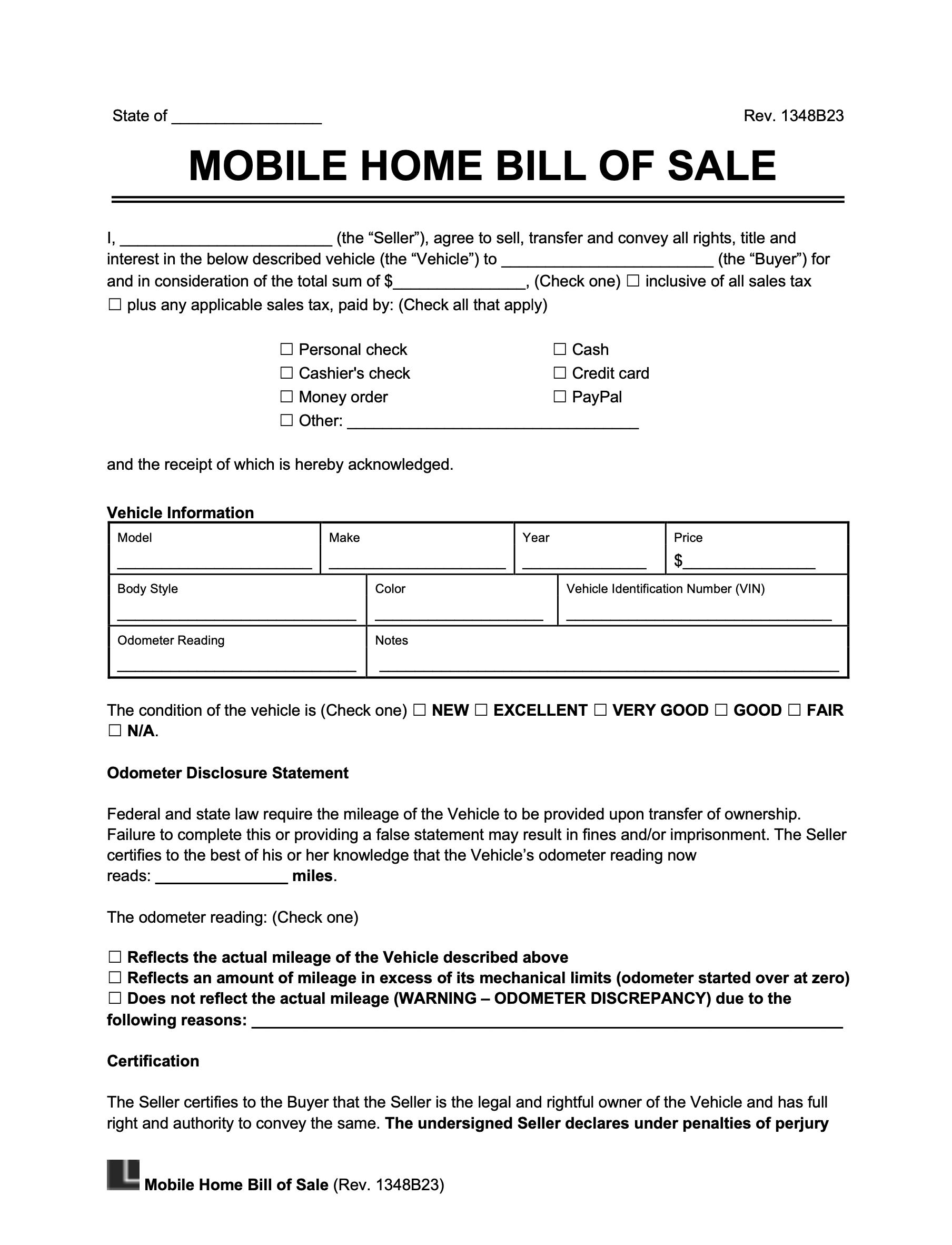

Why the mobile home bill of sale form is your only real protection

Think of this document as your shield. For the buyer, it proves ownership. For the seller, it’s the "get out of jail free" card that transfers liability. Once that money hits your hand and the form is signed, you’re no longer responsible if the water heater explodes two days later or if the roof starts leaking during a summer storm.

Most people assume the title is enough. It isn’t. While the title (issued by your state's Department of Housing or DMV) shows who owns the unit, the mobile home bill of sale form outlines the terms of that ownership change. It’s the contract. It says, "I'm selling this 'as-is,' and no, I'm not giving you a warranty." Without that specific language, you might accidentally find yourself on the hook for repairs you thought you’d walked away from.

The "As-Is" trap and why it matters

In many states, if you don't explicitly state the home is being sold "as-is" on the bill of sale, there’s an implied warranty of habitability. This is huge. If a buyer moves in and finds a massive mold issue or a cracked frame that wasn't disclosed, and your paperwork is flimsy, a judge might decide you owe them for repairs. You've got to be crystal clear. Use the words. Put them in bold.

🔗 Read more: Chuck E. Cheese in Boca Raton: Why This Location Still Wins Over Parents

Essential details that actually belong on the form

You can’t just put "One blue mobile home" and call it a day. The specifics matter because the government wants to track these things for tax purposes. If the VIN or serial number is off by even one digit, the state will reject the filing. You'll be stuck chasing down the buyer—who might already be living three states away—to get a corrected signature.

- The VIN or Serial Number: Usually found on a data plate inside a kitchen cabinet, near the main electrical panel, or stamped on the steel frame (the "tongue").

- Make, Model, and Year: Don't guess. Check the existing title or the HUD tag.

- HUD Tag Numbers: Those little metal plates on the exterior? Those numbers are gold. They prove the home meets federal standards.

- The Purchase Price: Be honest here. Some people try to under-report the price to save the buyer on sales tax. That's tax fraud. Plain and simple. Plus, it messes with the "basis" if the buyer ever sells it later.

- Park Information: If the home is staying in its current lot, you need to mention the park name and lot number.

A quick note on the land

Is the land included? Probably not, unless you own the dirt beneath the wheels. This is where a lot of first-time buyers get confused. If the home is in a park, the mobile home bill of sale form only transfers the structure. The buyer still has to go through a separate background check and lease agreement with the park management. If they get rejected by the park but you’ve already "sold" them the home, you’ve got a massive problem on your hands. Always make the sale contingent on park approval.

Common mistakes that kill the deal

People get lazy. It’s human nature. But laziness in a private party sale is expensive.

One major blunder is forgetting the "Right of First Refusal." Many mobile home parks have a clause in their lease that says if you sell your home, the park gets the first chance to buy it at your asking price. If you sign a mobile home bill of sale form with a third party without checking this, the park can actually void the sale. It sounds crazy, but it’s in the fine print of those 30-page lot leases.

💡 You might also like: The Betta Fish in Vase with Plant Setup: Why Your Fish Is Probably Miserable

Another thing? Notaries. Depending on your state—places like Ohio or Kentucky come to mind—you might actually need a notary to witness the signatures on the bill of sale for it to be considered valid for title transfer. Even if your state doesn't require it, do it anyway. It costs five bucks at a local bank and makes the document nearly impossible to dispute in court. It proves that the person signing was actually who they said they were.

Taxes, Liens, and the "Hidden" Paperwork

Before you even look at a mobile home bill of sale form, you have to clear the title. You’d be surprised how many people try to sell a mobile home while they still owe $15,000 on a personal loan or have back taxes due to the county.

In many jurisdictions, mobile homes are taxed as personal property. If those taxes aren't paid, the county puts a lien on the unit. You cannot legally transfer a title until those taxes are caught up. As a buyer, you should always call the county tax assessor’s office with the VIN. Ask them if there are any outstanding "chattel" taxes. If you don't, you might inherit a $2,000 tax bill the moment you sign that bill of sale.

Dealing with the HUD Plate

If that little red metal tag is missing from the exterior, getting financing becomes a nightmare. Most FHA or VA loans won't touch a home without it. If you're the seller and the tag is gone, you should mention that in the bill of sale so the buyer can't claim they were misled about the home's eligibility for future financing. You can order a "Letter of Label Verification" from the Institute for Building Technology and Safety (IBTS) if the tags are gone, but it takes time.

📖 Related: Why the Siege of Vienna 1683 Still Echoes in European History Today

How to actually execute the transfer

The process is pretty straightforward, but you have to follow the sequence. Don't skip steps.

- Verification: Buyer checks the VIN against the title and confirms the seller is actually the person named on the title.

- Park Approval: If the home is in a park, the buyer gets their "green light" from management.

- The Form: Both parties fill out the mobile home bill of sale form in duplicate. Everyone gets an original.

- The Cash: Payment is exchanged. Usually, a cashier's check or wire transfer is safest. Cash is okay, but get a receipt.

- Title Signing: The seller signs the actual title over to the buyer. This is usually a separate document from the bill of sale.

- The DMV/Housing Office Trip: The buyer takes the bill of sale and the signed title to the state agency to get a new title issued in their name.

Don't leave the "Date of Sale" blank. It’s the anchor for the whole timeline. It determines when the insurance coverage should switch over and when the new owner's tax liability begins.

Real-world nuance: The "Abandoned" Home

Sometimes you’ll find a deal that seems too good to be true. A "handyman special" left behind by a previous tenant. Be careful. You can't just use a mobile home bill of sale form if the person selling it doesn't have the title. If a park owner is selling an abandoned unit, they have to go through a "warehouseman’s lien" or an "abandonment process" first. If they haven't done that legal legwork, that bill of sale they give you is basically a piece of scrap paper. You won't be able to register the home, and you won't be able to get insurance.

What about the contents?

Unless you specify otherwise, a bill of sale for the home usually includes the fixtures—things like the stove, fridge, and HVAC system. But what about that nice shed in the backyard? Or the expensive porch furniture? If it's not attached to the home, it's not part of the sale unless you write it down. I’ve seen friendships end over a $500 lawnmower that the buyer thought was included and the seller took with them.

Actionable Next Steps

If you're ready to move forward, don't just grab the first generic form you find on a random website. You need to ensure it meets your specific state's criteria.

- Check your state's specific requirements. Places like Florida (Department of Highway Safety and Motor Vehicles) and California (Housing and Community Development) have very specific forms they prefer you use alongside your bill of sale.

- Gather your numbers. Locate the VIN, the HUD tag numbers, and the serial number. If you can't find them, stop. You need these before you can draft a valid document.

- Call the Tax Assessor. Ensure there are no outstanding personal property taxes tied to the unit's VIN.

- Draft the "As-Is" clause. Even if you're selling to a friend, protect yourself by clearly stating that the home is sold in its current condition with no guarantees.

- Get a Notary. Find a local mobile notary or visit your bank. It’s the single best way to prevent future claims of "I never signed that."

Handling a mobile home bill of sale form correctly is about more than just a transaction. It's about finality. It’s the difference between a clean break and a lingering legal tie to a property you no longer want. Take the extra thirty minutes to do it right. You'll sleep better.