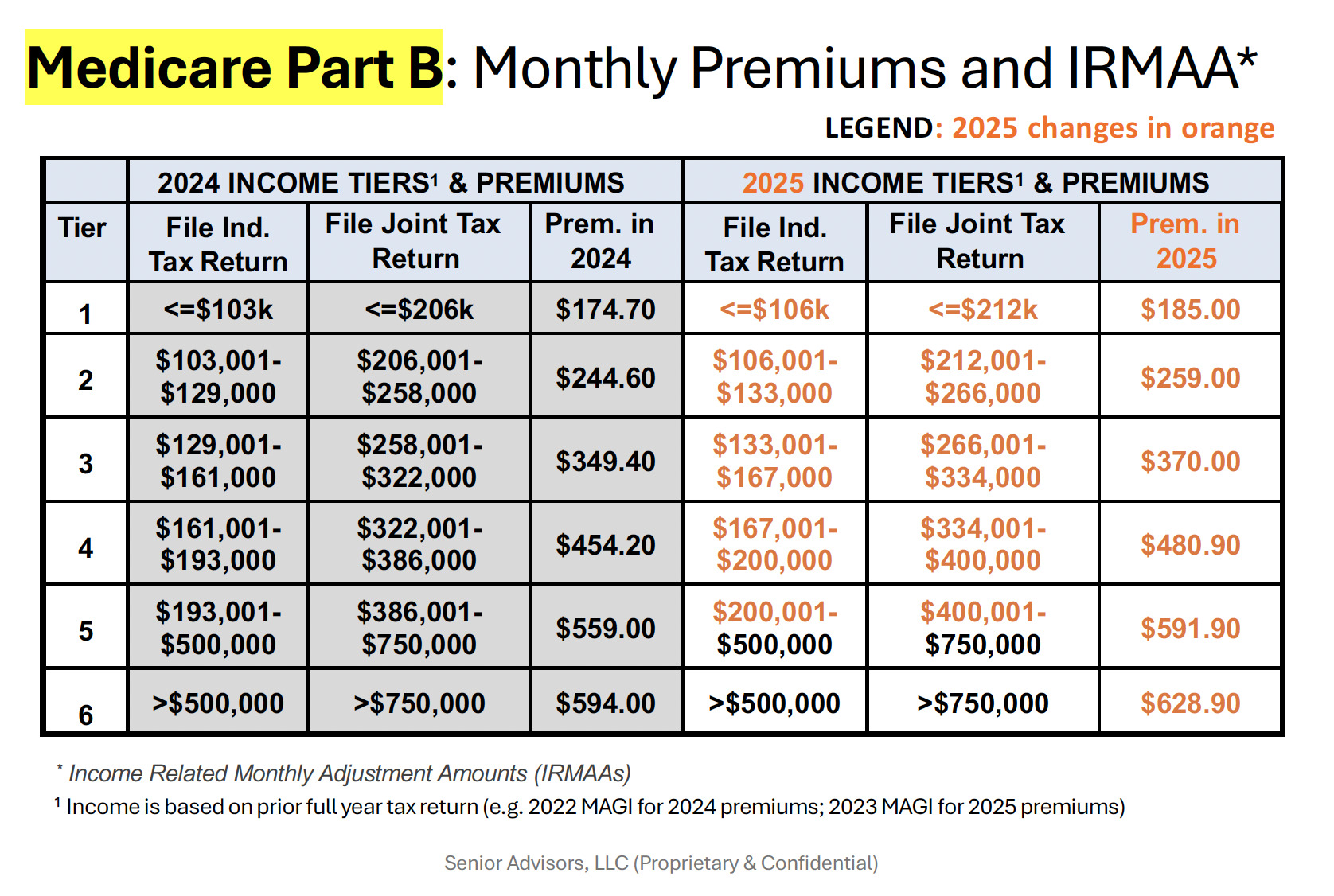

You ever look at your paystub and wonder why your "Gross Pay" looks so much better than the actual money that hits your bank account? It's honestly a bit of a gut punch. You see these acronyms—FICA, OASDI, Med—and they’re just eating away at your hard-earned cash.

Basically, we’re talking about the heavy hitters of payroll: Social Security and Medicare. Most people just assume it’s a flat percentage that never changes. They're wrong. For 2026, the goalposts have shifted again. If you’re trying to figure out how much is medicare and ss tax, you need to look at more than just a single percentage.

Between the new wage base limits and the way "Additional Medicare Tax" kicks in for higher earners, your actual tax bill can feel like a moving target.

The Social Security Breakdown for 2026

Let’s talk Social Security first. This is the big one, officially known as OASDI (Old-Age, Survivors, and Disability Insurance).

For 2026, the tax rate itself remains steady at 6.2% for employees. Your employer matches that, paying another 6.2% on your behalf. But there is a catch: the "Wage Base Limit."

Uncle Sam doesn't tax every single dollar you make for Social Security. Once you hit a certain amount of earnings in a calendar year, the 6.2% tax just... stops. For 2026, that limit has jumped to $184,500. That is up quite a bit from the $176,100 limit we saw in 2025.

If you make $200,000 a year, you only pay that 6.2% on the first $184,500. Everything above that is "Social Security tax-free." It’s sort of a built-in pay raise that happens later in the year for high earners. If you're a math person, that means the absolute maximum an employee will pay into Social Security in 2026 is **$11,439.00**.

Medicare: The Tax That Never Ends

Medicare is a different beast entirely. Unlike Social Security, there is no wage limit for Medicare. None. Zip.

The standard rate is 1.45%. You pay it on your first dollar, and you pay it on your millionth dollar. Your employer matches this one too, putting in another 1.45%.

But then there's the "Additional Medicare Tax." This was a "gift" from the Affordable Care Act that's still very much in play. If you earn more than $200,000 (for single filers), the IRS tack on another 0.9% to your Medicare tax.

Here is the kicker: your employer does not match the 0.9%. That’s all on you. And they are required to start withholding it the moment your wages with that specific employer cross the $200,000 mark.

It gets messy for married couples. If you make $150,000 and your spouse makes $150,000, neither of your employers will withhold that extra 0.9%. But when you file your taxes together, the IRS looks at your combined $300,000. Since the threshold for married couples is $250,000, you'll suddenly owe that 0.9% on the extra $50,000. You've basically got to plan ahead for that bill in April.

The Self-Employed "Double Tax" Reality

If you’re a freelancer or a small business owner, the answer to how much is medicare and ss tax is significantly more painful. You are the employee and the employer.

You pay both halves.

This is what’s known as the Self-Employment Tax (SECA). Instead of 7.65%, you’re looking at a total of 15.3%.

- 12.4% goes to Social Security (up to that $184,500 limit).

- 2.9% goes to Medicare (on all your net earnings).

Before you panic, there is a bit of a silver lining. The IRS lets you deduct the "employer" half of that tax—the 7.65%—when you’re calculating your adjusted gross income. It doesn't make the check you write to the Treasury any smaller, but it does lower your overall income tax bill.

Kinda helps. Sorta.

Why the Numbers Changed This Year

You might be wondering why the Social Security limit keeps climbing. It’s tied to the National Average Wage Index. As wages across the country go up, the Social Security Administration (SSA) bumps the taxable maximum to keep the system funded.

For 2026, we also saw the impact of the One Big Beautiful Bill Act (OBBBA). While that law focused heavily on making income tax brackets permanent, it also reinforced the stability of these FICA rates.

A Quick Cheat Sheet for 2026

If you just want the raw numbers to check against your paystub, here they are:

Social Security (OASDI):

- Tax Rate: 6.2%

- Wage Base: $184,500

- Max Tax: $11,439.00

Medicare (HI):

- Tax Rate: 1.45%

- Wage Base: No limit

- Additional Tax: 0.9% on earnings over $200,000 (Single) or $250,000 (Jointly).

What You Should Do Now

Knowing these numbers is great, but actually doing something with them is better.

First, if you're a high earner or part of a dual-income household, check your withholding. If you think you're going to cross those $200k or $250k thresholds, you might need to ask your employer to withhold a little extra federal income tax to cover the Medicare surtax. It beats a surprise penalty later.

Second, if you’re self-employed, make sure your estimated quarterly payments are based on the 2026 wage base of $184,500. If you're still using 2025 numbers, you’re going to be underpaid.

📖 Related: Why the NYSE 52 week low list is actually a contrarian goldmine

Finally, keep an eye on your "year-to-date" earnings on your paystubs. Once you hit that $184,500 mark, your take-home pay will suddenly jump by 6.2%. That’s a great time to shove that "extra" money into a 401(k) or a high-yield savings account before you get used to spending it.

Don't let the FICA acronym confuse you. It’s just a fancy way of saying "the price of admission for future benefits." Stay on top of the limits, and you won't be surprised when the tax man comes knocking.