You'd think having insurance would be enough to keep the repo man away from your front door. Honestly, for millions of families, it’s just not. We’ve all heard the horror stories: a sudden car wreck, a cancer diagnosis, or even just a weirdly expensive trip to the ER that ends in a five-figure bill. But when you look at the actual data for 2026, the reality of medical bankruptcies in america is even more complicated than just "bad luck."

Basically, medical debt has become a permanent fixture of the American financial landscape. Even with the Affordable Care Act (ACA) and various state-level protections, the system is still churning out debt at a staggering rate. About 100 million people in this country are currently saddled with health care debt they can’t pay back. That is nearly 41% of all adults.

Think about that. Four out of every ten people you see at the grocery store are likely struggling to pay for a doctor’s visit they already had.

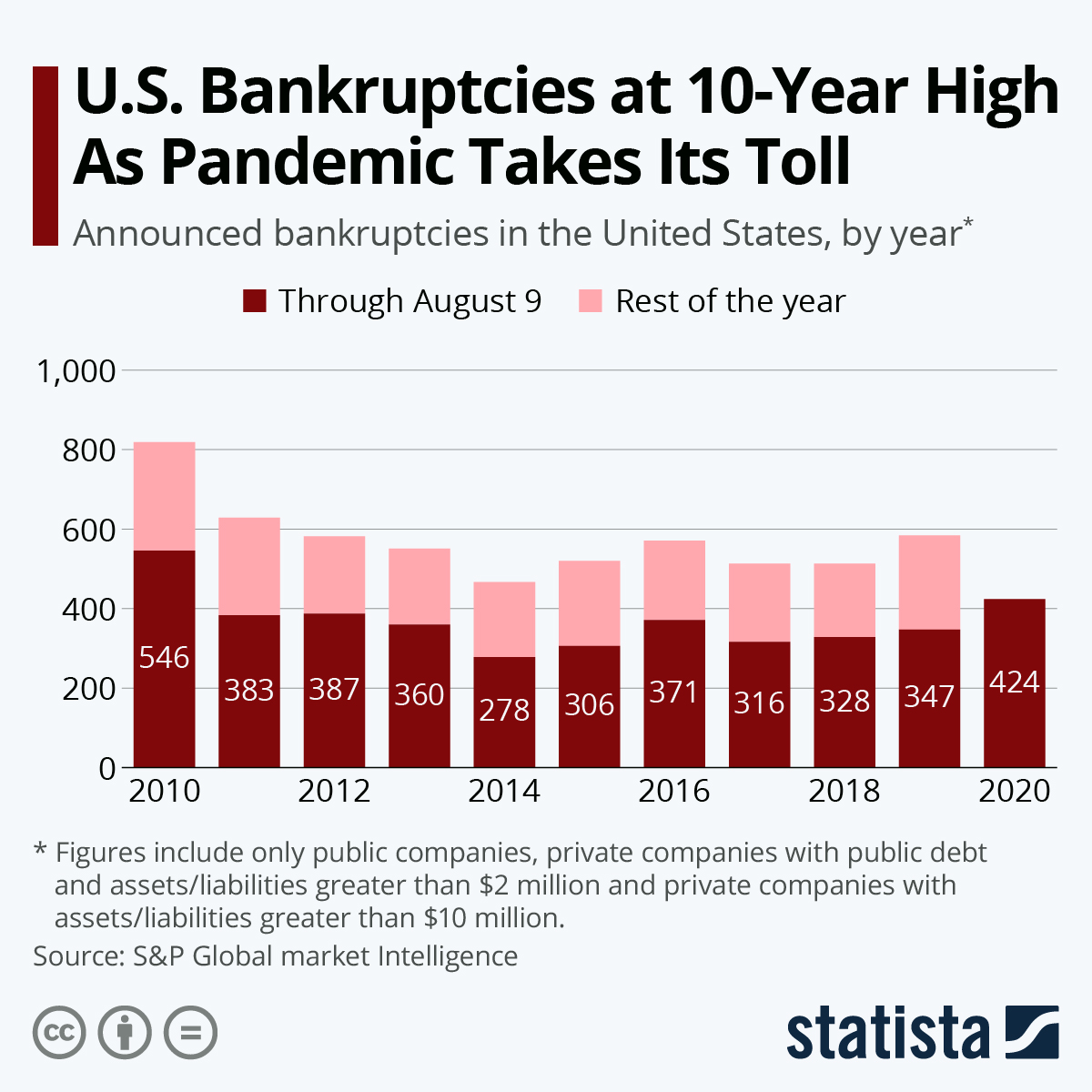

The 66% Factor: What Really Drives People to File

If you walk into a bankruptcy court today, there is a two-thirds chance the person filing is there because of medical expenses. According to research led by Dr. David Himmelstein, a professor at Hunter College, about 66.5% of all bankruptcies in the U.S. are tied to medical issues.

It isn't always just the bill from the surgeon, either. It’s the "collateral damage" of being sick. You lose your job because you can't work. You burn through your savings to pay the mortgage while you're in recovery. Then the credit cards get maxed out just to buy groceries. By the time someone actually files for bankruptcy, the medical debt has usually triggered a total financial collapse.

Why Insurance Isn't a Safety Net Anymore

Most people filing for medical-related bankruptcy actually had insurance when they got sick. This is the part that trips people up. You pay your premiums every month, you stay "in-network," and you still get clobbered.

💡 You might also like: Why the Long Head of the Tricep is the Secret to Huge Arms

- The Deductible Trap: Many plans now have deductibles of $5,000 or even $10,000. Most Americans don't have $1,000 in savings, let alone ten times that.

- The "Covered" Lie: Just because a procedure is "covered" doesn't mean it's paid for. Co-insurance—where you pay 20% or 30% of the total cost—can easily reach five figures for a major surgery.

- The One Big Beautiful Bill Act (OBBBA): This recent federal legislation has shifted the landscape in 2026. While it aimed to streamline some costs, the cuts to Medicaid and the expiration of ACA tax credits have left millions of people "underinsured." They have a card in their wallet, but they can't afford to use it.

The Credit Score War of 2025 and 2026

There was a huge moment of hope in early 2025. The Consumer Financial Protection Bureau (CFPB) finalized a rule that was supposed to scrub medical debt from credit reports entirely. It was a massive deal. It would have helped 15 million people overnight.

Then the courts stepped in.

In mid-2025, a federal court vacated that rule. As of right now in 2026, medical debt over $500 that is more than a year old can still be reported to credit bureaus in many states. This means a single hospital bill can still tank your credit score by 20 points or more, making it impossible to get a car loan or a mortgage.

However, some states haven't waited for Washington to fix it. California, New York, and Colorado have passed their own laws. In these states, your credit report is a bit safer, but the debt doesn't just vanish—the hospitals can still sue you; they just can't ruin your FICO score as easily.

Real Numbers: The Cost of a "Small" Crisis

It doesn't take a heart transplant to ruin someone. Research from the Kaiser Family Foundation (KFF) shows that even "mid-sized" bills are causing havoc.

📖 Related: Why the Dead Bug Exercise Ball Routine is the Best Core Workout You Aren't Doing Right

| Type of Financial Strain | Percentage of Adults Affected (Approx.) |

|---|---|

| Difficulty affording any healthcare cost | 47% |

| Problems paying medical bills in the last 12 months | 28% |

| Medical debt over $250 | 9% |

| Medical debt over $3,100 (Average) | 15% of those with debt |

Honestly, the "average" medical debt of $3,100 might not sound like a lot to a CEO, but for a family living paycheck to paycheck, it's an insurmountable mountain.

The Medicaid Gap and the Uninsured Rise

As we move through 2026, we're seeing the fallout from the "One Big Beautiful Bill Act." The Congressional Budget Office (CBO) projected that nearly 15 million people would become uninsured over the next decade due to Medicaid work requirements and funding cuts.

When people lose Medicaid, they don't stop getting sick. They just stop going to the doctor until it's an emergency. Then they hit the ER, get a $20,000 bill, and the cycle of medical bankruptcies in america starts all over again.

How to Protect Yourself (Actionable Steps)

If you’re staring at a bill you can’t pay, don't just put it in a drawer and hope it goes away. That’s how lawsuits start.

1. Demand the Itemized Bill

Hospitals are notorious for "fat-finger" errors. Ask for a bill with "CPT codes." Often, just asking for this makes a few hundred (or thousand) dollars miraculously disappear as the billing department "reviews" your file.

👉 See also: Why Raw Milk Is Bad: What Enthusiasts Often Ignore About The Science

2. Check for Financial Assistance (Charity Care)

Most non-profit hospitals are legally required to have a Financial Assistance Policy. If your income is below a certain level (often up to 400% of the Federal Poverty Level), they might have to forgive part or all of your bill. You have to ask for the application; they won't just give it to you.

3. Use the "No Surprises Act"

If you went to an in-network hospital but were treated by an out-of-network doctor (like an anesthesiologist you didn't choose), they generally cannot charge you out-of-network rates. This is a federal law that has been a lifesaver for many since 2022.

4. Don't Put it on a Credit Card Yet

Once you move medical debt to a credit card, you lose all your leverage. You can't negotiate a "medical" bill with a bank. Keep the debt with the hospital as long as possible while you negotiate.

5. Consult a Consumer Bankruptcy Attorney

If the debt is over $15,000 or $20,000 and you have no way to pay, talk to a pro. A Chapter 7 bankruptcy can wipe medical debt entirely. It’s a "nuclear option," but sometimes it's the only way to get a fresh start and actually keep your house.

The medical system in 2026 is still built to prioritize the bottom line, and unfortunately, that often means the patient's wallet is the first thing to suffer. Staying informed and knowing your rights under both state and federal law is the only real defense we have left.