Honestly, if you look at your paycheck and feel like the numbers aren't quite adding up compared to what you see in the news, you aren't alone. We talk about the economy like it's one big monolith, but the median income of usa is a slippery thing to pin down. It’s the middle point—the exact spot where half of the country earns more and half earns less.

As of early 2026, the data shows a landscape that is, frankly, a bit of a mixed bag. Depending on who you ask and how they're measuring it, the median household income in the United States is hovering around $83,730. That’s the "real" median, meaning it's been adjusted for the inflation that’s been eating away at our buying power for the last few years.

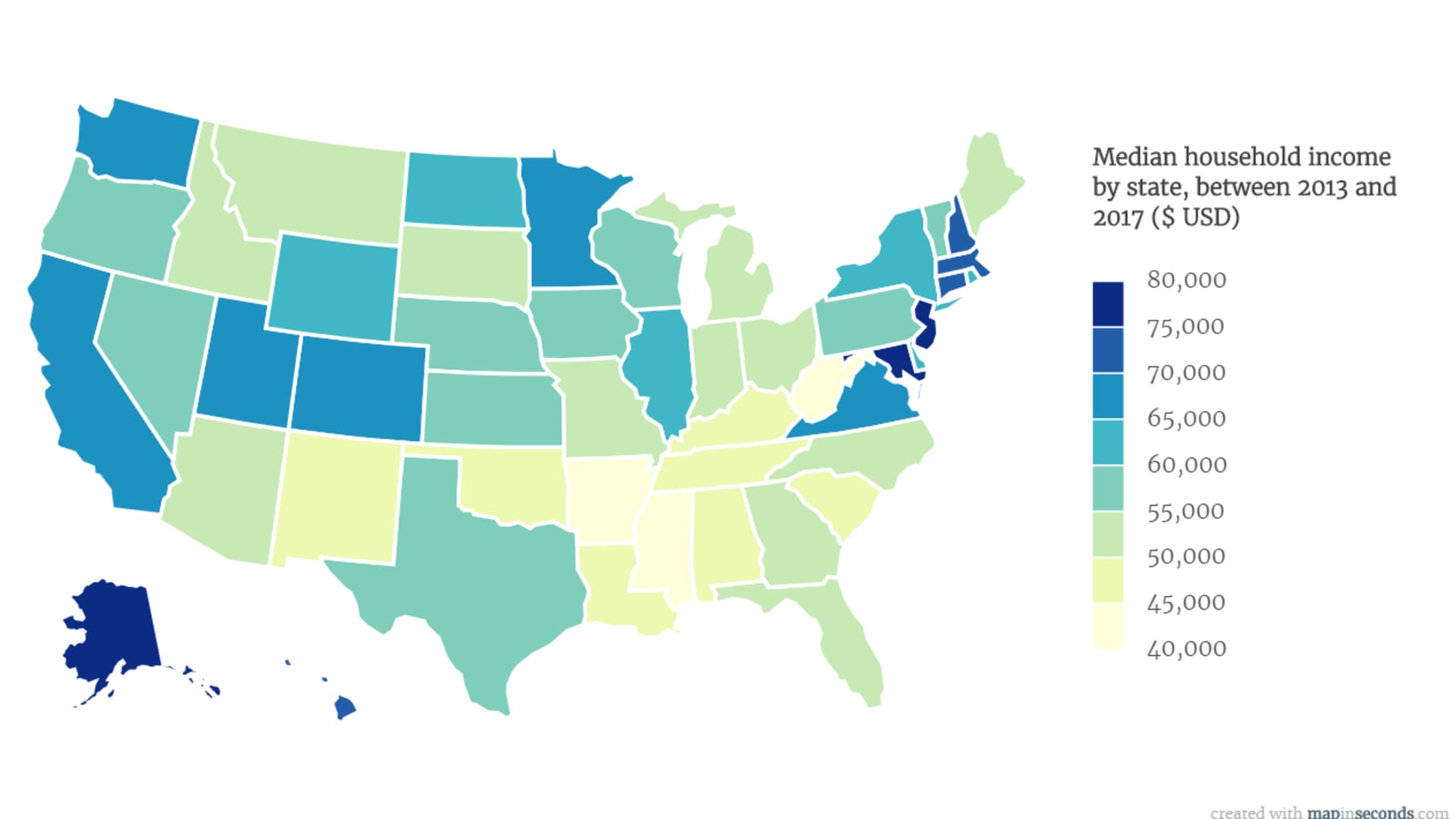

But here’s the thing: nobody actually lives in a "median" house in a "median" town. The distance between a software engineer in San Jose and a retail manager in Gulfport, Mississippi, is vast.

The Great Divide: Geography and Reality

If you’re living in Maryland or Massachusetts, that $83k might feel like you’re just scraping by. In those states, the median household income is pushing well past **$100,000**. On the flip side, in states like Mississippi or West Virginia, the numbers tell a very different story, often sitting closer to $55,000 or $63,000.

Location matters more than almost anything else. You’ve got "rich" states and "poor" states, but even that is a simplification. It’s really about the cost of living—the "hidden tax" of where you choose to park your car at night.

✨ Don't miss: Is US Stock Market Open Tomorrow? What to Know for the MLK Holiday Weekend

- Maryland: Median often hits over $109,000.

- Mississippi: Usually lags around $56,000.

- California: A massive spread, but the state median is roughly $100,000, though your money vanishes twice as fast in San Francisco as it does in Fresno.

What’s Actually Changing in 2026?

We’ve seen some weird shifts lately. For a while, wage growth was actually outpacing inflation, which was a nice change of pace. But as we move through 2026, things are cooling off. The labor market is in a "slow hiring, slow firing" phase. Employers are holding onto the people they have because they’re scared of how hard it was to find them in the first place, but they aren't exactly handing out 10% raises like they were back in 2022.

The Bureau of Labor Statistics (BLS) recently noted that average hourly earnings grew by about 3.8% year-over-year. That’s okay, but when you factor in the cost of rent and the price of a gallon of milk, that "growth" feels more like a light breeze than a tailwind.

The Education and Race Gap

It’s uncomfortable to talk about, but the median income of usa isn't distributed evenly across demographics. Education is still the biggest lever you can pull. If you have a professional degree, your median weekly earnings are likely double what someone with only a high school diploma is bringing home.

And then there's the racial wealth gap. Census data from late 2025 showed that Asian households lead the pack with a median income well over $112,000, while Black and Hispanic households continue to face systemic hurdles, with medians sitting significantly lower—often around $56,000 to $65,000 respectively. These aren't just numbers on a spreadsheet; they represent the different "starts" people get in the race.

🔗 Read more: Big Lots in Potsdam NY: What Really Happened to Our Store

Why the "Average" is a Lie

Whenever you hear someone quote the "average" income, reach for your wallet. Averages are skewed by the billionaires. If Jeff Bezos walks into a bar, the average person in that bar is suddenly a billionaire.

The median is much more honest.

Even within the median, you have to look at household size. A single person earning $80,000 is doing great. A family of five earning $80,000 is probably qualified for some form of assistance in half the states in the country. The Department of Justice actually tracks this for bankruptcy filings, and their data shows that a 4-person family often needs to earn over **$125,000** just to be considered "middle class" in high-cost areas.

The Impact of Modern Policy

Wait, there’s more. We’ve had a lot of policy shifts recently—new tariffs, changes in immigration numbers, and tax reconciliation acts. These things take time to trickle down to your bank account. The Congressional Budget Office (CBO) expects some modest growth through the end of 2026 as supply chains settle, but "modest" is the keyword there.

💡 You might also like: Why 425 Market Street San Francisco California 94105 Stays Relevant in a Remote World

We aren't in a boom, but we aren't in a freefall either. We’re in a "wait and see" economy.

Actionable Steps for Your Own "Median"

Knowing the national median is fine for trivia, but it doesn't pay your bills. Here is how you actually use this info:

- Benchmarking: Check your local "Cost of Living Index." If you earn the national median ($83k) but live in Manhattan, you are effectively earning about $35,000 in "real" purchasing power. Use tools like the Sperling’s Best Places index to see where you actually stand.

- Negotiation: If your field (like tech or healthcare) is seeing 4-5% wage growth but you haven't had a raise in two years, you are actively losing money. Use the BLS Occupational Outlook Handbook to find the specific median for your job title, not just the national average.

- Household Strategy: Since the median household income is often the result of two earners, look at your "per-person" productivity. Many families are finding that the cost of childcare actually makes the second income "negative" or "neutral" once you hit the median threshold.

- Tax Planning: As you cross into the upper-middle-class brackets (around $117,000+ for many states), your tax strategy needs to change. This is the point where standard deductions start to lose their luster and you need to look at 401(k) Max-outs or HSA contributions to keep your "taxable" median lower.

The reality of the median income of usa is that it’s a moving target. It’s a snapshot of a country trying to find its footing in a post-inflationary world. Whether you're above the line or below it, the trick is knowing how to play the hand you're dealt in the specific zip code where you live.

Next Steps for You:

- Compare your current salary against the BLS 2026 Wage Data for your specific metropolitan area to see if you’re being underpaid relative to the local median.

- Review your household’s "Real Income" by subtracting your local inflation rate (CPI) from your last annual raise to see your actual purchasing power change.

- Check the U.S. Trustee Program's latest state-by-state median income tables if you are considering major financial restructuring or qualifying for specific housing programs.