When you hear people talk about the "average" American, they’re usually imagining someone who lives in a suburban house with a white picket fence and a steady job. But if you actually look at the data, the reality is a lot more complicated. Honestly, most people get the math wrong before they even start. If you want to know what is median income in United states, you have to look past the flashy headlines and the billionaires who skew the averages.

The "average" (or mean) income is basically what happens when you take everyone’s money, throw it in a giant pile, and divide it equally. It sounds fair, but it’s a terrible way to measure real life because the top 1%—the Jeff Bezoses and Elon Musks of the world—pull that average way up.

Median income is different. It's the literal middle point. If you lined up every household in America from the poorest to the richest, the median is the person standing right in the center. Half of us make more, half of us make less. It's the most honest snapshot of how the typical American family is actually doing.

The Latest Numbers: What Is Median Income in United States Right Now?

According to the most recent data from the U.S. Census Bureau released in late 2025, the real median household income in the United States sits at $83,730.

That number might sound high to some or low to others, depending on where you live. What’s interesting—and kinda frustrating—is that even though this is a nominal increase from previous years, "real" income (which is adjusted for inflation) has been sticking around the same level. Basically, we’re making more dollars, but those dollars are buying about the same amount of groceries and gas as they did a few years ago.

The Breakdown by Category

Income isn't just one flat number. It shifts wildly depending on who you are and what your household looks like. Here is how it shakes out across different groups:

- Asian Households: These households typically see the highest median income, often hovering around $112,000.

- White (Non-Hispanic) Households: Usually come in next, around $89,000.

- Hispanic Households: Have seen some of the most significant growth lately, reaching a median of about $71,000.

- Black Households: Currently sit around $59,000, reflecting a persistent wealth gap that hasn't closed as fast as many hoped.

You also have to look at the difference between a "household" and an "individual." A household could be a single person living alone, or it could be a family of five with three people working. That’s why household numbers always look a bit "healthier" than what a single person takes home in their Friday paycheck.

💡 You might also like: Mississippi Taxpayer Access Point: How to Use TAP Without the Headache

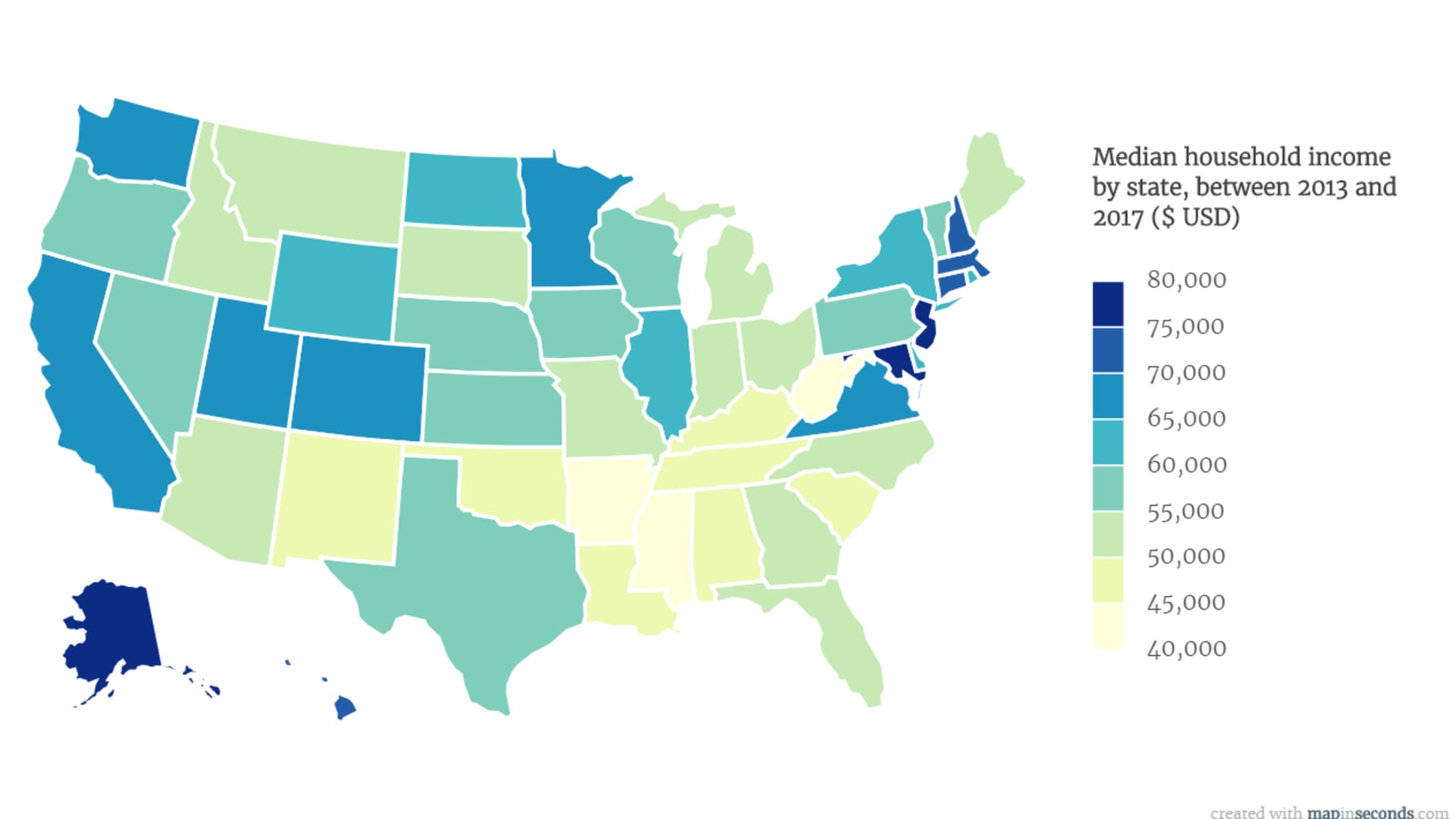

Geography is Everything

You’ve probably noticed that $80k goes a lot further in Jackson, Mississippi than it does in San Francisco. This is where the national median starts to lose its meaning.

In Maryland or New Jersey, you’ll see state medians that soar past $94,000. These states have high concentrations of government jobs, tech, and healthcare. On the flip side, in states like Mississippi or Arkansas, the median household income often struggles to break the $50,000 mark.

It’s a massive gap.

If you live in a high-cost area, you might feel "broke" even if you're technically above the national median. This is because the median doesn't account for the $3,000-a-month rent or the $15 cocktails that are standard in places like New York or D.C.

Top Earning Metro Areas

- San Jose-San Francisco-Oakland, CA: $125,015

- Washington-Baltimore-Arlington, DC-MD-VA: $113,624

- Seattle-Tacoma, WA: $109,389

- Denver-Aurora-Greeley, CO: $106,878

When you look at these cities, you realize that the national median is just a baseline. If you're a software engineer in the Bay Area, making the national median of $83,730 would actually put you quite far down the local ladder.

The Inflation Trap: Why $83k Doesn't Feel Like $83k

Inflation is the silent killer of the American dream.

📖 Related: 60 Pounds to USD: Why the Rate You See Isn't Always the Rate You Get

Between 2023 and 2026, we saw prices for "the basics"—eggs, rent, electricity—climb steadily. Even though the U.S. Census Bureau reports that the median income is up, people don't feel "richer."

Economists call this "real" versus "nominal" income. Nominal is the number on your W-2. Real is what that money can actually get you at Target.

In 2024, the median income rose about 4% in nominal terms. However, once you factor in the rising cost of living, that gain basically evaporated for a lot of families. It’s like running on a treadmill; you’re moving fast, but you aren’t really getting anywhere.

Education and the Income Ceiling

We’ve all heard that you need a degree to succeed, and the data mostly backs that up—sorta.

People with a Bachelor’s degree or higher have a median weekly earnings of about $1,747. If you only have a high school diploma, that number drops to around $980. That’s a nearly $40,000 difference over a year.

But it's not a magic bullet.

👉 See also: Manufacturing Companies CFO Challenges: Why the Old Playbook is Failing

The "cost" of that education (student loans) often eats up a huge chunk of the extra income. A person making $100k with $1,500 in monthly student loan payments might actually have less disposable income than someone making $70k with no debt.

The Gender Gap in 2026

We’re still talking about it because it’s still there.

Currently, the female-to-male earnings ratio sits at roughly 80.9%. For every dollar a man makes, a woman in a similar full-time role makes about 81 cents. This gap actually widened slightly in the last two years, which surprised a lot of analysts.

Why? Part of it is the "motherhood penalty." Women are still more likely to take time off or choose flexible roles to handle childcare, which impacts long-term salary growth. It’s a structural issue that a single "median" number can't fully explain.

Actionable Steps: How to Use This Information

Knowing the median income isn't just for trivia night. It's a tool for your own life.

- Benchmark Your Salary: If you’re making significantly less than the median for your specific city and education level, it’s time to ask for a raise or look for a new role. Use sites like Glassdoor or the Bureau of Labor Statistics (BLS) to get hyper-local data.

- Adjust for Lifestyle Inflation: If you get a raise that matches the 4% national median increase, don't go out and buy a new car. That 4% is likely just covering the increased cost of your existing life.

- Look at "Post-Tax" Realities: The Census Bureau notes that median post-tax income is often about $10,000 lower than the pretax median. When budgeting, always work off your take-home pay, not the "gross" number your boss told you.

- Consider Relocation Carefully: Moving to a high-income state like Massachusetts might boost your salary, but check the "cost of living" index first. If your income goes up 20% but your rent goes up 50%, you’re actually losing money.

The median income is a pulse check for the country. Right now, that pulse is steady, but it's under a lot of pressure from a changing economy. Whether you're above or below that $83,730 mark, the key is understanding how your specific location, industry, and education levels change the game.

Stay informed. Don't just look at the big number—look at what's happening in your own backyard.