When you hear that the median household income USA sits somewhere around $80,000, your first instinct might be to laugh—or maybe to wince. It depends entirely on where you’re standing. If you're paying $3,500 a month for a one-bedroom in San Francisco, that number feels like a fast track to poverty. If you’re living in a quiet corner of West Virginia, it feels like you've finally made it.

The Census Bureau loves their averages, but averages are messy. They mask the jagged edges of the American economy. Honestly, "median" is just a fancy way of saying "the person right in the middle." Half of the country makes more, half makes less. But the middle is moving. It’s shifting under the weight of inflation, weirdly resilient job markets, and a housing crisis that won't quit.

Let's get into the weeds of what people actually earn, because the headline figures usually miss the point.

What the Median Household Income USA Actually Tells Us Right Now

The most recent data from the U.S. Census Bureau—specifically the Income in the United States: 2023 report released late in 2024—showed a real-term increase for the first time in years. They pegged the national median at $80,610.

That sounds great on paper. It's a jump from the previous year.

But there’s a catch. Inflation is a thief. While the "nominal" income went up, the "real" income (what you can actually buy with those dollars) only recently started to recover from the post-pandemic spike in prices. You've probably felt this at the grocery store. You get a 3% raise, but eggs and car insurance go up 15%. You’re technically richer and practically poorer.

It’s also worth noting that household income isn't the same as individual salary. This is a huge distinction. A "household" could be a single mom working two jobs, or it could be three roommates in Brooklyn pooling their tech salaries. When the median household income USA rises, it sometimes just means more people are living together because they can't afford to live alone.

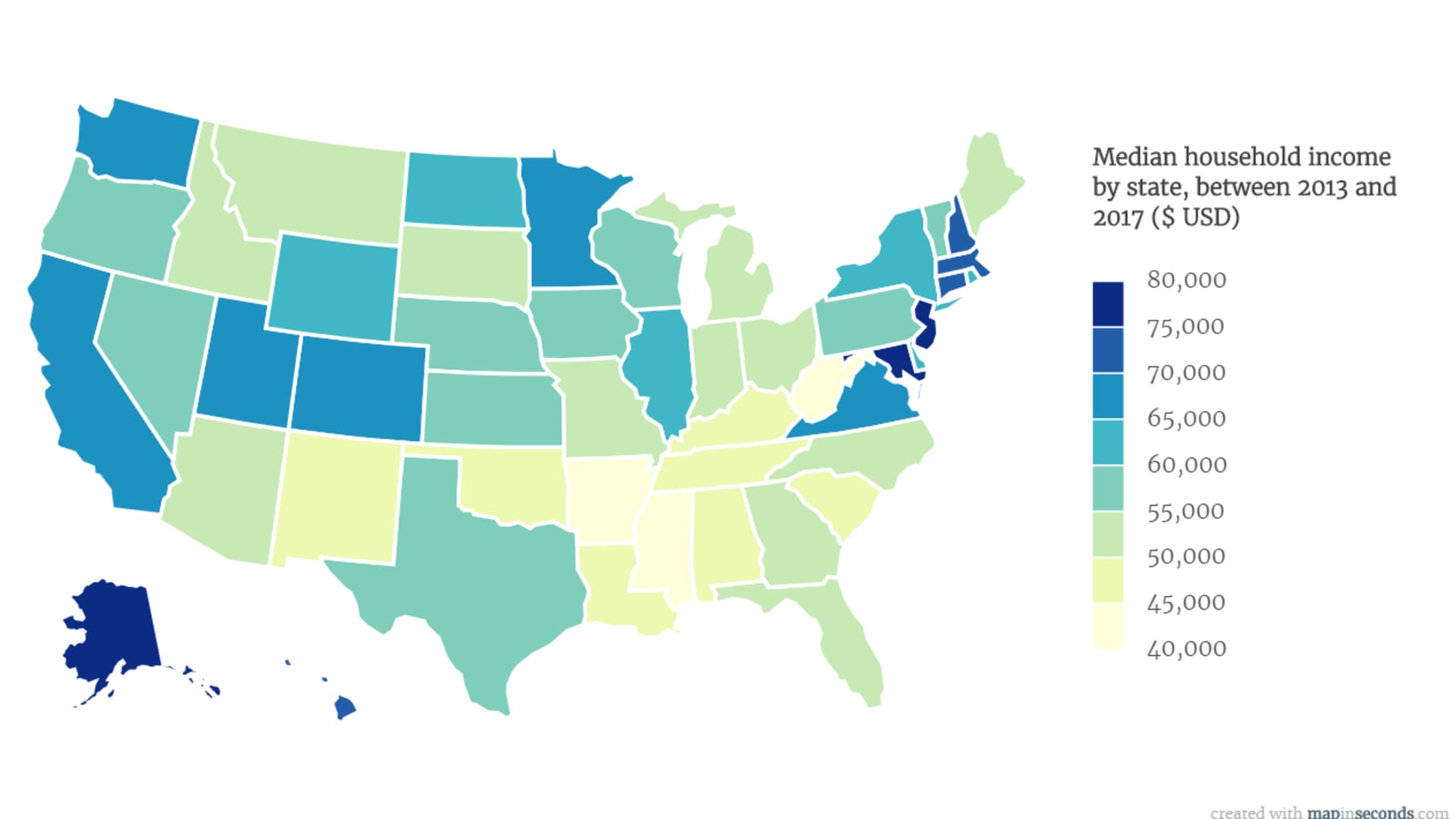

The Geography of the Paycheck

Location isn't just a factor; it's the whole game.

Maryland and New Jersey consistently fight for the top spot, often hovering with medians well above $95,000. On the flip side, states like Mississippi often see medians closer to $52,000. If you take a Mississippi salary to Maryland, you're underwater. If you take a Maryland salary to Mississippi, you're the king of the neighborhood.

But even within states, the divide is brutal. Take California. The median in Santa Clara County (Silicon Valley) is nearly double the median in some of the rural Central Valley counties. We talk about "America" as one economy, but it’s actually thousands of micro-economies stacked on top of each other.

📖 Related: Panamanian Balboa to US Dollar Explained: Why Panama Doesn’t Use Its Own Paper Money

The Disappearing Middle Class and the "K-Shaped" Reality

Economists like Peter Temin have argued that we are becoming a "dual-track" economy.

On one track, you have the finance, technology, and electronics sectors. These households are seeing their incomes soar. They have assets. They own homes with 3% mortgage rates. On the other track, you have the service sector. These households are struggling with stagnant wages and rising rents.

The median household income USA doesn't show the gap. It just shows the point where the two tracks meet.

Why your education matters more than ever

The gap between a high school diploma and a bachelor’s degree is basically a canyon at this point.

- Households headed by someone with a professional degree often see medians exceeding $170,000.

- Households with only a high school diploma usually sit around $50,000.

It’s not just about the money, though. It’s about the benefits. It’s about the 401(k) matching and the health insurance that doesn't have a $5,000 deductible. When we look at the median household income USA, we aren't seeing the "total compensation," which makes the struggle of lower-income households even more intense than the raw numbers suggest.

Age, Race, and the Wealth Gap

Age plays a massive role that people forget to mention. You don't hit your peak earning years until your 40s or 50s.

Younger households (under 25) have a median income that is often less than half of those in the 45-54 age bracket. This is normal, sort of. You gain experience, you get promoted. But the current generation of young workers is facing a unique hurdle: the cost of entry into the middle class (education and housing) has scaled way faster than the entry-level median household income USA.

Race also remains a persistent, uncomfortable factor in the data.

- Asian households consistently report the highest median incomes, often north of $100,000.

- White (non-Hispanic) households usually follow.

- Hispanic and Black households continue to trail significantly, reflecting decades of systemic barriers to high-paying industries and homeownership.

These aren't just statistics. They are reflections of who gets access to capital and who doesn't.

👉 See also: Walmart Distribution Red Bluff CA: What It’s Actually Like Working There Right Now

The Work-from-Home Ripple Effect

One of the weirdest things to happen to the median household income USA in the last few years is the geographical decoupling of work.

Suddenly, someone with a Manhattan salary could move to a small town in the Poconos. This "imported" income drives up the local median, which sounds good for the town’s tax base. But it also drives up the cost of a hamburger and a house for the people who were already there working local jobs. It’s a gentrification of the entire country, not just the cities.

Is $80,000 Actually Enough?

Short answer: No.

Longer answer: It depends on your "burn rate."

If you are a family of four living on the median income in a major metro area, you are likely living paycheck to paycheck. Between childcare—which in some states costs more than a mortgage—and transportation, that $80,000 vanishes quickly.

The Economic Policy Index (EPI) maintains a "Family Budget Calculator." If you plug in the numbers for a standard family in most US cities, the "attainable" lifestyle actually requires significantly more than the median household income USA. This is the "middle-class squeeze" you hear politicians talking about. People feel like they are doing everything right—working hard, getting the degree—and they still can't save for a rainy day.

The Hidden Costs of Being Middle Class

There’s this weird phenomenon where once you hit the median, you lose a lot of the safety nets.

You make too much for Medicaid or subsidized childcare, but you don't make enough to actually afford the private versions comfortably. It’s the "subsidy cliff." Sometimes, a small raise that bumps a household above the median can actually result in less disposable income because they lose a thousand dollars a month in childcare credits or healthcare subsidies.

It’s a trap. A mathematical, frustrating trap.

✨ Don't miss: Do You Have to Have Receipts for Tax Deductions: What Most People Get Wrong

How to use these numbers for yourself

Don't look at the national median household income USA to judge your success. It’s a tool for economists, not a yardstick for your life.

Instead, look at the "Real Median" for your specific metro area and your specific age group. If you're 30 and living in Des Moines, comparing yourself to a 55-year-old in Greenwich is just going to make you miserable for no reason.

Actionable Steps to Improve Your Household Standing

Since you can't control the national economy, you have to control your own micro-economy. Here is how you move the needle on your own household income:

Audit your "Lifestyle Creep" aggressively. Every time the national median goes up, companies find new ways to take that extra money from you. Subscriptions, premium versions of things you don't need, and the "convenience tax" of delivery apps. If your income matches the median but your savings are zero, the problem might be the "leakage" in your budget.

Negotiate based on the "Replacement Cost." Companies are currently terrified of losing "institutional knowledge." When you ask for a raise, don't talk about your rent going up—they don't care. Talk about what it would cost them to find, hire, and train someone to do what you do. That is your leverage.

Diversify the Household Income streams. The most resilient households in the median household income USA dataset aren't just relying on two W-2 salaries. They have a side hustle, a small rental property, or even just a high-yield savings account (HYSA) actually working for them. In 2026, if your money is sitting in a 0.01% interest savings account, you are losing the battle against inflation.

Upskill in "Recession-Proof" niches. Healthcare, specialized trades (plumbing, electrical), and specific AI-implementation roles are showing way more wage growth than general administrative work. If you're stuck below the median, the fastest way out is usually a pivot, not a promotion in the same dead-end role.

Understand the tax brackets. Making more money is great, but understanding "tax-advantaged" accounts like HSAs and 401(k)s can effectively increase your take-home pay by lowering your taxable income. It’s not about what you make; it’s about what you keep.

The median household income USA is a moving target. It’s a snapshot of a country in transition. Whether that number feels like a ceiling or a floor is ultimately up to your local cost of living and how you manage the gap between your earnings and your expenses. Keep your eyes on your own spreadsheet, not just the national headlines.