Money isn't everything. But honestly, it's the yardstick we use to figure out if we’re actually getting ahead or just treading water in a really deep pool. When you look at what is the median household income in united states, you aren't just looking at a dry government stat. You're looking at the literal "middle" of the American dream.

The Census Bureau dropped the latest bomb in late 2025, and the numbers are... well, they’re complicated. For 2024 (the most recent full-year data analyzed), the real median household income hit $83,730. That sounds like a decent jump from the $82,690 we saw in 2023, but here’s the kicker: when you adjust for the soul-crushing inflation we've all been feeling at the grocery store, the "real" income remained essentially flat. It’s basically the same as it was back in 2019 before the world turned upside down.

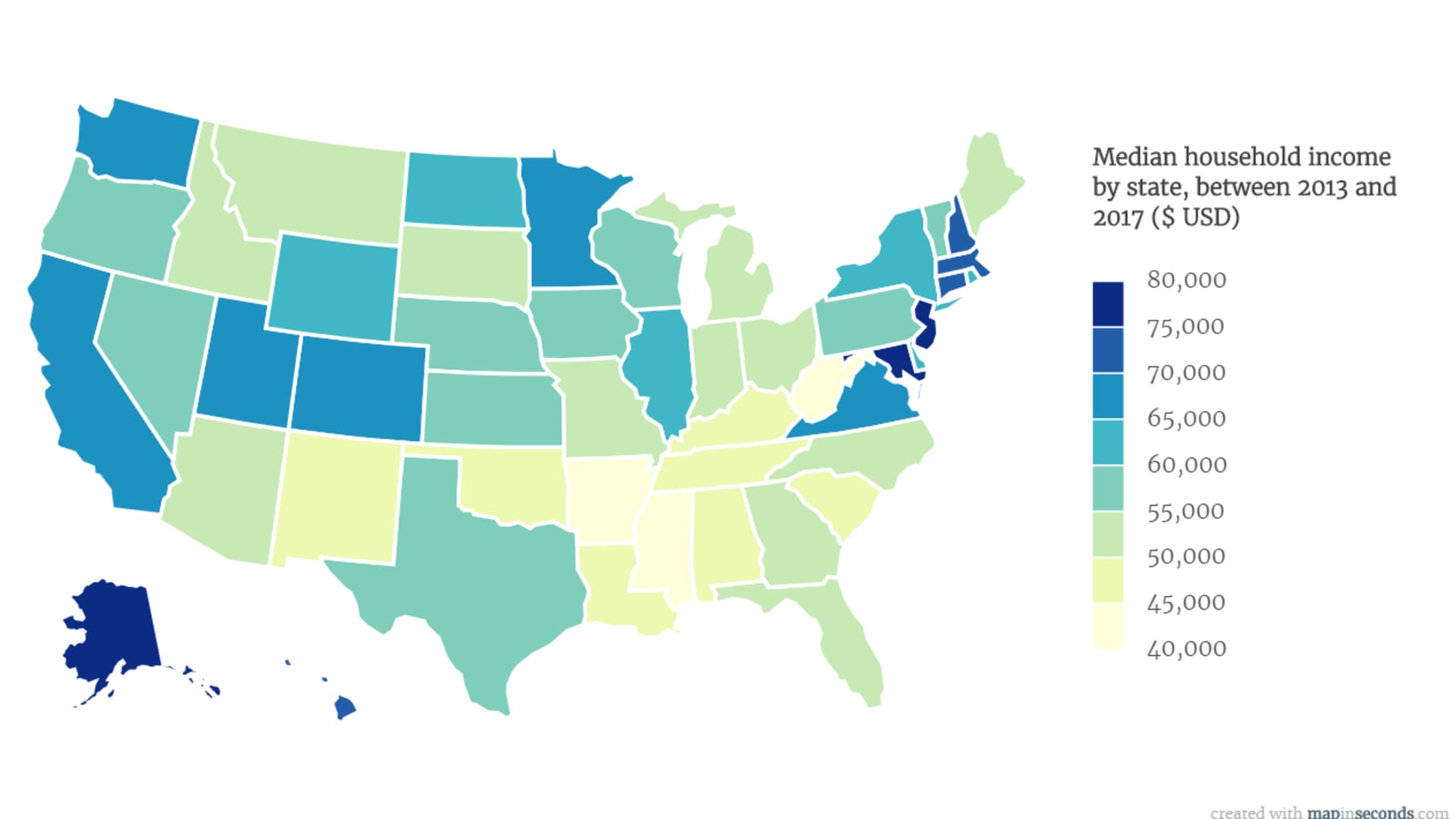

The Great Geographic Divide

You’ve probably felt it if you’ve ever moved across state lines. $83k in Mississippi makes you feel like royalty. In San Francisco? You’re probably sharing a studio with two other people and a very expensive sourdough starter.

Geography is the biggest factor that messes with these averages. According to recent 2025 releases from the U.S. Trustee Program and Census updates, the spread is wild. Massachusetts is currently leading the pack with a median clearing $113,900. On the flip side, Mississippi is still struggling to break the $60,000 ceiling, sitting at roughly $55,900.

If you’re living in the District of Columbia, the "middle" looks more like $150,381. That’s not a typo. The concentration of high-level policy jobs and tech hubs creates a bubble that most of the country just doesn't recognize as reality.

Why the "Median" Matters More Than the "Average"

Most people use these terms interchangeably. Don't do that.

✨ Don't miss: How to make a living selling on eBay: What actually works in 2026

If Jeff Bezos walks into a bar with 100 people earning $40,000 a year, the average income in that bar becomes billions of dollars. But the median—the person standing right in the middle of the line—is still making $40,000.

The median is a better "vibe check" for the working class. It filters out the outliers. Interestingly, while the median stayed flat, the top 10% of households saw their incomes rise by about 4.2% to roughly $251,000. Meanwhile, the bottom tenth only saw a 2.2% bump. The gap is widening, and you don’t need a PhD in economics to feel that tension in the air.

The Race and Education Factor

It’s uncomfortable, but the data is clear: race and education are still the biggest predictors of where you land on the income scale.

- Asian households continue to have the highest median income, surging to about $112,800 in recent estimates.

- Non-Hispanic White households hover around $89,000.

- Hispanic households showed a rare win, being the only group to see a significant 4.3% real-term increase compared to pre-pandemic levels, landing at $70,950.

- Black households actually saw a slight statistical dip, sitting around $59,500.

Then there’s the degree. If you have a Bachelor’s degree or higher, the median income sits comfortably near $115,000. If you didn't finish high school? You’re looking at a median of $37,000. That’s a massive gulf that dictates everything from where you live to how long you’ll live.

The Cost of Living Reality Check

Here is the part that usually gets left out of the headlines. Who cares if you make $83,000 if your rent is $4,000?

🔗 Read more: How Much Followers on TikTok to Get Paid: What Really Matters in 2026

In early 2026, Zillow reported that a "typical" home mortgage is finally becoming affordable in 20 major metros. But "affordable" is a loaded word. It means the mortgage doesn't eat more than 30% of that $83,730. For a long time, we were way past that. In 2024, home prices were roughly five times the median income. In the 90s, that ratio was about 3.2.

Basically, we're working harder for a house that costs a much larger slice of our pie than it did for our parents.

What This Means for You Right Now

Statistics are just numbers until they hit your bank account. If you’re feeling like you’re "behind" because you aren't hitting that $83,730 mark, remember that this number includes every person in the house over 15. It’s a collective number.

If you want to actually use this information to better your situation, you have to look at the "Real" income—what’s left after taxes and inflation. Post-tax median income is actually closer to $72,330. That’s your actual spending power.

Actionable Steps to Benchmark Your Income:

💡 You might also like: How Much 100 Dollars in Ghana Cedis Gets You Right Now: The Reality

First, check your local "Parity." Use a cost-of-living calculator to see what $83,000 in your city equals in a place like New York or Austin. You might find you're actually doing better than the national median once adjusted for your local rent and gas prices.

Second, look at your household composition. Married couples consistently report the highest medians—often crossing $120,000—simply because of the "dual-income" advantage. If you’re a single-person household, comparing yourself to the national median is like comparing a bicycle to a minivan.

Finally, watch the "Real Median" trends. If your raises aren't beating the annual inflation rate (which has been the thorn in the side of the 2024-2025 economy), you are technically taking a pay cut every year. Negotiating based on "Real" value rather than just a percentage increase is how you stay above the midpoint.

The U.S. economy in 2026 is showing signs of stabilization, but that $83,730 figure is a reminder that for most Americans, the struggle isn't about getting rich—it's about staying in the middle.

Next Steps for You:

Check the specific median income for your county through the Census Bureau’s "QuickFacts" tool to get a more accurate picture of your local economy. Then, calculate your "Price-to-Income" ratio by dividing your local median home price by your annual household income to see how your purchasing power stacks up against the 5.0 national average.