Ever feel like the numbers just don't add up? You hear the stock market is hitting record highs and the unemployment rate is sitting at historic lows, yet your bank account feels like a sieve. It’s a weird paradox. To really understand what’s happening in the pockets of American families, we have to look past the flashy GDP headlines and get into the weeds of the median household income in the us.

Most people mix up "average" and "median." Big mistake. If Jeff Bezos walks into a dive bar, the average wealth in the room shoots up to a billion dollars, but the median—the person right in the middle—is still just a regular guy with a beer. That’s why the median is the only number that actually tells you what life looks like for the middle class.

According to the most recent data released by the U.S. Census Bureau in their "Income and Poverty in the United States" report, the real median household income in the us sits at roughly $80,610.

The Inflation Hangover and the Middle Class Squeeze

Numbers are tricky. On paper, $80,000 sounds decent, right? But here’s the kicker: when you adjust for inflation, we’re basically running on a treadmill. The Census Bureau pointed out that while nominal income (the actual dollar amount on your paycheck) went up, the "real" income—what that money actually buys—has struggled to outpace the soaring costs of eggs, gas, and rent.

Basically, you’re earning more but feeling poorer. It’s frustrating.

Since the pandemic, we’ve seen a massive shift in how money moves. Between 2019 and 2022, real median household income actually dipped slightly before starting a slow, painful crawl back up. We’re currently hovering around 2019 levels. Think about that for a second. We’ve had years of technological "progress" and labor shortages that were supposed to drive up wages, yet the typical family has roughly the same buying power they had seven years ago.

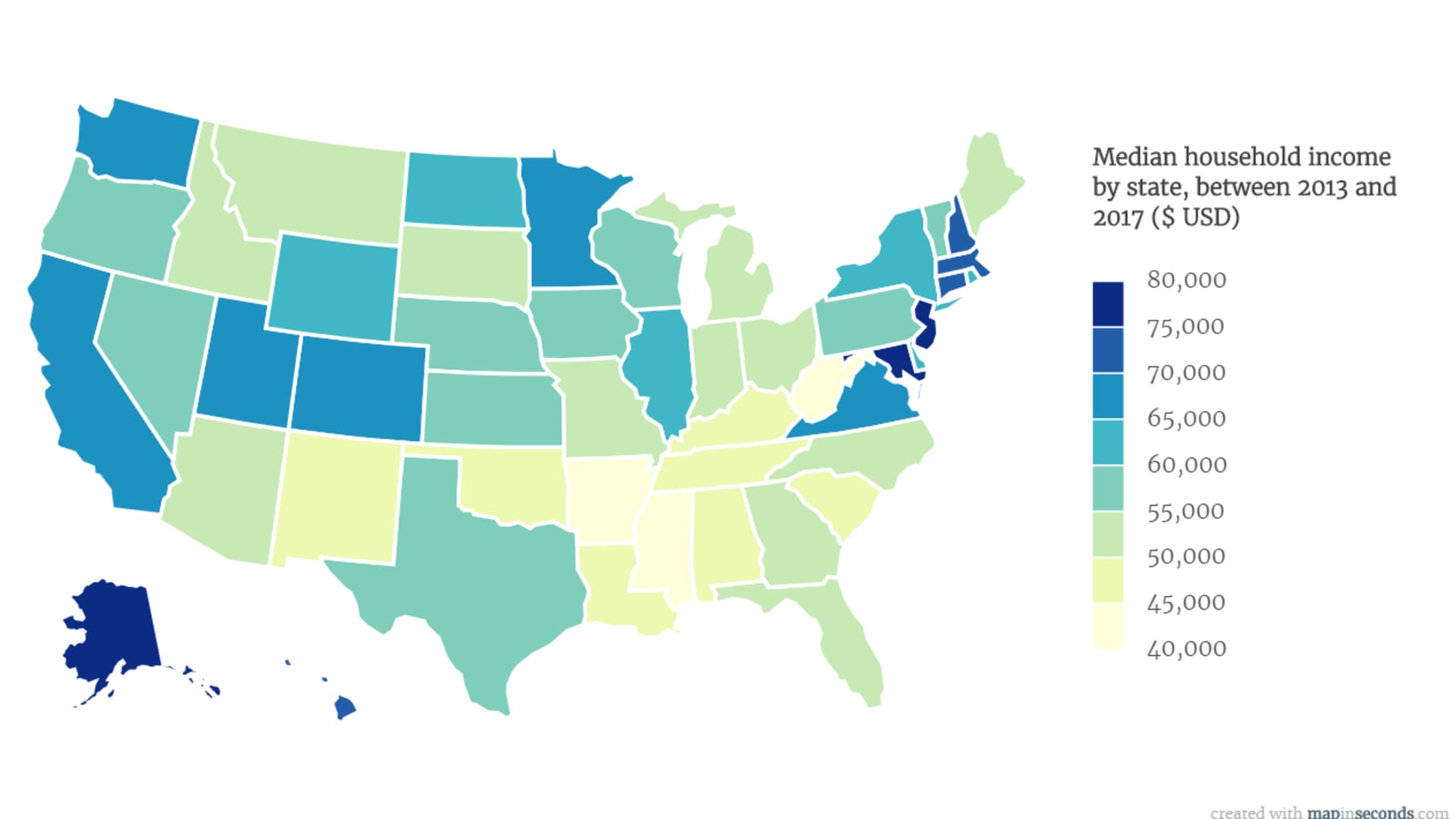

Geography is Destiny (Sorta)

Where you live matters more than almost anything else. If you’re pulling in $80k in Jackson, Mississippi, you’re living like a king. You’ve got the big house, the yard, and money left over for a boat. But take that same $80k to San Francisco or Manhattan? You’re sharing an apartment with two roommates and eating ramen.

The disparities are wild. Maryland, New Jersey, and Massachusetts consistently top the charts with median incomes often exceeding $95,000. On the flip side, states like Mississippi, West Virginia, and Arkansas often see medians closer to $55,000.

✨ Don't miss: Melissa Calhoun Satellite High Teacher Dismissal: What Really Happened

It’s not just about the paycheck. It’s the "Cost of Living Adjusted" income that matters. Economists at the Bureau of Economic Analysis (BEA) track something called Regional Price Parities. They’ve found that a dollar in Hawaii is worth about 84 cents, while a dollar in South Dakota is worth about $1.15.

Who is Actually Getting Ahead?

Education is still the biggest divider, though the "ROI" on a college degree is getting questioned more than ever. Households headed by someone with a bachelor's degree earn a median of roughly $115,000. Compare that to households headed by someone with only a high school diploma, where the median drops to around $51,000.

That’s a massive gap. Nearly double.

But even that doesn't tell the whole story. We're seeing a "hollowing out" of the middle. Low-wage service jobs are growing, and high-tech executive roles are growing, but those steady, mid-level manufacturing and administrative jobs? They’re being eaten by automation and AI.

The Age Factor

- Under 25: Median income is low, around $45,000, as people start their careers.

- 45 to 54: This is the "peak earning" window. Medians here often hit $100k+.

- 65 and over: Income drops as people move to Social Security, landing around $50,000.

It’s a bell curve. You spend your 20s broke, your 40s stressed but paid, and your 70s hoping the cost of healthcare doesn't spike.

The Race and Gender Gap That Won’t Quit

We can’t talk about the median household income in the us without addressing the elephant in the room: it’s not equal. Not even close.

🔗 Read more: Wisconsin Judicial Elections 2025: Why This Race Broke Every Record

Asian households typically see the highest median income, often crossing the $100,000 mark. White (non-Hispanic) households follow. However, Black and Hispanic households continue to trail significantly, with Black median household income often sitting nearly $30,000 below the national median.

Why? It’s a mess of systemic issues. Generational wealth, access to high-tier networking, and even just the zip code you were born in. It’s not just "hard work." It’s the starting line of the race.

And then there's the composition of the household. A "household" can be a single guy living with a dog or a family of six. The rise of multi-generational living is actually boosting the median numbers. When Grandma moves in and brings her Social Security check, or a 27-year-old moves back home, the "household" income goes up, even if everyone feels more crowded.

The Myth of the "Six Figure" Dream

For decades, $100,000 was the gold standard. If you made six figures, you had "made it."

Honestly? That’s dead.

In many US metros, $100,000 is now considered "low income" for a family of four. The Department of Housing and Urban Development (HUD) actually classifies families in the San Francisco area making $105,000 as "low income."

When we look at the median household income in the us, we have to realize that the "middle class" is becoming a very narrow tightrope. One medical emergency or a transmission failure on the car can knock a median-income family into a debt spiral.

💡 You might also like: Casey Ramirez: The Small Town Benefactor Who Smuggled 400 Pounds of Cocaine

What the Numbers Don't Show

The Census data is great, but it misses the "vibe." It doesn't track debt.

You could have a household income of $150,000, but if you’re paying $3,000 a month in student loans and $4,000 for a mortgage, you’re functionally poorer than someone making $60,000 with a paid-off house in a rural town.

Total household debt in the U.S. hit over $17 trillion recently. That’s the shadow lurking behind the income numbers. People are using credit cards to bridge the gap between their "median" income and their "actual" expenses.

Actionable Steps to Improve Your Financial Standing

If you find yourself looking at the $80,610 median and thinking, "I'm nowhere near that," or "I'm above that and still struggling," here is how to actually move the needle:

- Calculate your "Real" Local Income: Don't compare yourself to a national number. Use a cost-of-living calculator to see how your salary stacks up in your specific city. If you're in a high-cost area, a 10% raise might still leave you behind.

- Audit your "Fixed" vs. "Variable" Costs: The median household spends nearly 33% of its income on housing. If you're above 40%, you're "house burdened." Look into downsizing or refinancing if possible, though with current rates, that's easier said than done.

- Skill-Stacking: The data shows the biggest income jumps happen when workers move from "general labor" to "specialized technical" roles. You don't always need a new degree. Sometimes a $500 certification in a niche software or a trade skill can jump your income by $15k.

- Negotiate Beyond the Paycheck: If your employer can't hit the median salary you want, negotiate for remote work. Saving $5,000 a year on commuting and work clothes is the functional equivalent of a $7,000 pre-tax raise.

- Watch the Effective Tax Rate: As your income rises toward the median and beyond, you hit different tax brackets. Maxing out a 401(k) or HSA doesn't just save for the future—it lowers your taxable income today, keeping more of that "median" money in your pocket.

The median household income in the us is a useful yardstick, but it's not a destination. It’s a snapshot of a country in transition, trying to figure out how to pay for the future with a paycheck that feels like it belongs in the past. Understanding where you sit in that data is the first step toward actually beating it.

Practical Resource Checklist:

- Check the Census Bureau’s Interactive Income Map to see the median in your specific county.

- Use the Bureau of Labor Statistics (BLS) Inflation Calculator to see what your 2015 salary would need to be today to maintain the same lifestyle.

- Review your "Debt-to-Income" (DTI) ratio; lenders generally want to see this below 36% for a healthy financial profile.