Let’s be honest. Most people just click the "Married Filing Jointly" button on their tax software because that’s what society told them to do once they walked down the aisle. It feels like the natural next step, right? You share a bed, a fridge, and maybe a dog, so why wouldn't you share a tax return?

But here’s the thing.

Blindly choosing the married filing jointly tax deduction without looking at the math is a gamble. Usually, it pays off. Sometimes, it’s a disaster. The IRS isn't exactly in the business of calling you up to say, "Hey, you could’ve saved four grand if you checked a different box." You have to know the levers to pull.

The Standard Deduction Reality Check

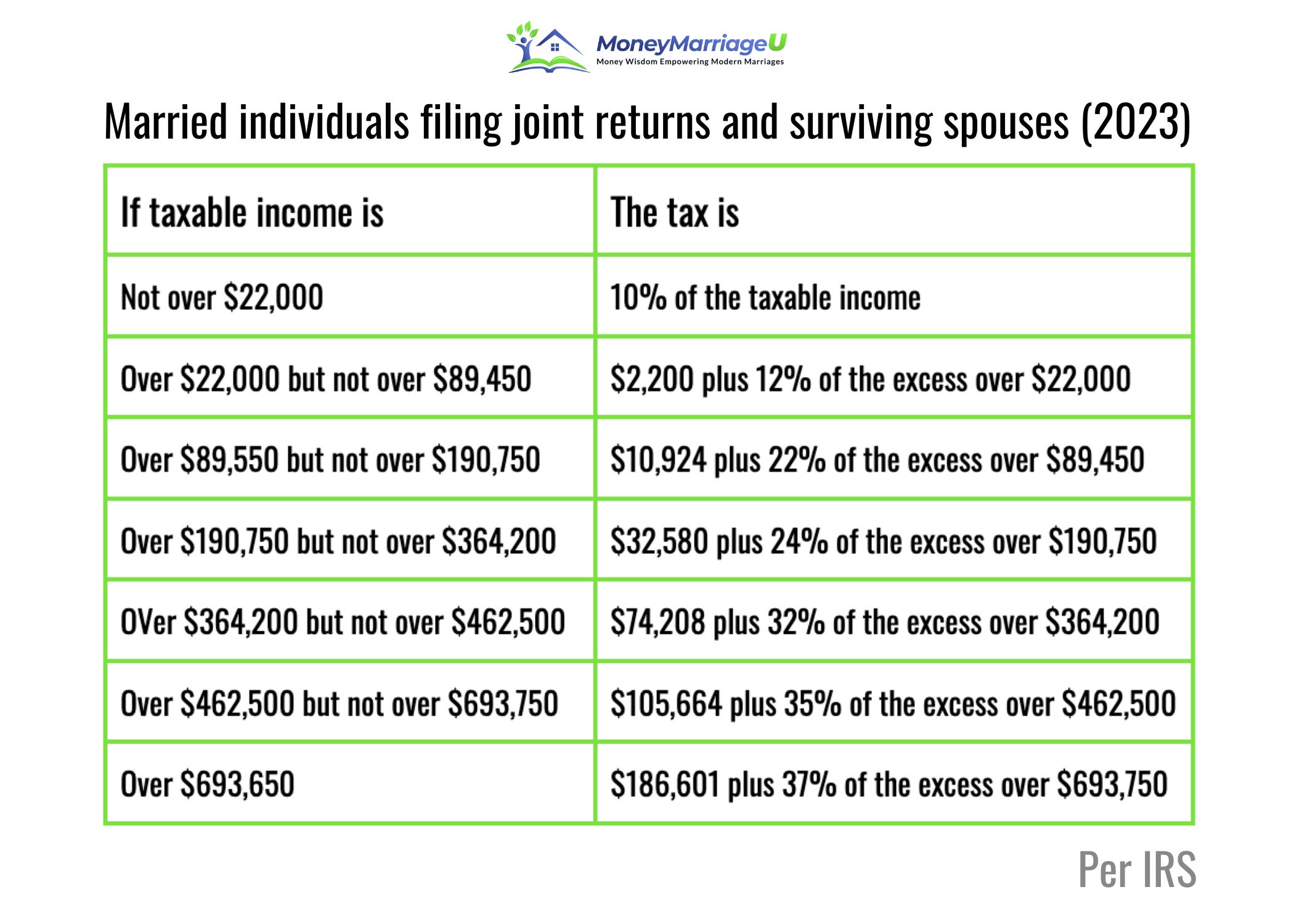

For the 2025 tax year (the ones you’re likely prepping for now), the standard deduction for married couples filing jointly jumped to $30,000. That is a massive chunk of change. If you’re a single person, you’re looking at $15,000.

Mathematically, it looks like a wash. Two singles get $30,000 combined, and one married couple gets $30,000. So where’s the "bonus"?

It’s in the brackets. The IRS stretches the income thresholds for couples. If one of you is a high earner and the other is working a part-time gig or staying home with the kids, filing jointly pulls that high income down into a lower tax bracket. It’s basically income shifting, legalized and encouraged by the federal government.

However, if you both make $150,000, that "marriage penalty" people whisper about starts to feel a bit more real, though tax reforms over the last few years have mostly neutralized it for the middle class.

🔗 Read more: Burnsville Minnesota United States: Why This South Metro Hub Isn't Just Another Suburb

When Itemizing Flips the Script

Most Americans—about 90% of us—take the standard deduction. It’s easy. It’s clean. But if you own a home in a high-tax state like New Jersey or California, or if you had a year plagued by massive medical bills, the married filing jointly tax deduction landscape changes.

If you itemize, you have to follow the leader. If one spouse itemizes, the other must itemize. You can’t have one person taking the $15,000 standard deduction while the other claims $40,000 in mortgage interest and state taxes. The IRS keeps it fair, or at least, they keep it consistent.

I’ve seen couples get burned because they didn't realize that state and local tax (SALT) deductions are capped at $10,000. That’s $10,000 per return, not per person. So, if you file jointly, you’re capped at $10,000. If you were single, you’d each get $10,000. By getting married and filing jointly, you literally lost $10,000 in potential deductions. It’s a quirk of the law that feels incredibly petty when you’re looking at a property tax bill in Westchester or Long Island.

The Student Loan Trap

This is where things get messy. Really messy.

If you or your spouse are on an Income-Driven Repayment (IDR) plan for student loans, filing jointly might be the worst financial move you ever make. Why? Because when you file jointly, the Department of Education looks at your combined adjusted gross income to calculate your monthly loan payment.

Suddenly, your $200 monthly payment triples because your spouse’s salary is now factored in.

💡 You might also like: Bridal Hairstyles Long Hair: What Most People Get Wrong About Your Wedding Day Look

In this specific scenario, people often choose "Married Filing Separately." You lose the higher married filing jointly tax deduction and some juicy credits—like the Child and Dependent Care Credit or the Earned Income Tax Credit—but you might save $800 a month on student loans. You have to weigh the tax refund against the monthly cash flow.

Real Numbers: An Illustrative Example

Think about Sarah and Marc. Sarah makes $120,000 as a project manager. Marc is finishing a PhD and making $25,000 as a TA.

If they file separately:

Sarah is taxed heavily on her $120k, hitting the 24% bracket quickly. Marc pays almost nothing.

If they use the married filing jointly tax deduction:

Their combined income is $145,000. Because the joint brackets are so wide, a huge portion of Sarah’s income that was being taxed at 24% suddenly drops into the 22% or even 12% range. They save thousands. This is the "Marriage Bonus" in its purest form. It rewards income disparity.

The "Secret" Credits You Only Get Together

The IRS dangles carrots to keep couples filing together. There are several credits that basically vanish if you file separately:

- The Child and Dependent Care Credit: Want to write off daycare? You almost certainly have to file jointly.

- Earned Income Tax Credit (EITC): This is a huge boon for lower-income earners, but it's notoriously difficult to claim if you're married but filing separately.

- Education Credits: The American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) usually require a joint return.

If you’re trying to save for a house or just survive the cost of diapers, these credits are often worth more than the deduction itself. A deduction lowers the income you’re taxed on; a credit is a dollar-for-dollar reduction in the tax you owe. Credits are king.

📖 Related: Boynton Beach Boat Parade: What You Actually Need to Know Before You Go

The Liability Headache

There’s a darker side to the married filing jointly tax deduction that nobody likes to talk about at dinner parties. It’s called "Joint and Several Liability."

When you sign that 1040 together, you are telling the IRS: "I am responsible for everything on this page, and so is my spouse."

If your partner is "creative" with their business expenses or forgets to report a side hustle, the IRS can come after you for the full amount of back taxes, interest, and penalties. Even if you get divorced later, that signature stays valid. There is "Innocent Spouse Relief," but winning that argument with the IRS is like trying to win an argument with a brick wall. It’s grueling and expensive.

How to Actually Decide

Don’t guess.

Most modern tax software will actually run a "What-If" scenario for you. It takes about ten minutes to toggle between "Joint" and "Separate" to see the bottom line.

Keep an eye on your medical expenses. If one spouse had a massive surgery and earns a lower income, filing separately might allow them to clear the 7.5% AGI threshold for deducting medical costs. If you file jointly, your combined income might be too high to deduct a single cent of those hospital bills.

Actionable Steps for This Tax Season

Stop treating your tax return like a chore and start treating it like a strategy session.

- Run the dual-scenario: Before you file, compare your total tax liability for "Married Filing Jointly" versus the combined total of two "Married Filing Separately" returns.

- Check your SALT limits: If your combined state and local taxes are way over $10,000, talk to a CPA about whether separating could help, though keep in mind the standard deduction loss usually negates this.

- Audit your student loans: If you’re on an IDR plan, use the loan simulator on the Federal Student Aid website to see how a joint return impacts your monthly payment.

- Coordinate your itemization: If you decide to itemize to take advantage of mortgage interest, ensure your spouse is prepared to do the same, even if their individual deductions are low.

- Verify your credits: Make a list of every credit you qualify for (Child Tax Credit, AOTC, etc.) and confirm they don't disappear under a "Separate" filing status.

The married filing jointly tax deduction is a powerful tool, but it's not a one-size-fits-all solution. In a world where "standard" is the default, being the person who actually checks the math is how you keep more of your paycheck. Look at your income gap, your debt obligations, and your total itemized deductions. Usually, the IRS wins when you don't pay attention. Don't let them.