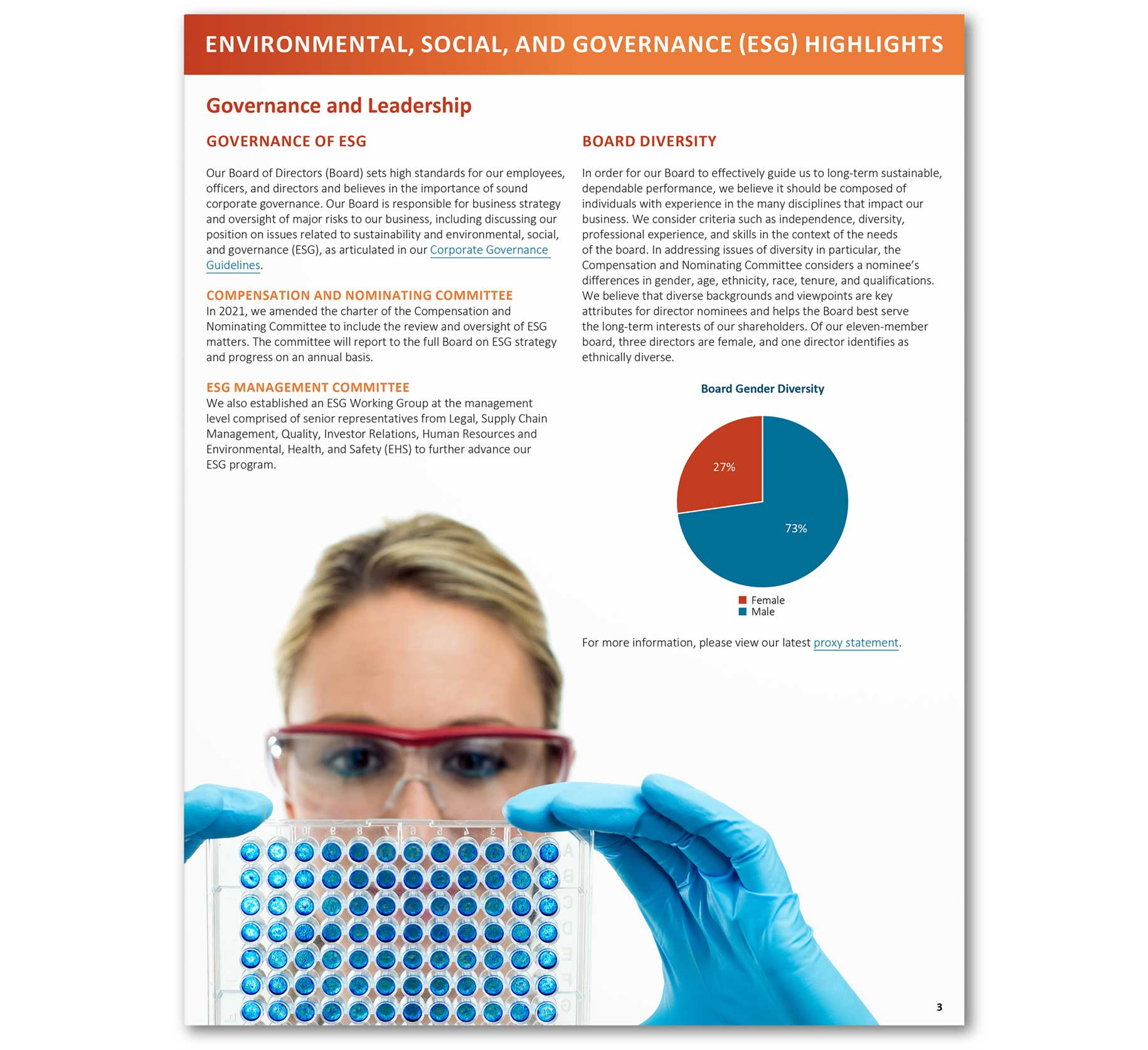

If you’ve been watching the biotech sector lately, you’ve probably noticed that things are... weird. Specifically, everyone seems to be trying to figure out if we’re in a post-pandemic hangover or a brand-new era of genomic medicine. Right at the center of that confusion is Maravai Life Sciences.

The stock has had a wild ride. Honestly, "wild" might be an understatement. We’re talking about a company that became a household name among institutional investors because it owned the "secret sauce" for mRNA vaccines—specifically their CleanCap technology. But as of early 2026, the conversation has shifted. It’s no longer just about COVID-19. It’s about whether this company can pivot fast enough to stay relevant in a world where "mRNA" is being applied to everything from cancer to rare genetic heart conditions.

Why Maravai Life Sciences stock is a different beast in 2026

Back in 2024 and 2025, the bears were screaming. They saw the plummeting demand for high-volume COVID-19 vaccine components and assumed the party was over. Revenue for the third quarter of 2025, for instance, clocked in at $41.6 million. That was a massive 39.7% drop compared to the year before. If you just look at the raw numbers, it looks like a sinking ship.

But here is what most people get wrong.

👉 See also: Wire Transfer Rate USD to INR: Why Your Bank Is Still Overcharging You

The "base business"—the stuff that doesn't involve those massive, one-time pandemic orders—is actually starting to show teeth. Maravai's subsidiary, TriLink BioTechnologies, is seeing order velocity pick up in the mid-to-late stage clinical pipeline. We aren't just talking about research kits anymore. We're talking about GMP (Good Manufacturing Practice) grade materials that are essential for drugs moving toward FDA approval.

The Officinae Bio Acquisition: A Game Changer?

In February 2025, Maravai did something smart. They completed the acquisition of Officinae Bio, an Italian firm specializing in AI-driven mRNA design.

This wasn't just a "buy-a-competitor" move. It was a "buy-the-brain" move. By integrating AI that can optimize mRNA sequences, Maravai effectively told the market: "We aren't just a chemical supplier; we are an R&D partner." This moves them up the food chain. Instead of waiting for a biotech company to tell them what to make, they can now help that company design the molecule from scratch.

Breaking Down the Numbers (The Real Ones)

Current analyst sentiment is a bit of a tug-of-war. As of mid-January 2026, the stock is trading around $3.93 to $4.00.

- The Bull Case: Analysts from firms like Wells Fargo and Zacks have been nudging their price targets upward, with some looking at a range between $4.50 and $6.50. They see the 2026 goal of positive adjusted EBITDA as a realistic milestone.

- The Bear Case: The "Zen Rating" and other quant models still flag a "Sell" or "Hold" because of the negative net income—roughly -$144.85 million annually.

- The Middle Ground: Technically, the stock is trading above its 50-day and 200-day moving averages. That's a classic signal that the floor might finally be in.

The "Lumpy" Reality of Biotech Earnings

CEO Trey Martin has used the word "lumpy" to describe their revenue, and he’s right. When you’re dealing with Biologics Safety Testing (the Cygnus segment) and Nucleic Acid Production, you don't get a smooth upward line. You get spikes.

Cygnus actually grew about 7.2% year-over-year in late 2025. This is the "boring" part of the business—testing to make sure there are no contaminants in biological drugs. But "boring" is profitable. It’s recurring. Unlike the mRNA side, which depends on clinical trial success, safety testing is required for almost everything that comes out of a bioreactor.

✨ Don't miss: Maryland Sales Tax Explained (Simply): What You’re Actually Paying and Why

The 2026 Outlook: What to Watch

We are approaching a critical earnings date, estimated for March 17, 2026. This will be the first real look at how the 2025 restructuring and the Officinae integration are hitting the bottom line.

One thing to keep an eye on is the MODTAIL technology. It’s a newer service for mRNA protein expression that launched recently. Through the end of 2025, they already had dozens of clients testing it. If those "tests" turn into "contracts," the stock could see a significant re-rating.

The Big Misconception: Is it still a "COVID Stock"?

Basically, no.

📖 Related: 5 Concourse Pkwy Atlanta GA: Why the King and Queen Towers Still Rule Perimeter Center

While Maravai still projects $10–$20 million in COVID-related CleanCap revenue for 2026, that is a tiny fraction of what it used to be. The company has spent the last 18 months trying to shed that label. They are now deeply embedded in cell and gene therapy (CGT). If you look at the 25 approved CAR-T cell and gene therapy products on the market, Maravai’s products are involved in a huge chunk of them.

You've got to realize that the market for mRNA synthesis raw materials is still projected to grow at a CAGR of about 7.1% through 2033. The "gold rush" is over, but the "mining" has just begun.

Actionable Insights for the Savvy Investor

If you're looking at Maravai Life Sciences stock, don't just stare at the 5-year chart and sigh about the 2021 highs. Those days are gone. Instead, focus on these three things:

- The EBITDA Inflection: Management is targeting 2026 for positive adjusted EBITDA. If they hit this in the Q1 or Q2 reports, it proves the business model is sustainable without pandemic tailwinds.

- Pipeline Conversion: Watch for news about their partners' Phase III trials. Maravai wins when their customers win. If a major mRNA flu or cancer vaccine hits a milestone, Maravai is the one selling the shovels for that mine.

- The European Footprint: The Venice-based Officinae Bio gives them a manufacturing hub in Europe. This is huge for avoiding some of the supply chain headaches and regulatory hurdles of shipping sensitive biological materials across the Atlantic.

The biotech sector is notoriously punishing for those who don't do their homework. Maravai isn't a "get rich quick" play anymore; it's a "bet on the infrastructure of medicine" play. It’s risky, sure. The negative free cash flow of about $5 million is a reminder that they are still spending heavily to grow. But for those who believe that the future of medicine is written in genetic code, this is one of the most direct ways to play that trend.

To stay ahead, keep an eye on the SEC filings—specifically the 10-K coming in March. Look for the "Nucleic Acid Production" segment growth excluding COVID. That’s the true heartbeat of the company. If that number moves up, the stock likely follows.

Disclaimer: I am an expert writer, not a financial advisor. Biotech stocks are high-risk. Always consult with a professional before making investment decisions based on market volatility and individual financial goals.

Key Next Steps

- Check the Moving Averages: Verify if MRVI stays above the $3.71 support level; a dip below could signal a trend reversal.

- Monitor Clinical Catalysts: Search for upcoming Phase 2 and Phase 3 data readouts from companies using CleanCap technology (like Pfizer or BioNTech).

- Review the March 17 Earnings: Pay close attention to the "Base Business" revenue growth as a percentage of total sales.