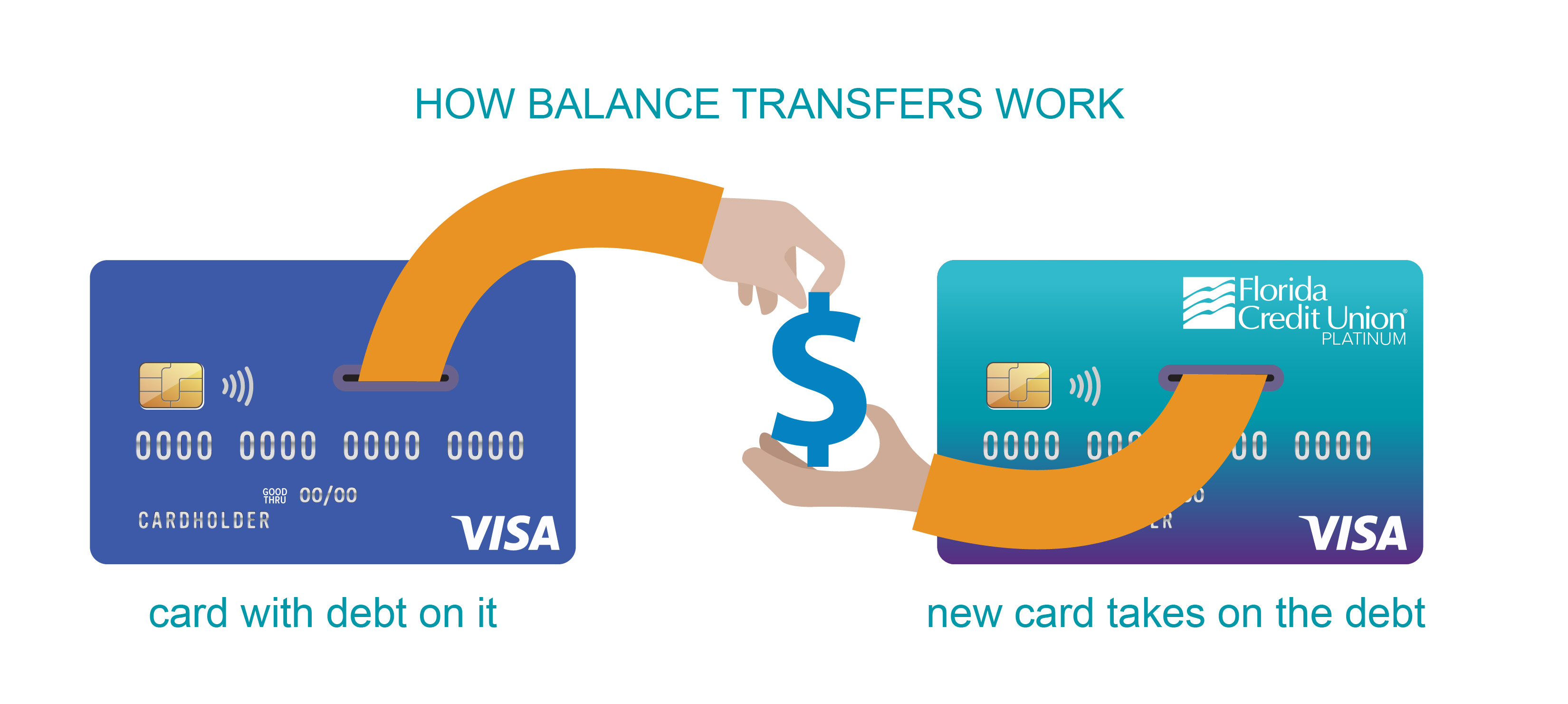

You’re staring at a $5,000 balance on a card with a 24.99% APR. It feels like trying to bail out a sinking boat with a teaspoon. Every month, you pay $150, but $100 of that just evaporates into interest charges. It’s infuriating. So, you start Googling. You see the ads. "0% APR for 18 months!" It looks like a life raft. But honestly, a low rate credit card balance transfer is a psychological trap as much as it is a financial tool. If you don't respect the math, you’re just moving piles of dirt around the backyard without actually digging a hole.

Most people think of these offers as "free money" or a "reset button." They aren't. They are a high-stakes bet the bank is making against your habits. They’re betting that you’ll see that $0 interest line item, breathe a sigh of relief, and stop being aggressive about your debt. Or worse, they’re betting you’ll use the "freed up" room on your old card to buy a new TV.

Banks aren't charities. They offer a low rate credit card balance transfer because it’s a customer acquisition strategy. They want your data, your future swipes, and they’re hoping you slip up. One late payment? Boom. That 0% or 1.9% rate usually vanishes, replaced by a "penalty APR" that can soar to 29.99%.

The Math Nobody Mentions (The Balance Transfer Fee)

Let's get real about the "low rate" part. Usually, when people talk about a low rate credit card balance transfer, they’re looking for 0% for a set period. But there is a hidden cost right at the front door. It’s called the balance transfer fee.

Most cards, like the popular options from Chase or Citi, charge between 3% and 5% of the total amount you move. If you move $10,000, you’re instantly slapped with a $300 to $500 fee. That gets added to your balance immediately. You’re starting $500 deeper in the hole. Is it still worth it? Probably. If your current card is charging you 20% interest, you’d pay roughly $2,000 in interest over a year. Paying $500 upfront to save $1,500 is a smart move. But you have to acknowledge that it isn't free.

Some cards, very rarely, offer "no fee" transfers. The UnionBank Platinum Visa or certain credit union cards used to be famous for this, though they often come with a slightly higher ongoing APR or a shorter 0% window. You have to decide: do you want a 0% rate with a 5% fee, or a 3% rate with no fee? For short-term repayment, the no-fee option often wins. For long-term breathing room, the 0% is king.

Why Your Credit Score Might Actually Drop

It sounds counterintuitive. You’re doing something responsible—managing your debt!—and yet your FICO score takes a hit. Here is why. First, you’re opening a new line of credit. That’s a hard inquiry. It’s a small ding, maybe 5 to 10 points.

Second, the "age of accounts" factor kicks in. Your credit score loves old accounts. By opening a brand-new card, you’re lowering the average age of your credit history.

✨ Don't miss: How to Sign Someone Up for Scientology: What Actually Happens and What You Need to Know

The biggest kicker is utilization. If you move $4,000 from a card with a $10,000 limit to a new card with only a $4,500 limit, that new card is now at 88% utilization. FICO hates that. It looks like you’re maxed out and desperate, even if you’re actually being savvy. You’ve gotta be careful. Don't close the old card once it’s empty. Keep it open with a zero balance to keep your total available credit high and your overall utilization low. Just... don't use it to buy tacos you can't afford.

The "Teaser" Reality and the Go-To Rate

A low rate credit card balance transfer isn't a permanent state of being. It's a "teaser." The CARD Act of 2009 actually helped us out here by requiring these promotional rates to last at least six months, but most "good" cards give you 12, 15, or even 21 months.

What happens when the music stops?

If you haven't paid off the balance by the time the promo expires, the remaining amount starts accruing interest at the "go-to" rate. This is usually the standard purchase APR, which is often tied to the Prime Rate. In today’s economy, that’s likely between 18% and 27%. If you have $1,000 left on a $5,000 transfer after 18 months, that $1,000 starts getting hit with heavy interest immediately.

Wait. It gets weirder. Some "store" cards (not typical bank cards) use "deferred interest." This is a predatory cousin of the low rate credit card balance transfer. If you don’t pay the whole thing off by the deadline, they charge you back-dated interest on the entire original amount. Thankfully, major balance transfer cards from lenders like Discover or American Express don’t usually do this, but you absolutely must read the Schumer Box—that's the little table of terms and conditions—to be sure.

Navigating the Application Minefield

You can’t just pick any card. If you already have a balance on a Capital One card, you generally cannot transfer that balance to another Capital One card. Banks don't let you swap debt within their own ecosystem. They want to steal customers from competitors, not help you avoid paying them interest.

You also need "Good" to "Excellent" credit. Typically, that means a score of 690 or higher. If your credit is in the 500s or low 600s because your utilization is already through the roof, you’re going to get denied. Or worse, you’ll get approved for a "toy limit."

🔗 Read more: Wire brush for cleaning: What most people get wrong about choosing the right bristles

Imagine you have $8,000 in debt. You apply for a low rate credit card balance transfer card and get approved... for a $1,000 limit. Now what? You’ve got a new inquiry on your report, a new account to manage, and you’ve only solved 12% of your problem. It’s a mess.

The Psychological Danger of "Empty" Cards

This is where the real damage happens. You move $5,000 to a new 0% card. Your old card now shows a $0 balance.

For many people, that $0 balance feels like a green light. "I'll just use it for emergencies," they say. Then "emergencies" becomes "a nice dinner because it was a long week." Suddenly, you have $5,000 on the new card and $2,000 on the old card. You haven't fixed your debt; you’ve just doubled your capacity to spend.

If you’re going to do a low rate credit card balance transfer, you have to address the "why." Why was the debt there in the first place? Was it a medical emergency? Fine. Was it lifestyle creep? Then the card is just a temporary bandage on a deep wound. You have to be honest with yourself. If you can't control the swipe, a balance transfer is just giving a shopaholic more rope to hang themselves with.

How to Actually Win the Game

To make a low rate credit card balance transfer work, you need a "Burn Rate" plan.

Take your total transferred balance (including the fee). Divide it by the number of promotional months minus one. If you have $5,000 to move and an 18-month 0% window, divide $5,000 by 17. That’s $294 a month.

Why 17 months instead of 18? Because you want a buffer. Life happens. If you aim to finish a month early, you won’t get caught by a surprise weekend or a processing delay that triggers the high interest rate. Set it on autopay and forget the card exists.

💡 You might also like: Images of Thanksgiving Holiday: What Most People Get Wrong

Specific Examples of Market Leaders

Right now, the landscape is dominated by a few heavy hitters.

- Wells Fargo Reflect® Card: Known for one of the longest 0% intro APR windows on the market, sometimes reaching up to 21 months from account opening on purchases and qualifying balance transfers.

- BankAmericard® credit card: Often offers a solid 18-cycle window with a competitive fee.

- Citi® Diamond Preferred® Card: Another long-hauler, though it’s pretty bare-bones on rewards.

You aren't getting cash back on these cards. You aren't getting travel points. You’re getting a "debt pharmacy." Treat it as such. Use it to get healthy, then get out.

What About Personal Loans?

Sometimes, a low rate credit card balance transfer isn't the best move. If you have $30,000 in debt, no credit card is going to give you a high enough limit to cover it. In that case, a fixed-rate personal loan might be better.

With a loan, you get a fixed monthly payment and a clear end date (usually 3 to 5 years). The interest rate won't be 0%, but it’ll be way lower than 25%. Plus, it’s an "installment loan" rather than "revolving credit," which can actually help your credit score more than a new credit card would.

But for smaller amounts—the $2,000 to $7,000 range—the credit card transfer is almost always the cheapest way to go if you have the discipline to kill the debt before the clock strikes midnight.

Your Immediate Action Plan

If you’re ready to pull the trigger on a low rate credit card balance transfer, do these four things in order:

- Audit your debt. List every card, its balance, and its APR. Move the highest APR debt first.

- Check your score. Use a free tool like Chase Journey or Capital One Eno. If you’re below 670, wait. Try to pay down some small balances first to boost your score before applying.

- Read the "Schumer Box." Look specifically at the "Balance Transfer Fee" and the "Late Payment Warning." Know exactly what the "gotchas" are.

- Hide the old card. Literally. Put it in a block of ice in the freezer or give it to a trusted friend. Do not carry it in your wallet.

The goal here isn't to have a "low rate." The goal is to have no rate because you have no balance. A transfer is just a tool to get you there faster. Don't let the tool become a crutch.