Look at the semiconductor world right now. Everyone is chasing the giants, the Nvidias and the TSMCs of the world, but there's this older player in the "back-end" of the business that keeps popping up on the radar of serious value investors. I'm talking about Kulicke and Soffa. It’s a mouthful of a name for a company that basically provides the "glue" and "stitching" for the world’s chips.

Kulicke and Soffa stock (ticker: KLIC) has been a bit of a wild ride lately. If you’ve been watching the charts in early 2026, you’ve seen it flirting with the high $50s, specifically hitting around $57.55 recently. But here’s the kicker: while some analysts are screaming "Strong Buy," others are getting cold feet. Just this week, Wall Street Zen downgraded it to a "Hold."

It’s a classic tug-of-war.

On one side, you have the AI-driven advanced packaging boom. On the other, you have the reality of a cyclical business that still depends heavily on "boring" things like cars and cheap consumer electronics. If you're trying to figure out if this is a value trap or a coiled spring, you have to look at what's actually happening on the factory floors, not just the ticker symbol.

The Advanced Packaging Hype vs. Reality

For a long time, Kulicke and Soffa was known as the king of wire bonding. Basically, they make the machines that connect a chip to its package using tiny gold or copper wires. It’s old school. It’s reliable. But it’s also a bit "last decade" when you compare it to the crazy stuff needed for AI chips.

That's where the APTURA series and Fluxless Thermo-Compression Bonding (TCB) come in.

Investors are obsessed with TCB because it’s the bridge to the future. As chips get smaller and more powerful, the old ways of connecting them don’t work anymore. You get heat issues. You get signal lag. TCB allows for much tighter connections—what the pros call "fine-pitch interconnects."

The company is betting big that half of their incremental growth in 2026 is going to come from these technology transitions. If they win the TCB war against competitors like Besi or ASMPT, the stock isn’t just a cyclical play; it’s a growth monster.

💡 You might also like: 25 Pounds in USD: What You’re Actually Paying After the Hidden Fees

But honestly? It’s a crowded space.

Besi has been winning a lot of the mindshare lately with hybrid bonding. K&S is trying to prove that their TCB solutions are more cost-effective for high-volume manufacturing. It’s a bit of a "bet on the tech" scenario.

Reading the 2026 Financial Tea Leaves

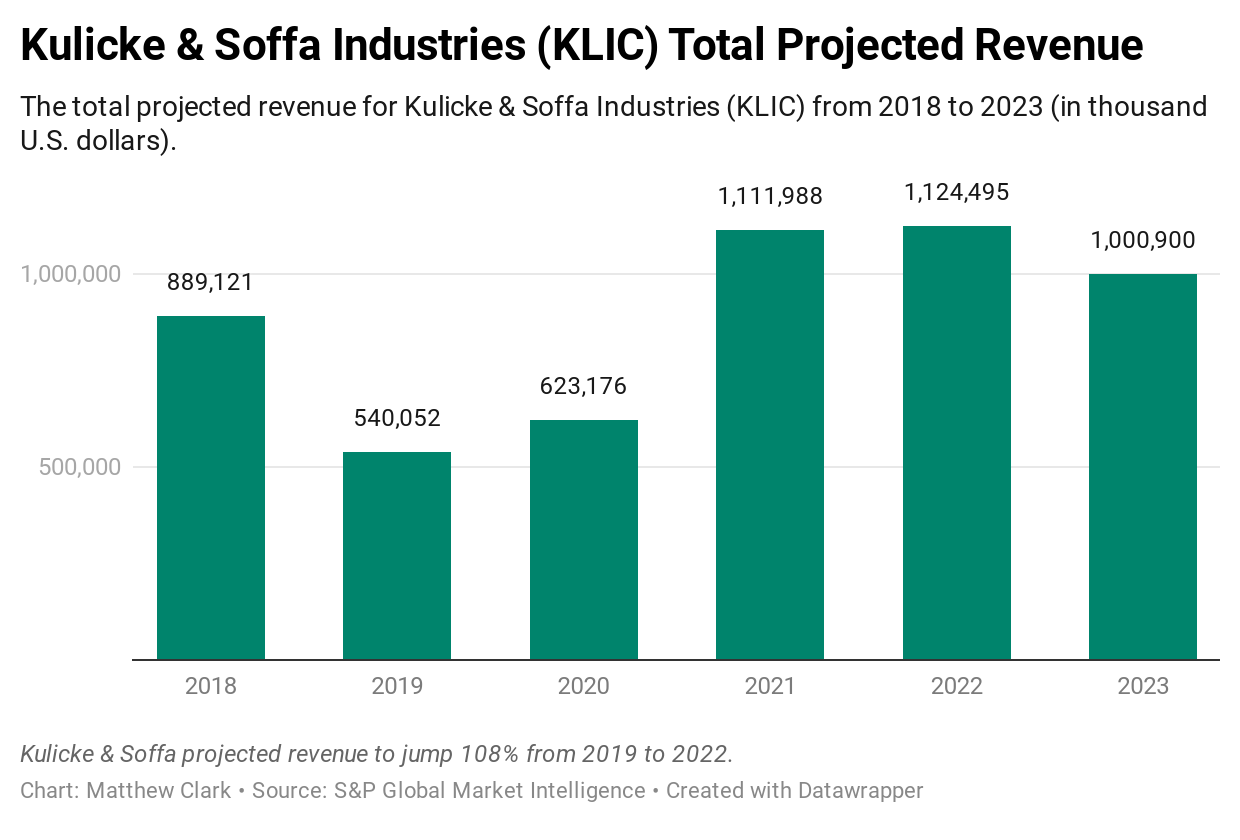

If you look at the Q4 2025 numbers that came out recently, the revenue was around $177.6 million. That’s actually a slight dip year-over-year, but they beat the street’s expectations on earnings per share (EPS), bringing in $0.28 non-GAAP.

For the first quarter of fiscal 2026, management is guiding for revenue to jump to $190 million.

Wait, why the jump? It’s the utilization rates. When semiconductor factories (foundries) are running at 50% or 60% capacity, they don’t buy new machines. They just use what they have. But right now, utilization in the memory and general semiconductor sectors is hitting 80% to 90%.

That is the "magic number" for K&S. When factories hit 80%+, they start ordering new equipment. That’s the cyclical recovery everyone has been waiting for.

The Numbers You Actually Need to Know:

- Price/Earnings Ratio: It looks wonky right now (negative on a GAAP basis) because of some one-time charges, but forward-looking analysts are projecting an EPS of $0.93 for the full year 2026.

- Dividend: They’re paying $0.205 quarterly. That’s a yield of roughly 1.4% to 1.6%. Not life-changing, but it shows they aren't bleeding cash.

- The Cash Pile: They have over $510 million in cash and short-term investments. In a world of high interest rates, having half a billion dollars in the bank and zero debt is a massive safety net.

What Most People Get Wrong About KLIC

People see "semiconductor" and think "AI." While K&S is definitely trying to get a piece of the AI pie through HBM (High Bandwidth Memory) packaging, they are still a huge play on the Automotive and Industrial sectors.

📖 Related: 156 Canadian to US Dollars: Why the Rate is Shifting Right Now

And that’s where the risk lives.

The auto sector has been "lagging a little bit," to put it in the words of interim CEO Lester Wong during the last earnings call. If the transition to Electric Vehicles (EVs) slows down or if global industrial demand stays soft, Kulicke and Soffa stock is going to feel that weight. You can't just ignore the fact that a huge chunk of their business is still tied to the stuff that goes into your car’s dashboard or your smart fridge.

Also, we need to talk about the insider selling.

Over the last three months, insiders have offloaded about 36,000 shares. Most notably, a Senior VP sold 30,000 shares at an average price of $56.53 in mid-January 2026. Usually, when the people running the company start selling near the 52-week high, it’s a sign that they think the "easy money" has been made for now.

The "Crossroads" and the China Factor

There’s a fascinating Harvard Business School case study from 2025 that basically describes K&S as being at a "strategic crossroads." They have to decide: do they keep milking the wire bonding cash cow, or do they dump all their money into high-risk, high-reward advanced packaging like hybrid bonding?

They’ve chosen a middle path. They’re buying back stock—nearly $96.5 million worth in 2025—while slowly ramping up their TCB and lithography tools.

Then there’s China.

👉 See also: 1 US Dollar to China Yuan: Why the Exchange Rate Rarely Tells the Whole Story

A massive portion of the "back-end" assembly happens in the Asia-Pacific region. If trade tensions between the U.S. and China flare up again, or if there are new export restrictions on "back-end" equipment, K&S is right in the line of fire. They aren't as protected as a "front-end" player like ASML might be with their proprietary EUV tech.

Is the Stock a Buy at $57?

The consensus target price from analysts is currently sitting around $47.25.

Do you see the problem? The stock is trading above the average analyst target. Needham is bullish with a $57 target, but B. Riley is sitting at $39. That is a massive spread. It tells you that nobody is really sure how fast the recovery is going to happen.

If you’re a momentum trader, you love the fact that the 50-day moving average ($46.49) is well below the current price. The trend is up. But if you’re a value-conscious investor, you’re looking at that 52-week high of $59.79 and wondering if there’s any room left to run.

Actionable Steps for Investors

If you're holding or looking at Kulicke and Soffa stock, don't just watch the price. Watch these three things instead:

- Foundry Utilization Rates: If you see news that major OSATs (Outsourced Semiconductor Assembly and Test) like ASE or Amkor are hitting 90% utilization, that is your green light. It means orders for K&S machines are about to explode.

- The New CEO Search: The company is currently under interim leadership after Fusen Chen retired. A "rockstar" CEO hire from a competitor could send the stock soaring. A safe, internal hire might leave the market bored.

- Advanced Packaging Revenue Share: In the next quarterly report, look for the percentage of revenue coming from "Power Semiconductor" and "Advanced Packaging." If that number isn't growing faster than the "General Semiconductor" segment, the AI story is just a story.

Kulicke and Soffa isn't a "get rich quick" AI meme stock. It’s a gritty, industrial, high-tech manufacturing play that lives and dies by the global manufacturing cycle. It’s a bet on the world needing more chips in more things—and those chips needing to be connected more reliably than ever before.

Just keep an eye on that $60 resistance level. If it breaks that with high volume, we’re in a new era. If it bounces off it again, you might get a chance to pick it up in the $40s later this year.

Next Steps for You:

Check the next earnings date (usually mid-February). If the company raises their Q2 2026 guidance above $200 million, the cyclical recovery is officially here. Also, keep an eye on SEC Form 4 filings; more insider selling at these levels would be a major red flag for a short-term pullback.