If you’ve been watching the skies lately, you’re probably not just looking for birds. You’re looking for those sleek, six-propeller electric taxis that promise to turn a two-hour gridlock nightmare into a ten-minute breeze. Joby Aviation stock performance has become a bit of a lightning rod for investors who can’t decide if they’re looking at the next Tesla or just a very expensive science project.

Honestly, the mood around JOBY right now is electric, literally and figuratively.

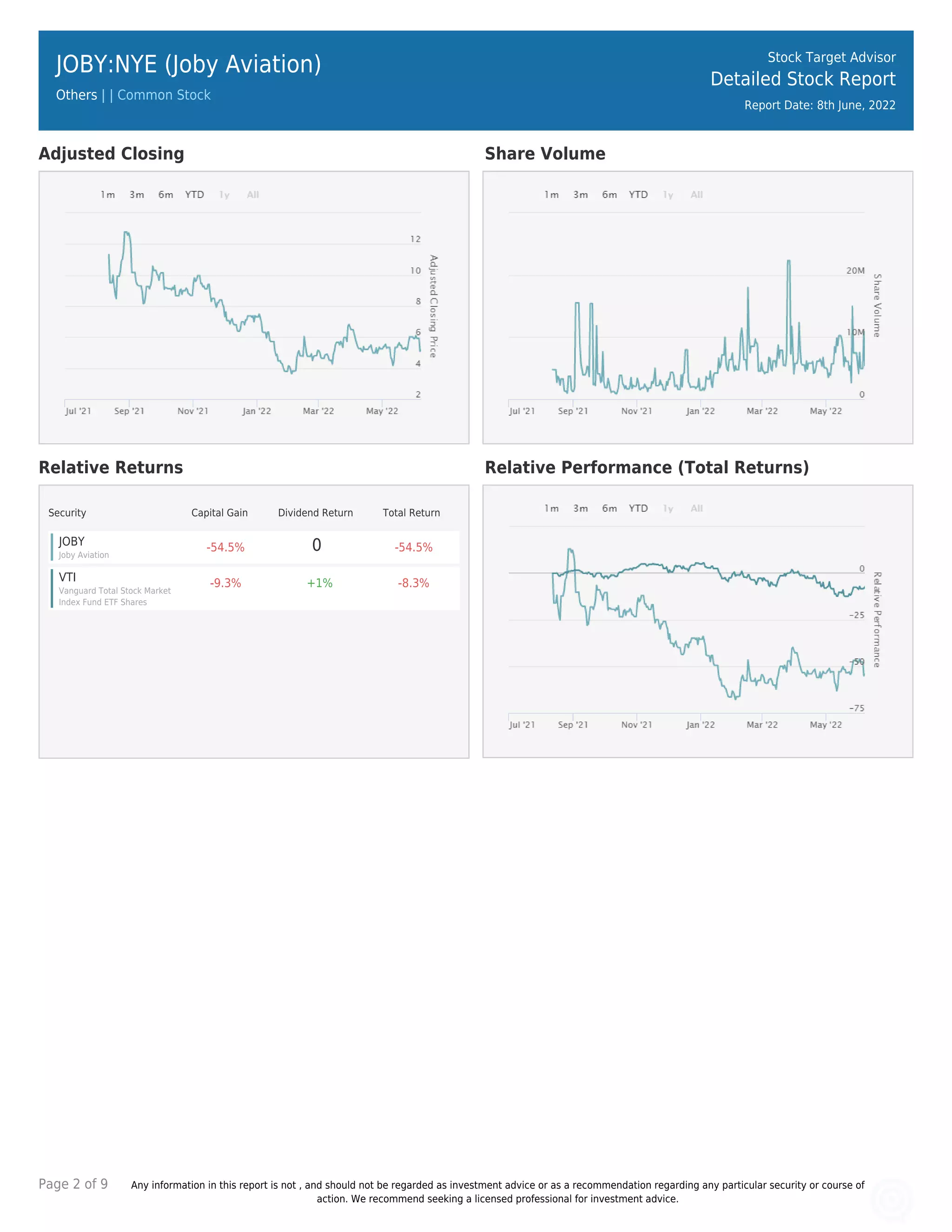

We just wrapped up 2025, and let’s be real: it was a wild ride. While the S&P 500 was busy doing its usual thing, Joby’s stock price decided to go on its own journey, surging about 62% over the year. It completely left competitors like Archer Aviation in the dust, which actually saw its valuation dip by nearly 23% in the same period.

But does that mean it’s all blue skies from here? Not necessarily.

Investing in flying cars—or eVTOLs (electric vertical takeoff and landing) if you want to sound fancy—is basically a high-stakes game of regulatory chicken. You've got massive capital burn on one side and the promise of a trillion-dollar market on the other. It’s a lot to stomach.

Why Joby Aviation Stock Performance is Defying Gravity

People keep asking why Joby is winning the "vibes" war against other eVTOL players.

Basically, it comes down to a "go-it-alone" strategy that most analysts thought was crazy a few years ago. Unlike Archer, which is piecing together parts from established aerospace giants, Joby is vertically integrated. They make their own motors. They make their own actuators. They even acquired Blade Air Mobility's passenger business in late 2025 to control the actual "hailing" part of the air taxi experience.

That move was huge.

Suddenly, Joby wasn't just a company with a cool prototype; it was a company with $23 million in quarterly revenue (as of Q3 2025). Most of that came from the Blade integration. Sure, the company still lost $401 million in that same quarter, but for the first time, investors could actually see a path to money coming in, not just going out.

The Toyota Factor

You can't talk about Joby without mentioning Toyota. They didn't just throw some pocket change at the project; they’ve poured nearly $1 billion into it.

Toyota’s engineers are practically living at Joby’s Marina, California facility. They aren't there to help with aerodynamics; they're there to teach Joby how to build thousands of these things without the wheels falling off. This partnership is probably the single biggest reason why Joby’s stock has held onto its gains while others, like the now-insolvent Lilium, crumbled.

The FAA Certification Reality Check

Here is the thing: the FAA moves at the speed of... well, a government agency.

We are currently in early 2026, and we’re entering the "Type Inspection Authorization" (TIA) phase. This is the big one. This is where FAA pilots actually get in the cockpit and say, "Okay, let's see if this thing actually does what the paperwork says."

- Milestone 1: Power-on testing of FAA-conforming aircraft (Started late 2025).

- Milestone 2: "For credit" flight testing with federal pilots (Expected H1 2026).

- Milestone 3: Full Type Certification (The "Holy Grail," projected for late 2026 or 2027).

If Joby hits these marks, the stock could moon. If there’s a battery fire or a software glitch during a TIA flight? You’re going to see a "limit down" day faster than you can say "vertiport."

🔗 Read more: Saudi Binladin Group: Why the Giant Construction Firm Still Matters in 2026

It’s also worth noting that Joby is playing it smart by looking outside the U.S. They’ve got a massive deal in Dubai for a commercial launch in 2026 and a memorandum of understanding with Saudi Arabia. Sometimes, it's easier to get things off the ground when you’re not dealing with the world's most crowded airspace first.

Analyzing the Numbers

If you look at the raw data from January 2026, the stock has been hovering around the $14 to $16 range.

Some analysts, like Chris Pierce over at Needham, have been banging the drum with a $22 price target. On the flip side, you’ve got the bears at JP Morgan who are worried about dilution. And they have a point. In October 2025, Joby did an equity raise that brought in $576 million.

Great for the balance sheet? Yes.

Great for your share of the pie? Not really. Every time they issue more stock to keep the lights on, your individual shares represent a slightly smaller slice of the company. It’s the "growth stock tax" we all have to pay.

What Most People Get Wrong About the Competition

There’s this narrative that it’s a winner-take-all market. That's probably wrong.

Think about Boeing and Airbus. Or Uber and Lyft. There’s room for two.

While Joby Aviation stock performance has been the star lately, Archer Aviation is picking up steam again in early 2026. They’ve pivoted hard toward defense contracts—over $140 million worth—and partnered with Anduril. Archer is basically saying, "If the taxis take too long, we’ll sell drones to the Air Force."

Joby is staying focused on the "Uber of the Skies" dream. They want the whole stack: the plane, the app, the pilot, and the terminal. It’s a much higher risk, but the reward is a complete monopoly on the user experience.

The "Quiet" Advantage

Have you actually heard a Joby aircraft? Probably not, and that’s the point.

One of the biggest hurdles for this stock isn't technology; it's NIMBYism (Not In My Backyard). If these things sounded like traditional helicopters, they’d be banned from Manhattan and Santa Monica in a heartbeat. Joby’s aircraft is reportedly about 100 times quieter than a helicopter.

That’s not just a "neat feature." It is the difference between a viable business and a hobby. If they can land these on top of parking garages without waking up the neighborhood, the TAM (Total Addressable Market) essentially explodes.

Practical Steps for the Curious Investor

If you're looking at your brokerage account and wondering what to do with JOBY, you've got to be cold-blooded about it. This isn't a "set it and forget it" index fund.

- Watch the TIA flight results. Any news regarding the FAA’s "for credit" testing is the only news that matters right now. Everything else is just noise.

- Monitor the cash burn. Joby has about $1 billion in the bank as of this month. At their current burn rate, that gives them enough runway into late 2027. If they announce another massive stock offering before then, it might signal that certification is taking longer than planned.

- Check the Dubai launch. If they can successfully fly paying passengers in the UAE by late 2026, it proves the business model. Once there's a "proof of concept" city, the pressure on the FAA to speed up will be immense.

- Differentiate between hype and hardware. Don't get distracted by flashy CGI videos. Look for "conforming" aircraft—that means planes built on a real production line, not hand-made prototypes.

The bottom line? Joby is the leader of the pack, but the pack is running through a minefield. You've got to decide if you're okay with the volatility that comes with literally reinventing transportation.

Keep a close eye on the upcoming Q4 2025 earnings report expected in February. That will be the first full look at how the Blade acquisition is actually impacting the bottom line and whether those "modest" revenues are starting to scale. If the revenue beat continues, $20 per share might be closer than the skeptics think.