You've probably heard the rumors. Maybe you saw a frantic headline or a TikTok "expert" shouting about a crash. Everyone wants to know if we are finally sliding into a housing market buyers market, but the reality on the ground is way messier than a simple yes or no. It depends on where you’re standing. Honestly, if you’re in Austin, Texas, it feels a lot different than if you’re trying to squeeze into a condo in Boston.

Numbers don't lie, but they do hide things.

The National Association of Realtors (NAR) recently noted that inventory levels have been creeping up, hitting roughly a 4-month supply in late 2025. In the old world—the pre-pandemic one—we used to say six months of inventory was the "magic number" for a true balance. We aren't there yet. But compared to the 2021 madness where people were waiving inspections on houses with literal holes in the roof? Yeah, things are shifting. It's a grind.

Why the housing market buyers market isn't a "sale" yet

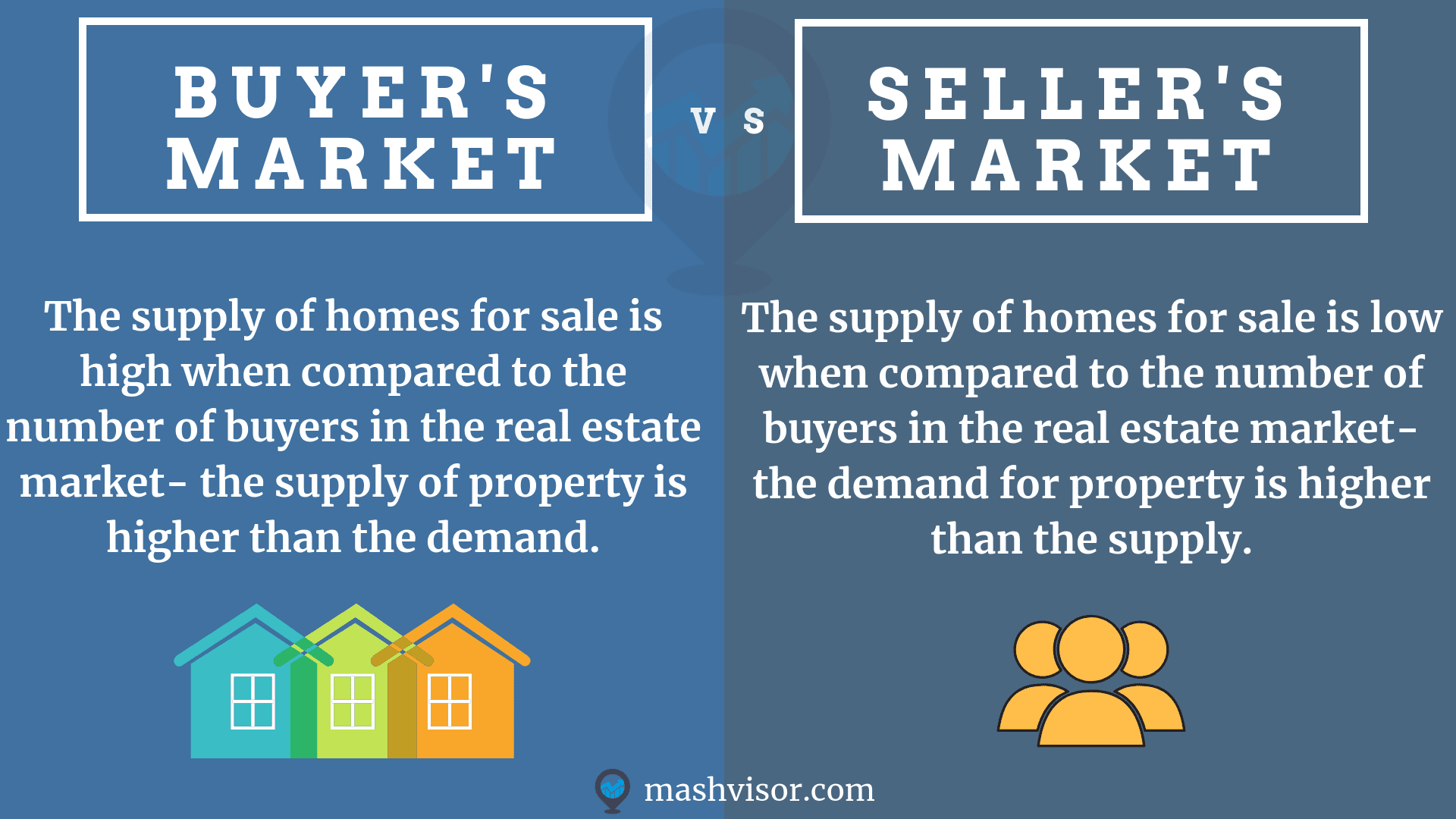

A lot of people think a buyer's market means prices are tanking. That is a huge misconception. In most of the U.S., prices aren't falling; they are just "settling." Sellers are finally realizing they can't list their home for 20% more than their neighbor did last year and expect a bidding war by Monday morning.

According to data from Redfin, a record number of sellers have had to drop their asking prices in the last few months. This is the "ego check" phase of the cycle.

When interest rates spiked, everyone froze. Sellers didn't want to lose their 3% mortgage, and buyers couldn't afford a 7% one. This "locked-in effect" basically broke the market for a while. Now, we are seeing a "thaw." People have to move eventually. Life happens. Babies are born, people get divorced, and jobs change states. This forced movement is what creates the opening for a housing market buyers market to actually take shape.

But here is the kicker: high rates actually help buyers who have cash or high equity.

🔗 Read more: Where Did Dow Close Today: Why the Market is Stalling Near 50,000

If you aren't fighting fifty other people, you have leverage. You can ask for repairs. You can ask for a closing cost credit. You can breathe. That’s the real win right now—not necessarily a lower price tag, but the ability to actually think before you sign away thirty years of your life.

The regional divide is getting weird

You can't talk about the national market anymore because the national market doesn't exist. It’s a collection of thousands of tiny, hyper-local bubbles.

Take Florida.

In places like Cape Coral or parts of Miami, inventory is exploding. Why? Insurance costs are absolutely nuking the math for a lot of homeowners. When your monthly escrow payment jumps by $400 just because of home insurance premiums, you sell. That creates a local housing market buyers market because the supply is outstripping what people can actually afford to carry monthly.

Compare that to the Northeast. In suburban New Jersey or certain pockets of Connecticut, supply is still a joke. It’s a desert. You might still see five offers on a decent ranch house because there just isn't anything else to buy.

The psychology of the "Wait and See" crowd

I talk to people every week who say they are waiting for rates to hit 5% again. Good luck.

💡 You might also like: Reading a Crude Oil Barrel Price Chart Without Losing Your Mind

If rates hit 5%, every single person currently sitting on the sidelines is going to sprint back into the market at the exact same time. What happens then? Prices go up. You end up in the same financial position, just with more stress.

Expert analysts like Lawrence Yun have pointed out that the supply-demand imbalance is a multi-year problem. We didn't build enough houses for a decade after 2008. You can't fix a 4-million-home shortage overnight just because interest rates moved a point.

Negotiating when you finally have the upper hand

So, let's say you find a house. It’s been sitting for 45 days. In 2022, a house sitting for 45 days meant it was probably haunted or built on a swamp. Today? It just means it was overpriced.

This is where you get to be a bit of a jerk, respectfully.

- The 2-1 Buy-down. Instead of asking for a $10,000 price cut, ask the seller to pay for a mortgage buy-down. This drops your interest rate for the first two years. It saves you way more on your monthly payment than a small price reduction ever would.

- Inspection Leverage. Don't waive it. Ever. In a housing market buyers market, the inspection is your best friend. If the roof is ten years old, ask for a credit. The seller knows if they go back on the market, the next buyer will find the same thing.

- The "Days on Market" psychological edge. Once a house hits the 60-day mark, sellers get desperate. They start imagining the house never selling. That is when you come in with a "clean" offer—no weird contingencies, just a solid price and a quick close.

What most people get wrong about "The Crash"

We are obsessed with 2008. It was a trauma for the whole country. But the math today is fundamentally different. Back then, we had "ninja" loans—No Income, No Job, no Assets. People were buying three houses with zero down and a prayer.

Today, lending standards are actually pretty strict. Most people sitting in homes right now have a ton of equity. Even if the market dips 10%, they aren't underwater. They aren't going to be forced into foreclosure in mass numbers. Without a wave of foreclosures, you don't get a 2008-style price collapse. You just get a slow, boring stagnation.

📖 Related: Is US Stock Market Open Tomorrow? What to Know for the MLK Holiday Weekend

And honestly? Boring is good. Boring is where you can actually find a home you like without crying in a parking lot after losing your fourteenth bidding war.

Actionable steps for the current climate

If you're looking to jump in, stop watching the national news and start looking at specific zip codes.

Track the inventory-to-sales ratio in your specific town. If you see houses staying on the market longer than 30 days consistently, the power is shifting to you.

Get a local lender. Big national banks are slow and don't care about your local market quirks. A local loan officer can tell you exactly which programs are available for first-time buyers in your specific county, some of which offer "silent" seconds or down payment grants that go unused because nobody asks.

Check the "expired" listings. Sometimes a house doesn't sell because the agent was bad or the photos were terrible. If a listing expires, it doesn't mean the seller doesn't want to sell; it means they are frustrated. Have your agent reach out. You might get a deal before it even hits Zillow again.

Look at new construction. Builders are hurting more than individual sellers because they have massive loans to pay back. They are often willing to throw in "free" upgrades, finished basements, or massive financing incentives just to get the inventory off their books before the quarter ends.

The housing market buyers market isn't a single event—it's a series of small wins for people who are patient enough to look for them. Stop waiting for a "crash" that might never come and start looking for a seller who is tired of waiting. That is where the real money is made.