Tax season is usually a mess of anxiety and caffeine. You look at your paycheck, see a chunk of change missing, and wonder where it actually goes. Understanding the IRS tax brackets 2024 isn't just for accountants or people who enjoy reading 500-page tax codes for fun. It’s for you. If you don't know how these tiers work, you're basically flying blind with your finances.

Most people think if they "jump" into a higher bracket, all their money gets taxed at that higher rate. That is totally wrong. Seriously. That’s not how the math works at all.

✨ Don't miss: CIEN Stock: What Most People Get Wrong About the AI Networking Boom

The Progressive Myth and IRS tax brackets 2024

Our system is progressive. This means your income is like a bucket that overflows into different jars. The first jar is taxed at a tiny 10%. Once that’s full, the next bit of money pours into the 12% jar. You only pay the higher rates on the specific dollars that land in those higher buckets.

For the 2024 tax year—which is the stuff you're filing right now in early 2025—the IRS shifted the goalposts. They do this because of inflation. If they didn't, "bracket creep" would happen. That's when you get a cost-of-living raise, but because the tax brackets stayed the same, you actually end up poorer because you're paying more in taxes despite having the same purchasing power.

The IRS adjusted these levels by about 5.4%. It’s a bit of a silver lining if your wages didn't keep up with the price of eggs and gas.

Breaking Down the Single Filer Tiers

If you’re filing solo, here is the raw deal. For the 10% bracket, we are looking at income up to $11,600. Once you make $11,601, you hit the 12% tier, which goes all the way up to **$47,150**.

Now, if you're a mid-career professional making, say, $85,000, you aren't paying 22% on all of it. You pay 10% on the first chunk, 12% on the middle chunk, and 22% only on the amount over $47,150. It’s a ladder. You climb it rung by rung.

The 24% bracket starts at $100,525. This is where things get "kinda" pricey for the upper-middle class. From there, it jumps to 32% for income over $191,950, then 35% at $243,725, and finally, the big 37% "millionaire" tax for anyone making over $609,350.

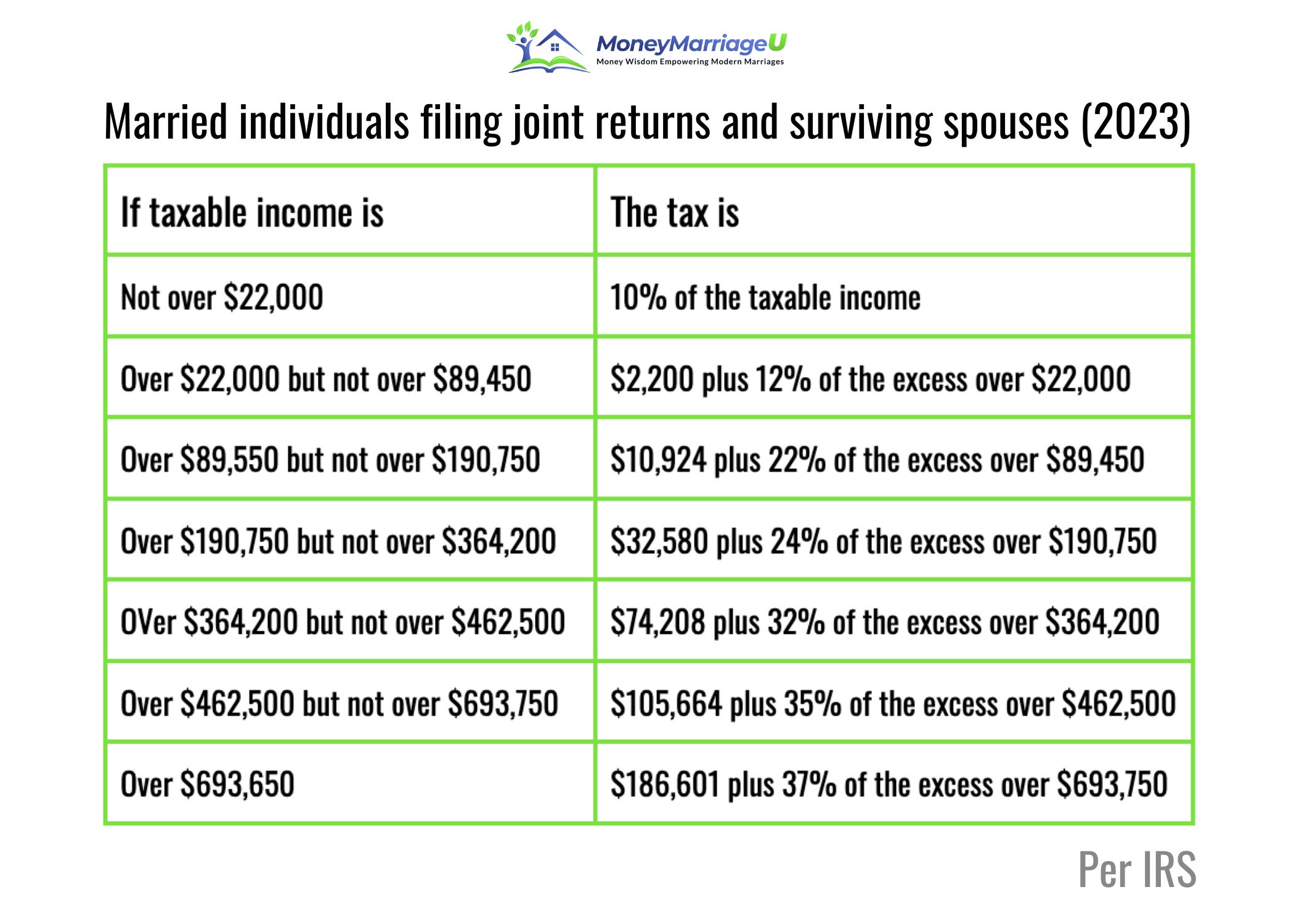

What about Married Couples?

Filing jointly changes the math. Basically, the IRS doubles most of the thresholds. For 2024, that 10% bracket covers up to $23,200. The 12% bracket stretches to $94,300.

Why does this matter? Well, if one spouse makes $90,000 and the other makes $5,000, filing together keeps almost all of that income in the 12% range. If they were single, the high earner would be getting walloped at 22%. It’s the "marriage bonus" that people talk about, though it doesn't always work out perfectly if both people are high earners.

Head of Household: The Middle Ground

There's this third category people often overlook. If you're unmarried but pay more than half the cost of keeping up a home for a qualifying person (usually a kid or a relative), you get better rates than a single person.

The 10% limit here is $16,550. The 12% goes up to $63,100. It’s a massive help for single parents who are already stretched thin by childcare costs and life in general.

The Standard Deduction: Your Secret Weapon

You can't talk about IRS tax brackets 2024 without mentioning the standard deduction. This is the amount of money the IRS just... ignores. You don't pay taxes on it. Period.

For 2024:

- Single filers get $14,600.

- Married filing jointly gets $29,200.

- Head of household gets $21,900.

If you're a single person making $50,000, you subtract $14,600 right off the top. Your "taxable income" is actually $35,400. That is the number that determines which bracket you land in. You might think you're in the 22% bracket based on your salary, but after the deduction, you're safely tucked away in the 12% tier.

It’s a huge distinction. People panic for no reason.

Marginal vs. Effective Rates

Your marginal rate is that "top" bracket you hit. If you're in the 24% bracket, your marginal rate is 24%. But your effective rate is the actual percentage of your total income that goes to the IRS.

👉 See also: Interest Rates Historical US: What Most People Get Wrong About Cheap Money

Honestly, most people’s effective rate is way lower than they think. If you earn $100,000, your effective rate might only be 14 or 15% after you factor in the lower brackets and deductions. Understanding this helps when you're deciding whether to take a bonus or a raise. You’ll almost always take home more money with a raise, even if it pushes you into a higher marginal bracket. The "I'll make less money if I get a raise" thing is a total myth.

The only exception is if you lose certain government benefits that are "cliff-based," but for the actual tax math? More is always more.

Strategic Moves to Lower Your Bracket

Knowing the IRS tax brackets 2024 allows you to play the game better. If you're hovering right at the edge of the 24% bracket, you might want to shove some extra money into a traditional 401(k) or an IRA.

Contributions to these accounts are "above the line" deductions. They lower your taxable income. If you're $5,000 into the 24% bracket, putting $5,000 into a 401(k) effectively keeps that money from being taxed at all this year. You’re essentially "paying yourself" instead of paying the government.

Health Savings Accounts (HSAs) are even better. They’re triple-tax-advantaged. The money goes in tax-free, grows tax-free, and comes out tax-free for medical stuff. It’s the closest thing to a "cheat code" in the tax world.

Capital Gains: A Different Beast

Don't confuse your salary tax with your investment tax. If you sell stocks you’ve held for more than a year, that money is taxed at Long-Term Capital Gains rates.

These are 0%, 15%, or 20%.

Most people fall into the 15% category. However, if your total taxable income (including those gains) is under $47,025 as a single person, you might pay 0% in federal taxes on those investments. That is a massive opportunity for retirees or people in lower-income years to lock in some profits without giving the IRS a dime.

Common Mistakes to Avoid

- Ignoring the W-4: If you got a huge refund last year, you’re giving the government an interest-free loan. If you owed a ton, you’re risking penalties. Adjust your withholding based on the 2024 brackets.

- Forgetting State Taxes: These brackets are only for federal. Your state probably has its own brackets, and they don't always align.

- Missing Credits: Brackets determine what you owe, but credits (like the Child Tax Credit) are dollar-for-dollar reductions in your tax bill. A $2,000 credit is worth way more than a $2,000 deduction.

Taking Action Today

The 2024 tax year is technically over in terms of earning, but you have until the April 2025 filing deadline to make certain moves.

First, go grab your last pay stub from December 2024. Look at your "Year to Date" gross income. Subtract your standard deduction. Now, look at the brackets mentioned above. Where do you land?

✨ Don't miss: Hows the Stock Market Doing: What the Charts Aren't Telling You Right Now

If you realize you're just a few thousand dollars into a higher bracket, you still have time to contribute to a traditional IRA (for the 2024 tax year) until the April filing deadline. This can retroactively lower your taxable income and potentially move you down a bracket.

Second, check your withholding for 2025. Since the brackets shifted again for the new year, you might want to use the IRS Tax Withholding Estimator tool. It’s a bit clunky, but it’s the most accurate way to make sure your 2025 taxes are on track so you don't get a surprise bill next year.

Third, organize your receipts for "above the line" deductions. Things like student loan interest (up to $2,500) and educator expenses for teachers are deducted before you even get to your bracket math. Having these ready will make the filing process significantly less painful.