It was supposed to be the "golden age" for accounting. Back in 2021 and 2022, everyone was talking about a massive talent shortage. Firms were desperate. The IRS was flaunting an $80 billion budget boost to hire 87,000 people. PwC was promising to add 100,000 new heads to its global roster.

Then 2024 and 2025 hit.

The narrative didn't just shift; it basically did a backflip. Instead of hiring binges, we started seeing headlines about cuts. Thousands of people who thought they were entering the most "recession-proof" career on the planet suddenly found themselves staring at severance packages or rescinded offers. If you’re one of the IRS PwC accounting layoffs applicants trying to make sense of this mess, you aren’t alone. Honestly, it’s been a weird couple of years for the profession.

The PwC Pivot: From 100k New Hires to "Recalibration"

Let’s look at PwC first because their situation is a classic case of over-promising and under-delivering on headcount. In late 2025, the firm’s annual report revealed they had actually trimmed their global workforce by about 5,600 people during the fiscal year. This was a massive departure from that 100,000-person hiring pledge made by former chair Bob Moritz.

What happened?

PwC leaders called it "recalibration." In May 2025, the firm cut about 1,500 U.S. roles, mostly in audit and tax. They blamed "historically low attrition." Basically, people weren't quitting as often as they used to. In the Big Four world, the business model relies on "up or out"—a certain percentage of people are supposed to leave every year to make room for new blood. When the exit door stayed shut, PwC had to push people through it.

It wasn't just "underperformers"

If you were an applicant or a recent hire during this time, the "low attrition" excuse felt like a slap in the face. Many of those let go were early-career professionals. Some had been at the firm for less than a year. One junior staffer told the Financial Times they were "completely blindsided" by a Microsoft Teams meeting that ended their career before it even really started.

📖 Related: 53 Scott Ave Brooklyn NY: What It Actually Costs to Build a Creative Empire in East Williamsburg

Wait. It gets more complicated.

While they were cutting staff, they were also dumping $1.5 billion into AI. The firm says the layoffs weren't "caused" by AI, but when you invest billions into "next-generation AI capabilities" and then cut 2% of your workforce, the optics are... well, they're not great.

The IRS U-Turn: Budget Wars and Pink Slips

If the private sector was shaky, the public sector was a total rollercoaster. The IRS, once the promised land for stable accounting careers, underwent a radical transformation under new administration priorities.

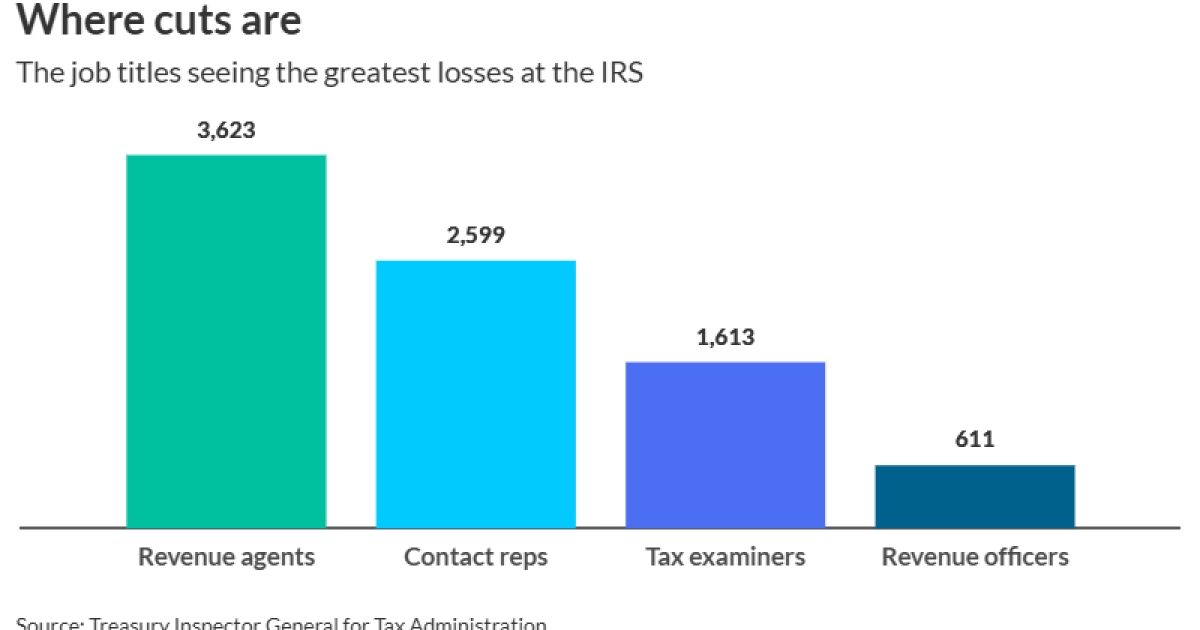

By early 2025, the agency wasn't just slowing down hiring—it was actively purging. A report from the Treasury Inspector General for Tax Administration (TIGTA) showed the IRS reduced its staff by 11% in just a few months. Over 11,000 employees left, many through buyouts, but many others were let go during their probationary periods.

The "Patriot" Surge and the Hiring Freeze

Then came January 20, 2025. A government-wide hiring freeze was implemented. For many IRS PwC accounting layoffs applicants, this was the final door slamming shut. Graduate students who had accepted offers to work in the Office of Chief Counsel saw those offers rescinded.

The focus shifted.

👉 See also: The Big Buydown Bet: Why Homebuyers Are Gambling on Temporary Rates

Instead of hiring thousands of tax auditors, the new mandate focused heavily on enforcement in other areas. Agencies like ICE reported a "historic 120% manpower increase," hiring 12,000 agents in record time, while the IRS was left to figure out how to operate with a "personnel gap" that former Commissioner Charles Rettig warned would be a "tough sell" to fix later.

Why Applicants are Feeling the Squeeze

So, if you’re an applicant right now, you’re probably looking at this and thinking, "Is accounting even a good career anymore?"

The answer is a frustrating "yes, but."

The demand for CPAs is still technically high. The U.S. Bureau of Labor Statistics still projects growth. But the type of demand has changed. Firms don't want "box-checkers" anymore. They want people who can act as "strategic advisors."

The Skills Gap Paradox

- Technology is no longer optional: If you aren't comfortable with advanced data analytics or internal AI tools like "ChatPwC," you’re going to struggle.

- The 150-hour rule is under fire: States like Minnesota and others have been pushing to lower the credit requirement for CPAs because the talent pipeline is drying up.

- Contracting is king: Robert Half reported that about 70% of finance leaders are increasing their use of contract talent. Firms want flexibility. They don't want to be stuck with "low attrition" problems again.

What Most People Get Wrong About These Layoffs

A lot of people think these layoffs mean there's no money in accounting. That’s wrong. Revenue for firms like Deloitte and EY actually grew in 2025.

The problem isn't a lack of money; it's a shift in where that money goes. PwC's revenue hit $56.9 billion in fiscal 2025, but the growth rate was slowing. When growth slows from 10% to 3%, partners start looking for ways to "optimize." Usually, that means cutting the most expensive line item: people.

✨ Don't miss: Business Model Canvas Explained: Why Your Strategic Plan is Probably Too Long

Actionable Steps for Displaced Applicants

If you were caught in the crossfire of the IRS cuts or the PwC "recalibration," sitting around and waiting for the "old" job market to come back is a bad move. It’s not coming back.

1. Pivot to "Specialized" Mid-Market Firms

While the Big Four are busy "reinventing" themselves with AI, many mid-tier firms are desperate for talent and aren't subject to the same "up or out" volatility. They often offer better work-life balance and more job security.

2. Lean Into the "Strategic Advisor" Role

Update your resume to focus on interpretation, not just preparation. If you can explain why the numbers look the way they do to a client who doesn't speak "accounting," you are ten times more valuable than a staffer who just runs reports.

3. Explore Federal Roles Outside the IRS

The hiring freeze didn't hit every corner of the government equally. Agencies involved in infrastructure, energy, and defense still need forensic accountants and auditors.

4. Get Comfortable with the "Fractional" Model

The rise of contract and "fractional" accounting roles means you might not have one 40-year career at a single firm. You might have five different "gigs" at once. It’s a different way to live, but the pay can actually be higher if you’re good at managing your own time.

The reality for IRS PwC accounting layoffs applicants is that the industry is in a painful transition period. We are moving from a labor-heavy model to a tech-heavy one. It’s messy, it’s unfair to many who did everything "right," and it’s certainly not the stable path it was promised to be. But for those who can bridge the gap between traditional tax/audit knowledge and the new world of AI-driven strategy, the opportunities are still there. They just look a lot different than they did five years ago.

To move forward, start by auditing your own tech stack. If you haven't mastered data visualization tools or learned how to prompt an LLM for tax research, that should be your priority this weekend. The firms may be "recalibrating," and you should be too.

Next Steps for Your Career:

- Identify three mid-market firms in your region that haven't announced layoffs in the last 12 months.

- Update your LinkedIn profile to highlight "AI-Assisted Auditing" or "Data Analytics for Tax" to catch the eye of 2026 recruiters.

- Check the latest USAJobs postings for "Financial Auditor" roles in non-Treasury departments to bypass the current IRS-specific volatility.