You’ve felt it at the checkout counter. That weird, lingering sting that doesn't quite go away. Even when the news anchors talk about "cooling" trends, your grocery bill seems to have its own ideas. Honestly, tracking inflation since january 2025 has been a bit of a rollercoaster, and not the fun kind. It’s been a year of "sticky" prices, weird supply chain hiccups, and a Federal Reserve that’s basically been playing a high-stakes game of chicken with interest rates.

Let's get real.

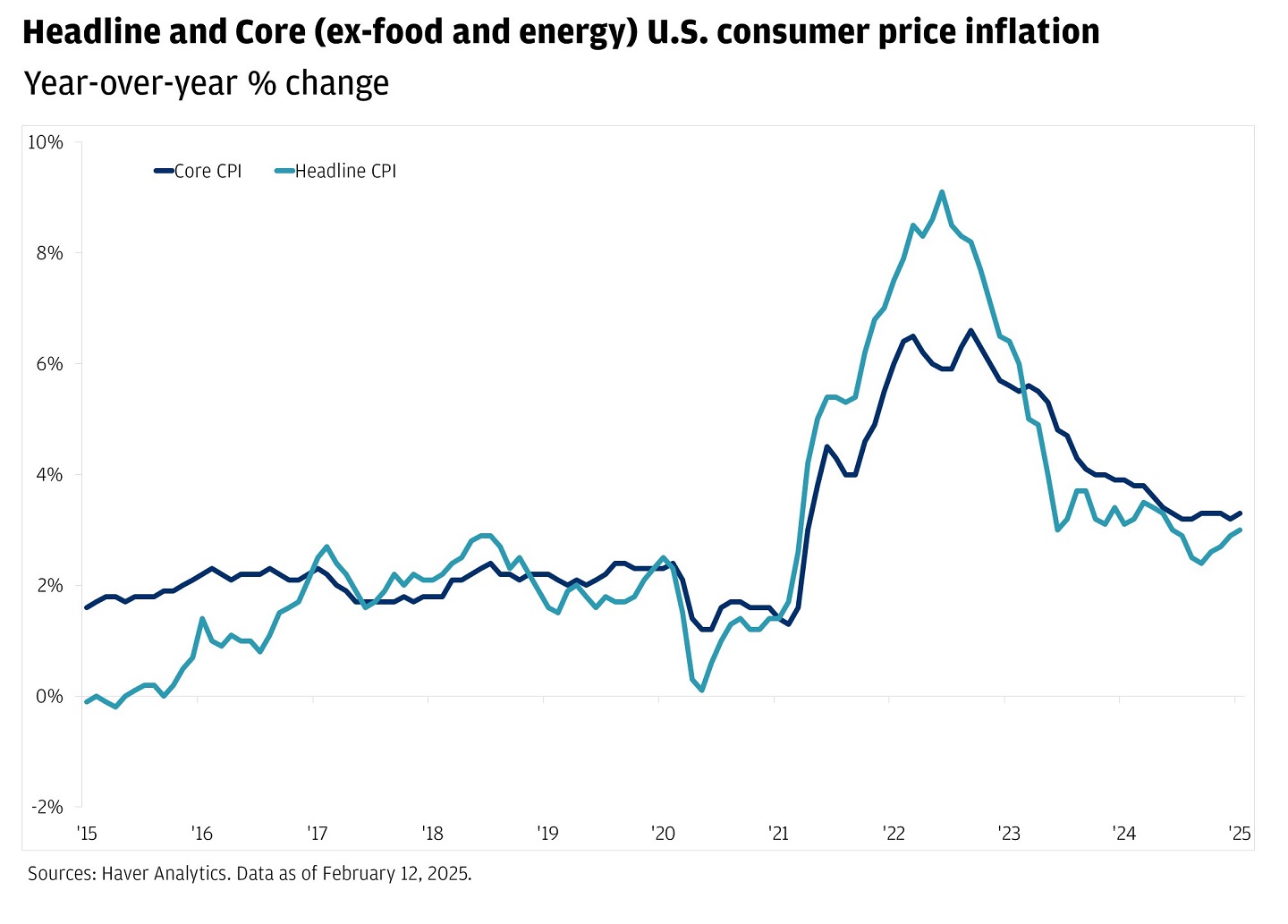

When 2025 kicked off, the vibe was cautiously optimistic. We thought we were out of the woods. Then January 2025 hit us with a 0.5% month-over-month jump in the Consumer Price Index (CPI). It was a wake-up call. Suddenly, everyone was talking about "residual seasonality" and firms hiking prices just because the calendar flipped.

The 2025 Pivot: Why Prices Didn't Just Drop

Most people expected a straight line down to that magical 2% target the Fed loves so much. It didn't happen. Instead, we got what economists call "sticky inflation."

Shelter was the biggest culprit. Even though the housing market felt like it was in a deep freeze for a while, rental prices and "owners' equivalent rent" stayed stubbornly high. By mid-2025, shelter alone was driving nearly a third of the total inflation increase. You can thank a massive shortage of single-family homes for that. If people can't buy, they rent. If they rent, prices go up. It’s a simple, annoying circle.

Then there were the "egg-streme" outliers. Remember the avian flu comeback early in the year? Egg prices shot up over 15% in a single month back in January 2025. It’s those tiny, specific shocks that kept the headline numbers looking messy even when other things, like used cars, were finally getting cheaper.

🔗 Read more: Are Banks Open Today? What Most People Get Wrong About January 15

The Tariff Factor

We have to talk about the elephant in the room: trade policy. Around April 2025, the buzz about new tariffs started hitting the markets. Businesses didn't wait for the ink to dry. They started "front-loading" goods, which is just a fancy way of saying they bought a ton of inventory early to avoid future costs.

This created a temporary spike in core goods inflation. By the time we hit the summer of 2025, we saw:

- Car insurance premiums jumping as repair costs stayed high.

- Electricity bills climbing—up nearly 7% year-over-year by December.

- Dining out becoming a true luxury, with full-service meal prices rising close to 5%.

Where We Stand in January 2026

Fast forward to right now. The latest data from the Bureau of Labor Statistics for December 2025 shows the annual inflation rate sitting at 2.7%.

It’s better than the 3.4% we saw a year ago, sure. But it’s not "back to normal."

The Fed actually cut rates three times in late 2025—September, October, and December. Why? Because the job market started looking a little shaky. Jerome Powell and the crew decided that preventing a recession was more important than crushing that last 0.7% of inflation. It’s a delicate balance. If they cut too fast, inflation since january 2025 could just come roaring back in 2026.

The Global Perspective

It's not just a "US thing." According to the United Nations’ World Economic Situation and Prospects 2026 report, global inflation is hovering around 3.1% now. That’s down from 4.0% in 2024. We’re seeing a world that is slowly healing, but trade tensions—especially between the US and China—are keeping everyone on edge.

🔗 Read more: www jcp credit card payment: Why Most People Overpay Without Realizing

In the European Union, they're looking at even slower growth because of these trade wars. Basically, everyone is paying more for imported stuff, and that "tariff tax" is getting passed straight to you.

What Most People Get Wrong About This

A lot of folks think that "lower inflation" means prices are going down.

Nope.

That would be deflation, and that’s a whole different nightmare for the economy. Lower inflation just means prices are rising more slowly. The 20% jump in grocery prices we saw over the last few years? That's the new baseline. It sucks, but that’s the reality of the post-2025 economy.

One surprising detail? Medical care. While most things were getting more expensive, medical care commodities actually stayed relatively tame, rising only about 1.5% over the last year. On the flip side, hospital services stayed hot, jumping over 6%. It's a weirdly fragmented landscape.

Actionable Steps for Your Money in 2026

Since we know the Fed is likely to keep rates in the 3.5% to 3.75% range for a bit, you need to adjust your strategy.

1. Audit your "Fixed" Costs

Electricity and natural gas prices have been wild. If you're in a deregulated state, now is the time to shop for a fixed-rate energy contract before summer hits. Natural gas jumped over 10% in the last 12 months—don't get caught off guard.

2. Rethink Your Cash Strategy

High-yield savings accounts are still paying decent rates, but as the Fed continues to cut, those APYs will drop. If you have extra cash, consider locking in a 1-year CD now while you can still get something near 4%.

📖 Related: Why 1095 Avenue of the Americas Still Dominates the Bryant Park Skyline

3. Watch the "Core" Trends

Ignore the headline number for a second. Look at "Core CPI" (which excludes food and energy). It’s currently at 2.6%. If this number starts creeping back up toward 3%, expect the Fed to stop the rate cuts. That means your mortgage or car loan isn't getting cheaper anytime soon.

4. Bulk Buy Non-Perishables

With tariff uncertainty lingering into the first half of 2026, non-perishable goods (electronics, household supplies, clothes) might see another price bump. If you know you need a new laptop or a set of tires, buying sooner rather than later might actually save you that 3-5% "tariff creep."

The bottom line? We've survived the worst of the 2025 volatility. The "inflation since january 2025" story is finally moving into a chapter of stabilization, even if your wallet still feels a little light. Keep an eye on the January 27-28 Fed meeting. That will set the tone for the rest of your year.