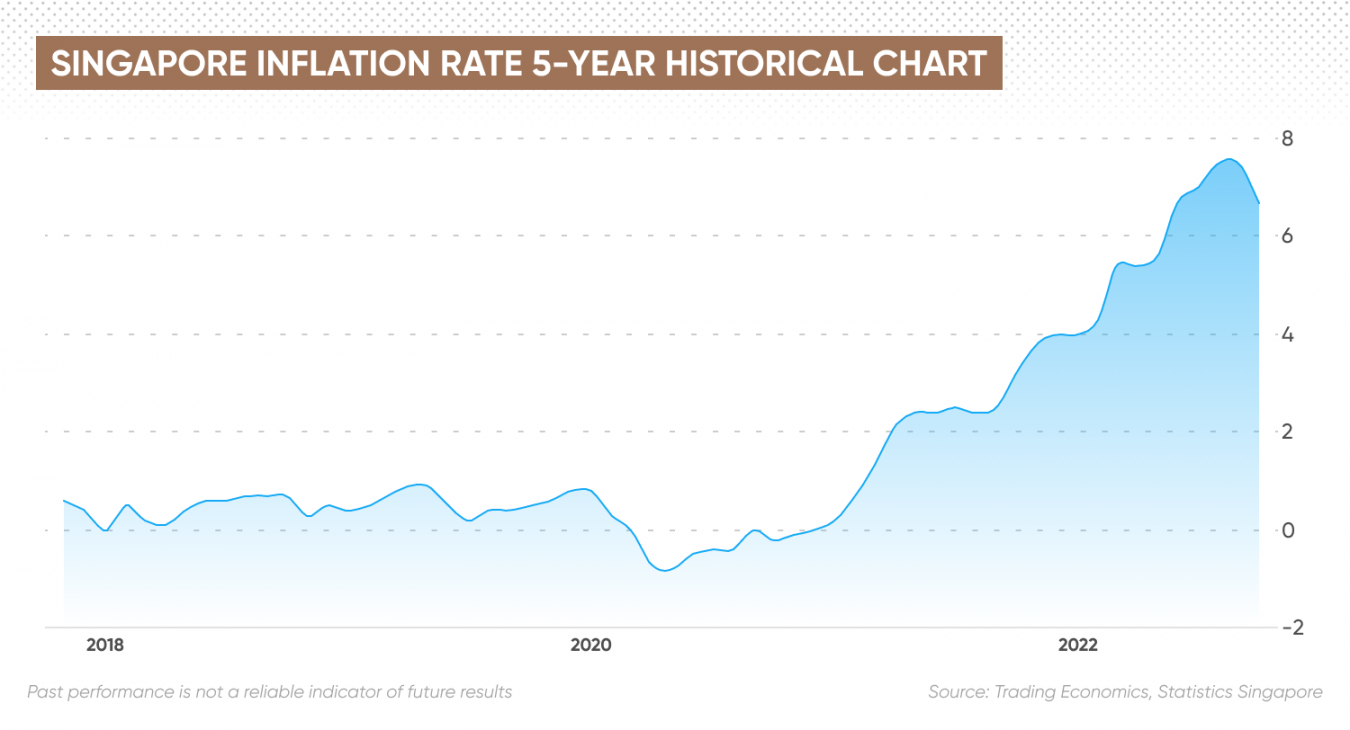

Honestly, walking into a grocery store right now feels like a combat sport. You’ve probably noticed it. You grab a carton of eggs, maybe some bread, and a gallon of milk, and suddenly you’re out forty bucks. It’s wild. The official numbers say the inflation rate this year is sitting at 2.7%, but if you ask anyone actually paying bills, that number feels like a flat-out lie.

How can the Bureau of Labor Statistics (BLS) claim prices only went up a tiny bit when your rent just jumped another hundred dollars?

Well, the December 2025 data—which basically sets the stage for the inflation rate this year—shows a weirdly stubborn economy. Headline CPI stayed flat at 2.7% for the 12 months ending in December. That’s the same as November. It sounds stable, right? But the "under the hood" details are messy.

💡 You might also like: Mark Hall and Monster Energy: The Story of the Man Who Actually Unleashed the Beast

The Inflation Rate This Year: What the Fed is Actually Watching

The Federal Reserve is in a tough spot. Jerome Powell and the rest of the FOMC spent most of last year cutting rates—three times, actually—bringing the federal funds rate down to a range of 3.5% to 3.75%. They were trying to stick a "soft landing," where inflation dies down without the whole job market imploding.

But here’s the kicker.

Core inflation, which ignores the roller-coaster prices of food and gas, is currently at 2.6%. That is technically the lowest it’s been since early 2021. However, the Fed’s "North Star" is 2%. We aren't there. And because we aren't there, the experts at places like J.P. Morgan and Goldman Sachs are split on what happens next. Goldman's David Mericle thinks we might see inflation drop toward 2.1% by December 2026 as the "tariff drag" fades and tax cuts from the One Big Beautiful Bill Act kick in.

Others aren't so sure.

The 43-day government shutdown late last year totally nuked the data collection for October 2025. It created a massive blind spot. When the BLS can't walk into stores to check prices, they have to estimate. Economists at RSM US have pointed out that the lack of October data makes current trends super hard to read. We're basically flying a plane with a cracked windshield.

Why Your Wallet Still Hurts

If the inflation rate this year is supposedly "cooling," why does everything still feel so pricey? It’s because of something called "price levels" versus "inflation rates."

Inflation is the speed at which prices rise. Just because the speed slows down doesn't mean the prices go back to where they were in 2019. They’re just climbing more slowly now.

- Shelter is the biggest villain. It rose 3.2% over the last year. Since housing makes up more than a third of the CPI, it’s dragging the whole average up.

- Food is a mixed bag. Eating at home went up 2.4%, but if you want to grab a burger at a restaurant (food away from home), you're looking at a 4.1% jump.

- Energy is weirdly okay. Gasoline prices actually dropped 3.4% recently, which is the only thing keeping the headline number from spiraling.

- Medical care is creeping up at 3.5%, which is a slow-burn disaster for anyone on a fixed income.

The "shelter" problem is particularly annoying. The way the government calculates "Owners' Equivalent Rent" is famously laggy. It doesn't reflect the "right now" of the housing market. Real-time data from Zillow often shows a different story than the BLS reports.

What to Expect for the Rest of 2026

So, what’s the move for the inflation rate this year? Most forecasters are betting on a "wait and see" approach from the Fed. The Cleveland Fed’s "nowcasting" model suggests that January 2026 might see a slight dip in year-over-year numbers, maybe down to 2.34%.

But don't get too excited.

There are massive "crosswinds," as the folks at Investopedia put it. You’ve got the impact of high tariffs, which usually get passed directly to consumers. Then there’s the labor market. If immigration crackdowns continue, industries like construction and hospitality might see wage spikes. While higher wages sound great, businesses usually cover those costs by—you guessed it—raising prices.

It's a cycle.

Actionable Insights for Your Money

Since we know the inflation rate this year is likely to hover above that 2% target, you can't just sit on your hands.

Watch the "Core" Number, Not Just the Headline. When you see news reports, look for "Core CPI." If that stays above 2.5%, interest rates probably won't drop much further. This means your high-yield savings account is still your best friend, but your mortgage refi dreams might stay on ice for a while.

Audit Your Recurring Services. Services inflation is stickier than goods inflation. Check your streaming subs, insurance premiums, and gym memberships. These "invisible" price hikes in the services sector (up 3.3% recently) are the silent killers of a monthly budget.

Timing the Market. If you’re looking to buy a car, used prices are actually softening—down 1.1% in the latest monthly report. New vehicles are basically flat. It’s one of the few areas where the consumer actually has a tiny bit of leverage right now.

Hedge with Real Assets. Gold and silver have been hitting record highs for a reason. Investors are nervous that the "soft landing" might turn into "sticky inflation." You don't need to be a doomsday prepper, but having some diversified exposure outside of just cash or tech stocks is a smart play when the BLS data is this messy.

The bottom line? The inflation rate this year is a story of two economies. On paper, things are "stabilizing." In reality, the cost of living in 2026 is a grind that requires more strategy than ever before. We’re waiting on the February 11th release of the January data to see if the downward trend is real or just a glitch from the shutdown.