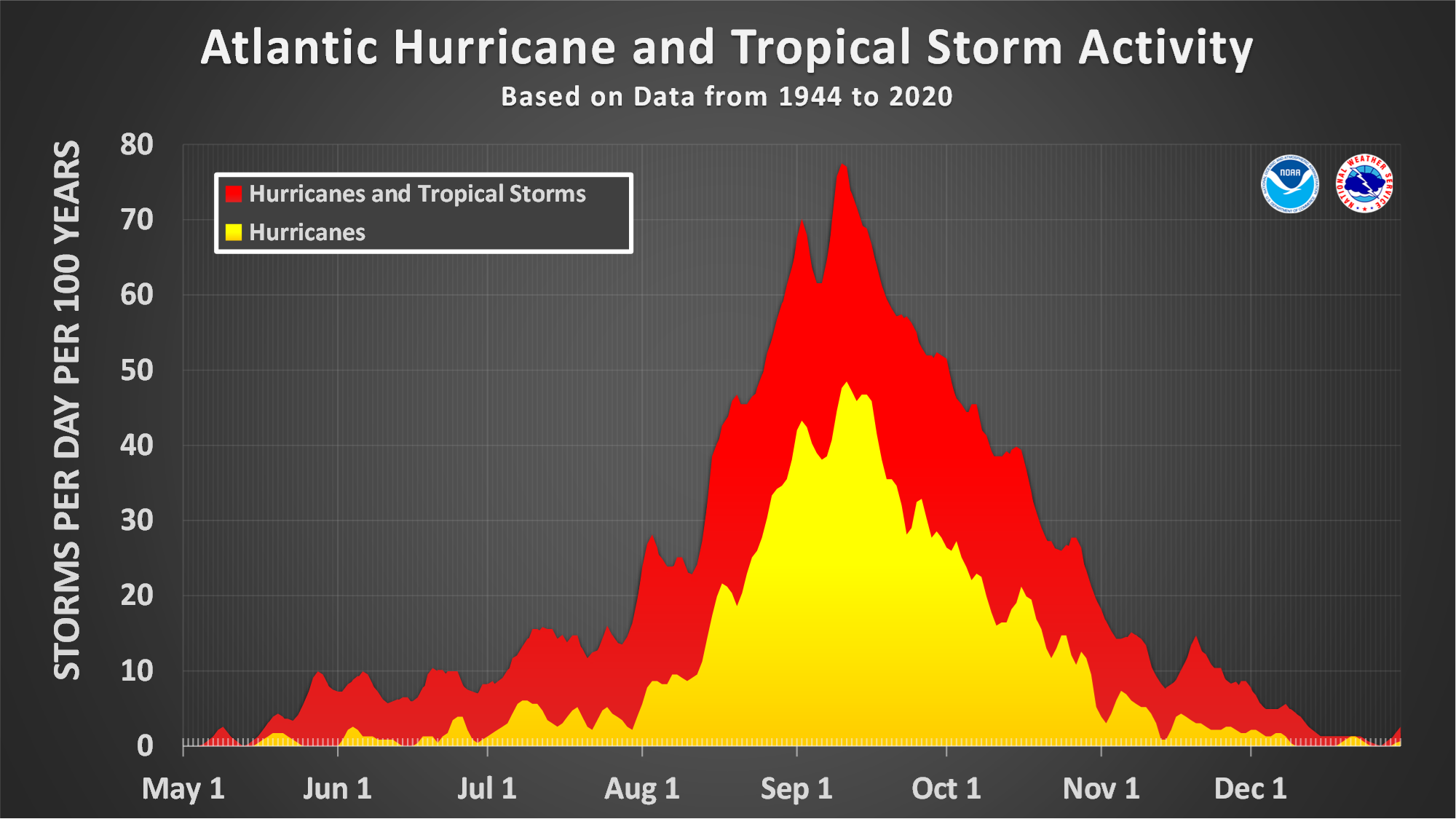

Florida is basically a magnet for big wind. If you live here, you know the drill: the local meteorologist becomes a household deity, you start eyeing the gas lines at Wawa, and suddenly everyone is an expert on the "cone of uncertainty." But honestly, hurricanes in Florida are changing in ways that the old-school playbooks don't always cover. It isn't just about the wind speed anymore.

We've seen it.

The 2024 season was a brutal reminder of that reality when Helene and Milton back-to-back rearranged the Gulf Coast. People who lived miles inland, in zones they thought were "safe," found themselves wading through two feet of tea-colored surge water. It’s scary stuff. But if we’re going to talk about surviving and thriving in the Sunshine State, we have to look past the dramatic news b-roll and get into the actual mechanics of what makes these storms tick lately.

Why the "Category" System is Kinda Flawed

Most people see a Category 2 on the screen and breathe a sigh of relief. That's a mistake. The Saffir-Simpson Scale measures sustained wind speed, which is great for knowing if your roof shingles are going to stay put, but it tells you zero about water. Water is what kills.

Take Hurricane Helene. When it hit the Big Bend as a Category 4, it was devastating, sure. But the real story was the surge it pushed into places like Tampa Bay and Cedar Key—hundreds of miles from the eye. The pressure and the sheer size of the wind field mattered more than the peak gusts at the center. We have to stop obsessing over the number. A "weak" Category 1 that moves at three miles per hour can dump twenty inches of rain and cause more damage than a fast-moving Category 5. Look at Harvey in Texas or Ian in Fort Myers. It's the forward speed and the moisture content that break your bank account.

The National Hurricane Center (NHC) has actually been experimenting with new graphics because they know we're bad at reading the cone. The cone shows where the center of the storm might go, not where the impacts will be. You can be sixty miles outside the cone and still get a tornado that levels your garage. It happens constantly.

💡 You might also like: Obituaries Binghamton New York: Why Finding Local History is Getting Harder

The Insurance Nightmare Nobody Wants to Talk About

If you’re moving here or already own a home, you’ve felt the sting. Property insurance for hurricanes in Florida has become a massive economic hurdle. It’s not just "expensive" anymore; it’s a crisis.

State-backed Citizens Property Insurance Corporation has become the largest insurer in the state because private companies are either fleeing or going belly-up. Why? Because the math doesn't work for them anymore. Between the rising cost of replacement materials—thanks, inflation—and the sheer frequency of billion-dollar disasters, the "risk pool" is more like a puddle.

- Reinsurance rates: Florida's insurers buy their own insurance (reinsurance) on the global market. When those rates go up, your premium hits the ceiling.

- Litigation: For years, Florida accounted for a massive percentage of all homeowners' insurance lawsuits in the U.S. Recent legislative reforms are trying to fix this, but it takes time for those changes to trickle down to your monthly bill.

- The "Flood" Gap: Here is the kicker. Your standard homeowners' policy almost never covers rising water. You need a separate NFIP (National Flood Insurance Program) policy or a private flood rider. If a surge hits your living room and you don't have that specific paper, you’re basically on your own.

The New Reality of Rapid Intensification

We used to have days to prepare. Now? These storms are "bombing out."

Rapid intensification is defined as an increase in maximum sustained winds of at least 35 mph within 24 hours. We saw it with Michael in 2018 and Ian in 2022. The Gulf of Mexico is acting like a battery, charging these storms up right before they make landfall. If you wait until a storm is a "major" to buy water and plywood, you're already too late. The shelves will be empty.

Scientists like Dr. Jeff Masters have pointed out that warmer sea surface temperatures provide more "fuel" for the engine. It's thermodynamics. The hotter the water, the higher the ceiling for how strong a storm can get. It’s not just about more storms; it’s about the ones we do get having a higher chance of becoming monsters overnight.

📖 Related: NYC Subway 6 Train Delay: What Actually Happens Under Lexington Avenue

Real Talk on Evacuation: Run From the Water, Hide From the Wind

This is the golden rule of Florida emergency management. If you are in a storm surge zone—usually labeled A, B, or C—and the local sheriff says go, you go. You don't "wait and see."

Vertical evacuation (going to the second floor) is a gamble that people lost during Hurricane Ian. If the surge is 10 feet and you're in a single-story home, there is nowhere to go. However, if you live in a modern, inland home built after the 2002 Florida Building Code changes, you are likely safer staying put than clogging up I-75.

The traffic during a Florida evacuation is a nightmare. I-95 and the Florida Turnpike turn into parking lots. If you don't have to leave your county, don't. Find a local shelter or a friend’s house on higher ground. Driving five miles inland is often enough to save your life, whereas driving 300 miles north just puts you in the middle of a massive traffic jam with no gas stations and a car full of stressed-out kids and pets.

Modern Construction vs. Old Florida Charm

There is a huge divide in how hurricanes in Florida affect different homes. If your house was built in the 1970s with a flat roof and jalousie windows, you're at high risk. If it was built in 2023 with impact-rated windows, reinforced "hurricane straps" connecting the roof to the walls, and a high-elevation foundation, you're in a much better spot.

The 2002 Florida Building Code is widely considered the gold standard. After Hurricane Andrew leveled Homestead in 1992, the state realized that "good enough" wasn't good enough. Now, every nail and every shingle has to meet specific wind-load requirements. It adds cost to building, but it's the only reason cities like Miami and Fort Lauderdale are still standing.

👉 See also: No Kings Day 2025: What Most People Get Wrong

What You Should Actually Be Doing Right Now

Don't wait for a tropical wave to show up on the satellite imagery. Prep is a lifestyle here, not a weekend project.

- Check your "Elevation Certificate." Find out exactly how many feet your finished floor is above sea level. This number determines if you’re going to get wet.

- The "Two-Week" Rule. Forget the three-day supply kit. After a major hit, infrastructure can be down for fourteen days. You need two weeks of water (one gallon per person per day), non-perishable food, and—most importantly—your medications.

- Digital Backups. Take photos of every room in your house, your appliances, and your electronics. Upload them to the cloud. If you have to file an insurance claim, having a "before" photo of your 65-inch TV is the difference between getting a check and getting a headache.

- Tree Maintenance. Those beautiful overhanging oak branches? They are projectiles. Trim them back every spring before the season starts in June.

- Generator Safety. More people often die from carbon monoxide poisoning after a storm than from the storm itself. Never, ever run a generator in your garage or near an open window. Keep it 20 feet away from the house.

Hurricanes in Florida are an inevitable part of the "paradise tax." You get the beaches, the sunsets, and the no-income tax, but you also get the occasional existential threat from the Atlantic. It’s a trade-off. But by understanding that the danger is usually the water, that the "Category" is only half the story, and that your insurance policy is probably thinner than you think, you can actually manage the risk.

Stay weather-aware, keep your gas tank at least half full from June to November, and always listen to the local guys who know the topography of your specific neighborhood. They know where the streets flood first.

Actionable Next Steps for Florida Residents:

- Download the FEMA App: It provides real-time alerts from the National Weather Service for up to five different locations.

- Locate Your Shut-Offs: Know exactly how to turn off your main water line and gas line. If a storm breaches your home, you don't want a gas leak adding to the chaos.

- Review Your Policy: Call your insurance agent tomorrow and ask specifically: "Do I have 'Replacement Cost Value' or 'Actual Cash Value'?" You want the former. Also, ask about your "Hurricane Deductible," which is usually a percentage of your home's value (2-5%), not a flat dollar amount. Be prepared for that out-of-pocket cost.