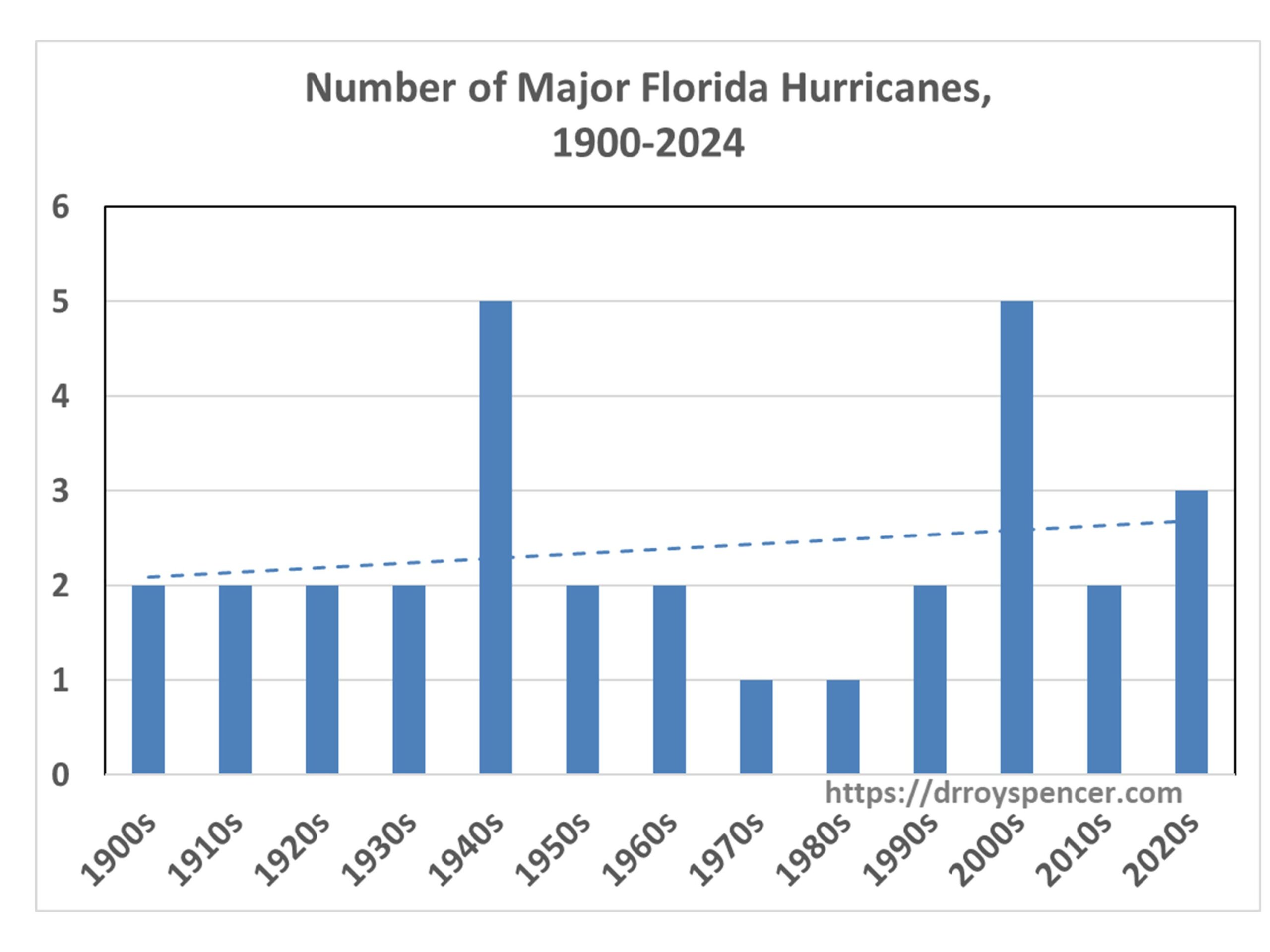

It felt like a bad movie script. People were still pulling sodden drywall out of their living rooms from Hurricane Helene when the news anchors started pointing at a tiny blob in the Gulf of Mexico. That blob became Hurricane Milton. It didn’t just grow; it exploded. Within 24 hours, it went from a Category 1 to a monster Category 5 with winds screaming at 180 mph. If you lived through the hurricane in Florida last year, specifically that brutal stretch in late 2024, you know that "unprecedented" is a word we're all tired of hearing, even if it’s the only one that fits.

Florida got punched twice in two weeks. It’s hard to wrap your head around that kind of back-to-back trauma.

First, Helene stayed offshore but sent a wall of water into the Gulf Coast that many residents hadn't seen in their lifetimes. Then Milton took a "wrong-way" path, cutting across the state from west to east. Everyone expected a quiet season because of Saharan dust or wind shear, but the Gulf of Mexico was basically a tub of hot water. That heat is rocket fuel.

Why the Hurricane in Florida Last Year Caught So Many Off Guard

Most people think they know hurricanes. You stock up on water, buy some batteries, and wait for the wind. But 2024 changed the math. The primary reason the hurricane in Florida last year felt different was the rapid intensification.

Meteorologists like John Morales from NBC 6 in Miami actually got emotional on air while discussing Milton’s pressure drops. It was terrifying to watch. The storm's central pressure fell to 897 millibars. In plain English? That makes it one of the most intense Atlantic hurricanes ever recorded. When a storm strengthens that fast, your evacuation window vanishes. You go to bed thinking it’s a manageable storm and wake up realizing you need to leave now.

The storm surge from Helene was the real killer for the Big Bend and Tampa Bay areas. It wasn't about the wind. It was about the ocean moving into your kitchen. We saw 15-foot surges in some spots. Honestly, the geography of the Florida shelf makes it a funnel for water. Even though Milton eventually weakened to a Category 3 before landfall near Siesta Key, the damage was done because the ground was already saturated. There was nowhere for the water to go.

The Myth of the "Safe" Inland Zone

We need to talk about the tornadoes.

During Milton, the deadliest part of the storm for many wasn't the eye wall on the coast. It was the "dirty side" of the storm hundreds of miles away. St. Lucie County, which is on the Atlantic side, got absolutely hammered by a record-breaking tornado outbreak before the hurricane even made landfall. This wasn't your typical Florida waterspout. We’re talking about massive, multi-vortex tornadoes that leveled a Senior Vitality Center and killed several people.

👉 See also: What Really Happened With the Women's Orchestra of Auschwitz

If you stayed inland thinking you were safe from the "hurricane," the atmosphere had other plans. Florida’s flat terrain offers zero protection when the outer bands start spinning up these monsters.

The Insurance Nightmare Nobody Wants to Face

Let's get real about the money. The hurricane in Florida last year wasn't just a weather event; it was a financial catastrophe that’s still playing out.

If you try to get a quote for homeowners insurance in Florida right now, you might need a drink afterward. After the 2024 season, major carriers like Farmers and AAA had already pulled back or limited coverage. Now, the state-backed "Citizens Property Insurance" is the only option for millions. But here’s the kicker: if Citizens runs out of money, every policyholder in Florida—even those not with Citizens—can be hit with a "hurricane tax" or assessment to cover the gap.

- Flood insurance is separate.

- Standard policies don't cover rising water.

- The 2% hurricane deductible is a massive out-of-pocket hit.

Many folks in the North Port and Sarasota areas found out the hard way that their "comprehensive" policy didn't cover the water that seeped up through the floors.

Science vs. Luck: What the 2024 Data Shows

For a while, it looked like Florida might dodge a bullet. July and August were weirdly quiet. The experts at Colorado State University (CSU), led by Dr. Phil Klotzbach, had predicted an extremely active season, and for a minute, it looked like they might be wrong. Then September hit.

The Sea Surface Temperatures (SSTs) in the Gulf were at record highs. We’re talking 85 to 88 degrees. When Helene and Milton moved over those waters, it was like throwing gasoline on a fire.

The wind shear that usually tears these storms apart was missing. Instead, we had a "high-pressure block" that steered Milton directly into the West Coast. Usually, these storms curve north or stay out at sea. Not this time. This was a direct hit on one of the most densely populated, low-lying areas in the country.

✨ Don't miss: How Much Did Trump Add to the National Debt Explained (Simply)

Recovery Isn't a Linear Process

Driving through Manasota Key or Clearwater Beach months later, you still see the "blue roof" tarp brigade. It’s a slow grind. FEMA assistance helps, but it’s often a drop in the bucket compared to the actual cost of rebuilding.

The psychological toll is also massive. There’s a thing called "hurricane fatigue." When you’ve spent three days boarding up windows, two days in a shelter, and a week without power in 90-degree heat, you start questioning why you live in paradise. We saw a spike in people listing their homes for sale in Pinellas County immediately after Milton.

But then, there’s the "Florida Man" resilience. You see neighbors with chainsaws helping clear roads before the official crews even arrive. It’s a weird mix of trauma and community.

Lessons Learned from the 2024 Florida Hurricane Season

If you’re living in Florida or thinking about moving here, the hurricane in Florida last year offered some hard truths. You can't rely on the "old" rules of thumb.

"I've lived here 30 years and never flooded" is a dangerous sentence. The 2024 season proved that 100-year flood zones are outdated. If you are anywhere near the coast or a drainage canal, you need flood insurance. Period. Even if your mortgage company doesn't require it.

Also, the supply chain for rebuilding is still a mess. Getting a garage door replaced or a roof retiled can take six months.

Actionable Steps for the Next Season

Forget the generic advice. Here is what actually worked for people who survived the 2024 hits with minimal stress.

🔗 Read more: The Galveston Hurricane 1900 Orphanage Story Is More Tragic Than You Realized

Hardened Structures Matter More Than Shutters

If you have the budget, impact-rated windows are a game changer. Not just for the wind, but for the peace of mind. Not having to fumble with heavy metal panels while the wind is picking up is a huge relief. If you can’t do windows, look into "Kevlar" hurricane screens. They are easier to install and incredibly strong.

Power is Everything

A portable generator is fine for a fan and a fridge, but the people who fared best had whole-home standby generators (like Generac) or large-scale battery backups. In the Florida heat, lack of AC after a storm isn't just uncomfortable; for the elderly, it’s a health crisis.

Digital Backups are Life

Don’t just put your papers in a "waterproof" bag. Take photos of every single room in your house—every closet, every drawer—before the storm. Save them to the cloud. When you go to file an insurance claim, having a timestamped photo of your 70-inch TV or your designer sofa makes the process ten times faster.

The "Go Bag" Evolution

Standard kits suggest three days of water. After the hurricane in Florida last year, most experts now suggest ten days. Why? Because bridges get washed out and roads get blocked by debris. You might be on an "island" even if you live miles from the coast.

Moving Forward

Florida isn't going anywhere, but the way we live here has to change. The 2024 season was a wake-up call that the Gulf of Mexico is changing. We are seeing more frequent rapid intensification and more "stall" events where storms sit over an area and dump 30 inches of rain.

The focus now is on "resiliency"—elevating homes, improving drainage basins, and updating building codes. It’s expensive and it takes time. But as the 2024 season showed us, the cost of doing nothing is much, much higher.

Practical Checklist for Residents

- Verify your elevation: Use the FEMA Flood Map Service Center to see your actual risk, not just what your realtor told you.

- Audit your insurance: Call your agent. Ask specifically about "Replacement Cost Value" vs. "Actual Cash Value." If you have the latter, you’re going to get a tiny check for an old roof.

- Tree Maintenance: Do it in the spring. Dead palm fronds and overhanging oak limbs are basically unguided missiles in 100 mph winds.

- The "External" Plan: Know where you will go if a Category 3 or higher is headed your way. Don't wait for the mandatory order; have a hotel booked in Georgia or Alabama two days early. You can always cancel the reservation. You can't always find a room when five million people are on I-75.

The hurricane in Florida last year left a scar on the state, but it also left us with a blueprint for how to handle the next one. We know the water is getting warmer. We know the storms are getting faster. The only variable we can actually control is how ready we are when the next blob appears on the radar.