Water doesn't care about your zip code. When Hurricane Milton tore across the Florida peninsula in October 2024, it proved that hurricane milton flood zones were more than just lines on a FEMA map—they were life-and-death boundaries that shifted in real-time. If you live in Florida, you’ve probably stared at those neon-colored evacuation maps until your eyes crossed. But here’s the thing: most people treat these zones as a "yes or no" question. Am I in the zone, or am I safe?

That’s a dangerous way to look at it.

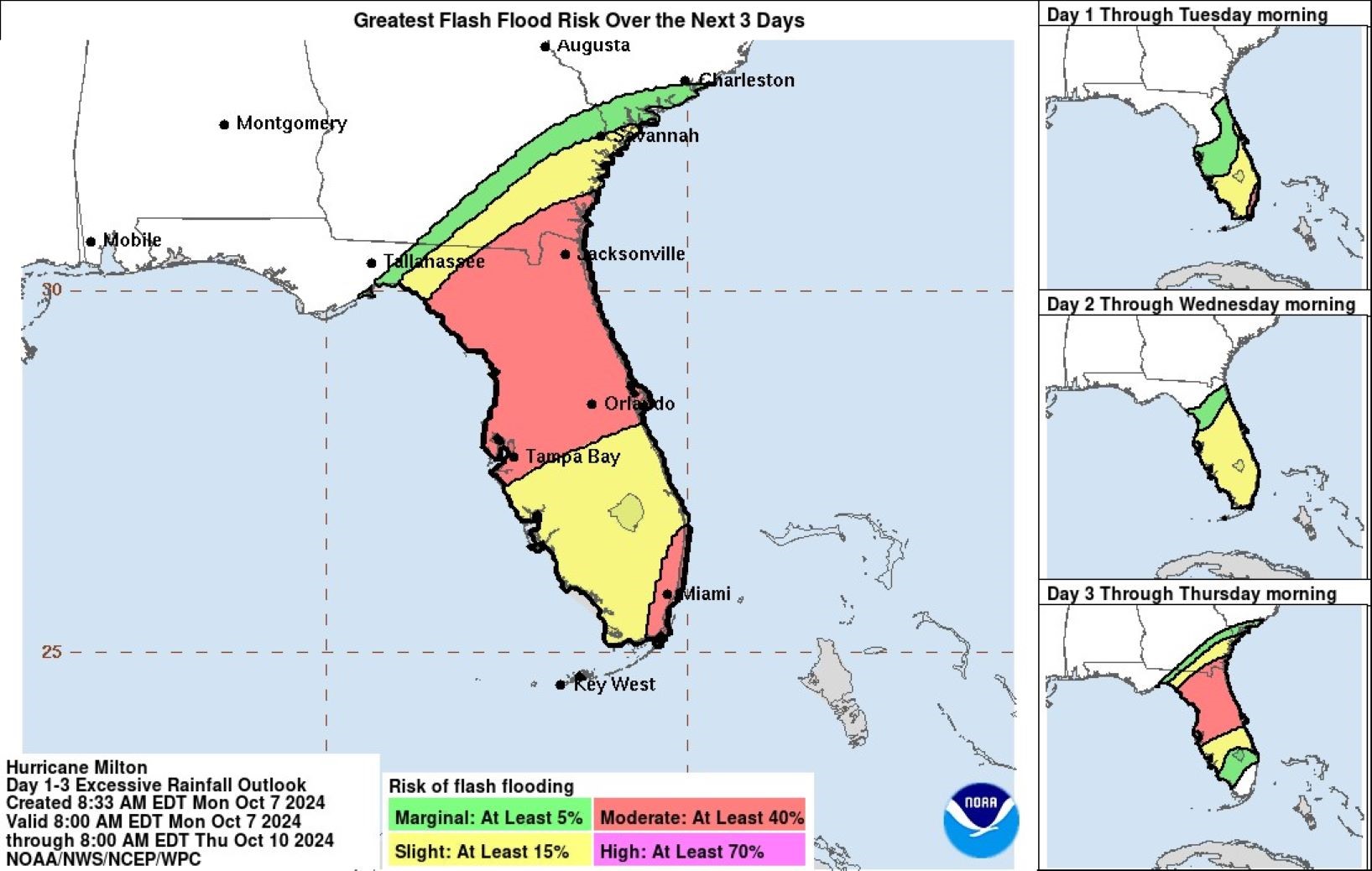

Milton was weird. It wasn't just a coastal surge event; it was a massive "precip" event that dumped over 18 inches of rain in spots like St. Petersburg. This created a dual-threat environment where the official flood zones often failed to predict where the water would actually end up. You had people in Zone X—the "safe" zone—watching water seep through their baseboards because the local drainage systems simply gave up.

Why the Hurricane Milton Flood Zones Shifted So Fast

The physics of Milton were brutal. We’re talking about a storm that underwent rapid intensification into a Category 5 before weakening slightly at landfall near Siesta Key. But the "weakening" was an illusion for those inland. The hurricane milton flood zones in places like Hillsborough and Pinellas counties were hammered by a "reverse surge" in some areas and a catastrophic 1-in-1,000-year rainfall event in others.

Basically, the ground was already saturated.

Think about a sponge. If the sponge is already dripping wet, you can't pour a glass of water on it and expect it to hold anything. Florida’s soil was that sponge. When Milton arrived, the water had nowhere to go but up and into living rooms. This is why we saw record flooding along the Hillsborough River and the Alafia River days after the winds died down. The maps didn't account for the "basin effect" where inland water takes days to migrate toward the Gulf.

The Surge vs. The Soak

Most people focus on the storm surge maps. These are the evacuation zones labeled A through E. In Milton, Zone A saw the expected 5 to 10 feet of surge in spots like Sarasota and Charlotte Isles. But the "soak"—the freshwater flooding—ignored those labels entirely. We saw significant flooding in inland Polk County and even Orlando, areas that usually feel "immune" to the coastal wrath.

It’s honestly scary how many residents stayed put because they weren't in a "flood zone" according to their mortgage paperwork. FEMA’s Special Flood Hazard Areas (SFHAs) are based on historical data. They aren't crystal balls. Milton showed that 21st-century storms are outgrowing 20th-century maps.

✨ Don't miss: The Deportation of Rasha Alawieh: What Really Happened at Boston Logan Airport

The Sarasota and Tampa Bay Reality Check

If you look at the specific hurricane milton flood zones across the I-4 corridor, the damage tells a specific story. In Tampa, the surge wasn't as bad as feared because the storm's track shifted slightly south, actually pulling water out of Tampa Bay for a while. This is called a negative surge. People were literally walking out onto the bay floor.

Don't do that. Ever.

The water comes back. And when it came back for the southern flank of the storm in Venice and Siesta Key, it was relentless. The National Hurricane Center (NHC) had warned of a 10-15 foot surge. While the peak was slightly lower in some residential pockets, the velocity of the water destroyed structures that had survived Ian only two years prior. It was a "stacked" trauma for the coastline.

- Evacuation Zone A: Complete inundation. These are the barrier islands.

- The Inland Creep: Neighborhoods five miles from the coast found themselves underwater because of backed-up storm sewers.

- The Retention Pond Failure: In newer developments around Lakewood Ranch, retention ponds designed for "normal" hurricanes overflowed, turning suburban streets into rivers.

Navigating the FEMA Map Mess Post-Milton

So, how do you actually find your zone now? The maps are being updated, but the process is slow. You need to check the FEMA Flood Map Service Center. But don't just look for your house. Look at the elevation of the "base flood."

If your home sits at 10 feet and the base flood elevation is 9 feet, you’re technically "safe." But Milton brought surges and rain totals that blew past those elevations. It’s a game of inches. Honestly, if you’re anywhere in the Florida peninsula, you’re in a flood zone. It’s just a matter of which one.

Insurance companies are now using Milton’s data to recalibrate premiums. If you’re in a zone that flooded during Milton but isn't technically an "A" or "V" zone, expect your private insurance to get... complicated. FEMA’s National Flood Insurance Program (NFIP) is the fallback, but even that has limits.

What the Experts Are Seeing

Hydrologists like those at the University of South Florida (USF) are studying the "back-bay" flooding from Milton. This is when the Gulf pushes water into the bays, and the rivers (like the Manatee River) try to push rainwater out. They meet in the middle. The result is a "clog" that keeps neighborhoods flooded for a week.

This isn't just bad luck. It’s geography.

If you're looking at property now, you have to ask about the "Milton Line." Where did the water stop on October 10, 2024? That is your new baseline. Forget the 100-year flood labels. Those years are passing by every eighteen months now.

Actionable Steps for Homeowners and Renters

Don't wait for the next "M" named storm to figure this out. The hurricane milton flood zones should be a wake-up call that the old rules are dead. You have to be proactive.

1. Get an Elevation Certificate

Don't rely on the general neighborhood map. Hire a surveyor. Knowing your home’s exact finished floor elevation (FFE) relative to sea level is the only way to know your true risk. If Milton’s surge was 8 feet and your floor is at 7 feet, you need a plan that involves more than just sandbags.

2. Check the "Hidden" Maps

FEMA maps are for insurance. Evacuation maps are for life safety. They are NOT the same thing. Your evacuation zone (A, B, C) is based on storm surge risk, not rainfall. You might be in Flood Zone X (low risk for insurance) but Evacuation Zone B (high risk for surge). Know the difference.

3. Install Smart Vents and Barriers

If you’re in a high-risk zone, look into engineered flood vents. They allow water to flow through a garage or crawlspace so the pressure doesn't blow out your foundation. After Milton, these saved dozens of homes in the Punta Gorda area.

4. Document Everything Now

Take a video of your home’s exterior and interior today. If the water comes back, you need "before" footage for the adjusters. Milton claims are still being processed, and the people who had clear, timestamped evidence are getting paid significantly faster than those who didn't.

5. Review Your "Loss of Use" Coverage

Many people realized too late that while their flood insurance covered the building, it didn't cover the cost of living in a hotel for three months while the mold was remediated. Check your policy. If it’s missing, add it. It’s usually cheap until you actually need it.

Florida is changing. The way we track hurricane milton flood zones has to change with it. The water is moving further inland, staying longer, and hitting harder. Being "out of the zone" on a piece of paper doesn't mean you’re out of the woods. Stay vigilant, watch the rivers as much as the coast, and never trust a dry street during a Florida autumn.

👉 See also: Which hostages will be released first: How the priority list actually works in high-stakes negotiations

The reality of the 2024 season is that "unlikely" is a word we should probably retire from the weather forecast. Milton was a masterclass in why we need to respect the water, no matter what the map says.