Let’s be real. Nobody writes checks anymore—until they have to. Then, suddenly, you’re standing at a landlord’s desk or a contractor’s truck, holding a piece of paper that feels like a relic from the 19th century, trying to remember if you’re supposed to use a decimal point or a fraction. You don't want to mess up. Checks are legal documents. If you scribble or smudge the amount, the bank might just reject the whole thing, leaving you with a late fee and a headache. Honestly, learning how to write a check for 400 dollars is mostly about muscle memory and avoiding the tiny mistakes that trigger fraud alerts.

It happens.

Most people mess up the "Legal Line." That’s the long line in the middle where you write out the words. If the numbers in the little box don’t match the words on that line, the words win. Every time. It’s a banking rule dictated by the Uniform Commercial Code (UCC). If you write "400" in the box but accidentally write "Four thousand" in words, you’ve just created a very expensive problem for yourself.

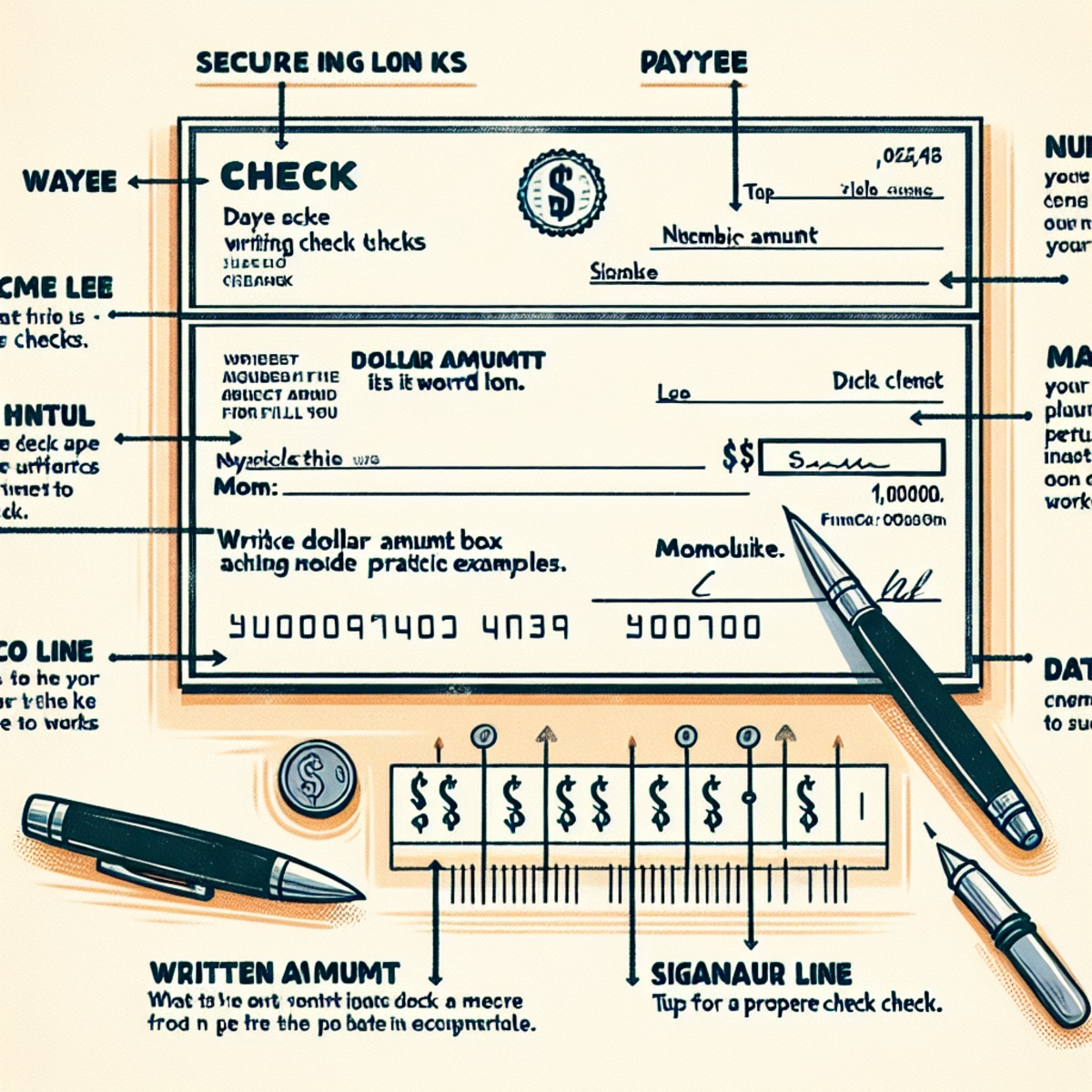

The Basic Anatomy of a Four Hundred Dollar Check

First things first: use a pen. Never, ever use a pencil. It sounds obvious, but people still do it, and it's a fast track to getting your check altered by someone with an eraser and bad intentions. Black or blue ink is the gold standard.

Start with the date in the top right corner. You can use the month-day-year format like January 14, 2026, or just go with 01/14/2026. If you're post-dating the check—meaning you don't want the person to cash it until a specific date—just know that banks often ignore those dates and process them anyway. It's a risky move.

Next is the "Pay to the Order of" line. This is where you put the name of the person or the business. Write it clearly. If you're paying a guy named Mike Smith, write "Mike Smith." Don't just write "Mike." If it’s for a business like "Oakwood Apartments," make sure you have the exact legal name. This prevents the "who is this for?" conversation at the teller window.

Filling in the Numbers

Now we get to the $400.00 part. In the small box on the right side, you want to cram the numbers as far to the left as possible. Why? Because if you leave a gap between the dollar sign and the "4," someone could easily sneak a "1" in there and turn your four hundred dollars into one thousand four hundred dollars.

Write "400.00" clearly. Use a decimal point. Some people like to make the cents smaller, which is fine, but just keep it readable.

The Most Important Part: Writing the Words

This is the "Legal Line." This is where you actually explain how to write a check for 400 dollars in a way the bank can't argue with.

💡 You might also like: Why Pick Your Part Chicago South is Still the Go-To for Used Car Parts

You should write: Four hundred and 00/100.

Notice I didn't say "Four hundred dollars." The word "Dollars" is usually already printed at the very end of the line. If you write "Four hundred dollars dollars," you look like a dork, though the bank will still take it.

The "and" is important. In the world of grammar and finance, "and" signifies the decimal point. If you were writing a check for $400.50, you'd write "Four hundred and 50/100." Since we're doing a flat four hundred, we use "00/100" or even "no/100" to show there are zero cents.

Draw a straight line from the end of your writing to the word "Dollars." This is a security measure. It fills the empty space so nobody can add extra words like "and ninety-nine cents" later on.

Why the Fraction Matters

You might wonder why we use "00/100" instead of just writing "Four Hundred." It’s a clarity thing. Banks process millions of checks using Optical Character Recognition (OCR). The machines are smart, but they like consistency. The fraction "00/100" is a universal signal that the dollar amount is finished and no cents are involved. It’s a legacy habit from the days of hand-processing that just never went away because it works.

The Memo Line and Your Signature

The memo line is optional, but honestly, you should use it. If this $400 is for "January Rent" or "Repairs on the Ford," write that down. It’s not for the bank; it’s for you. When you’re looking at your bank statement three months from now and see a $400 withdrawal, the memo will save you from a minor existential crisis.

Finally, sign it.

The signature must match what the bank has on file. If you’ve changed your signature significantly since you opened the account at age sixteen, you might want to update your signature card at the branch. An unsigned check is just a piece of paper. It’s worthless.

👉 See also: What Is the Rate of Platinum Today: Why Prices Are Smashing Records in 2026

Common Blunders to Avoid

Let's talk about mistakes. We all make them.

If you mess up a word, don't try to scribble over it. Most banks will reject a check with heavy "white-out" or obvious alterations because it looks like a forgery attempt. If you make a mistake, just write "VOID" in big letters across the front of the check and start over with a fresh one. It’s better to waste a ten-cent check than to have a $400 payment bounce or get delayed.

Another thing: watch your balance.

Writing a check for $400 when you only have $380 in your account is a recipe for a $35 overdraft fee. Even if you think you’ll get paid tomorrow, the person you give the check to might drive straight to the bank. Digital check deposits via mobile apps mean that money can leave your account in hours, not days. The "float"—that period where the money stays in your account while the paper travels—is basically dead.

Security Tips for Physical Checks

Checks contain your account number and your routing number. That's a lot of sensitive info. When you're handing over a check for 400 dollars, you're handing over a map to your bank account.

- Don't leave the "Pay to" line blank. This is called a "bearer check." If you lose it, anyone who finds it can write their own name in and cash it.

- Keep your checkbook locked up. Don't leave it in your car or on your desk at work.

- Check your statements. If a check you wrote for $400 shows up as $460 in your transaction history, call the bank immediately.

Is There a Better Way?

Kinda. In 2026, we have Zelle, Venmo, and ACH transfers. But sometimes you just need a paper trail. Small businesses love checks because they don't have to pay the 3% credit card processing fee. For a $400 payment, that’s $12 the business owner gets to keep.

If you're paying a government agency, like the IRS or the DMV, they often prefer checks because their systems are, frankly, ancient. In those cases, the paper check is your best friend because the canceled check image serves as a legal receipt that no one can dispute.

🔗 Read more: Carvana News Today October 2025: Why Most People Get It Wrong

Actionable Steps for Your Next Check

To make sure your $400 payment goes through without a hitch, follow this specific order of operations:

- Verify the funds: Open your banking app and make sure you have at least $400 (plus a buffer) sitting in your checking account.

- Write the recipient first: Fill out the "Pay to the Order of" line before anything else. This prevents the check from becoming a "blank check" if you drop it.

- Use the "00/100" format: On the legal line, write "Four hundred and 00/100" and draw a line to the end.

- Record it: Write the check number, date, and amount in your check register or a notes app.

- Double-check the box: Ensure the "$400.00" is tucked tight against the dollar sign.

Once you’ve signed it, you're done. It feels a bit old-school, but doing it right ensures your money goes where it's supposed to without any extra fees or drama.