Tax season is usually a headache, right? You’re staring at a screen, wondering if you should stick with the old ways or jump into the "New Tax Regime" that the government keeps pushing. If you've been looking for an income tax calculator fy 2024-25, you've probably noticed that things look a bit different this year. Finance Minister Nirmala Sitharaman made some pretty specific tweaks in the July 2024 Union Budget that actually change the math for most salaried employees in India.

It's not just about plugging in your salary anymore.

It's about the strategy. Honestly, most people just wait until March to figure this out, which is a massive mistake. By then, your HR has already deducted the TDS, and you’re left scrambling for insurance policies you don't even need just to save a few bucks. Let’s break down what’s actually happening with your money this financial year.

The Big Shift: New vs. Old Regime in 2024-25

The biggest thing you need to know about the income tax calculator fy 2024-25 is that the New Tax Regime is now the "default." If you don't tell your employer otherwise, they’re going to tax you based on the new slabs.

Is that bad? Not necessarily.

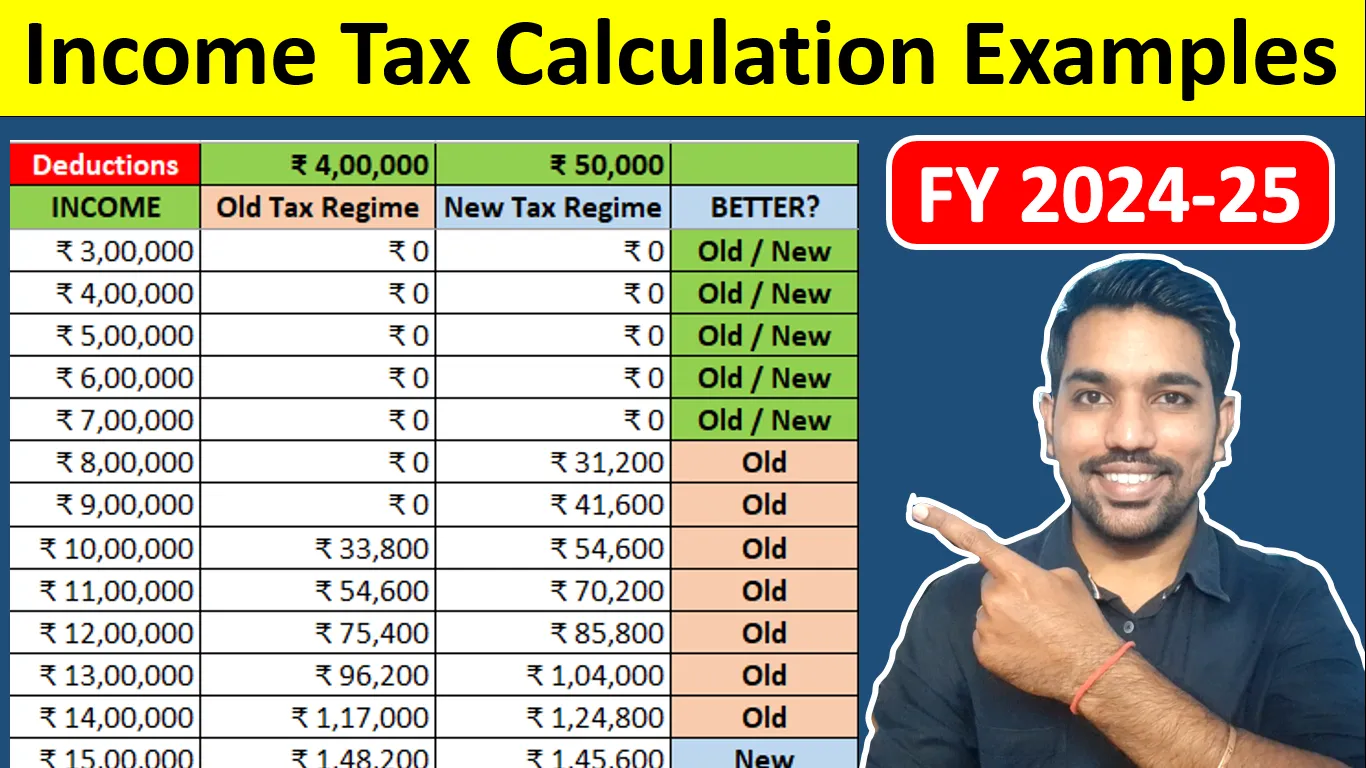

The 2024 Budget actually bumped up the standard deduction for the New Regime from ₹50,000 to ₹75,000. That’s a free pass on an extra twenty-five thousand rupees of your income. On top of that, the tax slabs were stretched out. Now, you don’t hit that 5% bracket until you’re past ₹3 lakh, and the 10% bracket doesn’t kick in until you’re over ₹7 lakh.

But here is the kicker. If you have a massive home loan or you’re dumping ₹1.5 lakh into Section 80C (like PPF or ELSS), the Old Regime might still be your best friend. It’s a tug-of-war. On one side, you have the simplicity of the New Regime—no receipts, no proofs, just lower rates. On the other side, you have the "deduction hunt" of the Old Regime. You’ve gotta run the numbers for both. No exceptions.

Why the Math Changed After the July Budget

You might see some outdated calculators online. Be careful. The interim budget in February was one thing, but the full budget in July 2024 changed the game for the New Tax Regime.

💡 You might also like: Mississippi Taxpayer Access Point: How to Use TAP Without the Headache

Let’s look at the actual slabs for the New Regime for FY 2024-25 (AY 2025-26):

- Up to ₹3,00,000: Nil

- ₹3,00,001 to ₹7,00,000: 5%

- ₹7,00,001 to ₹10,00,000: 10%

- ₹10,00,001 to ₹12,00,000: 15%

- ₹12,00,001 to ₹15,00,000: 20%

- Above ₹15,00,000: 30%

If you’re earning ₹7 lakh or less, you basically pay zero tax under the New Regime because of the Section 87A rebate. It’s a sweet spot. But once you cross that line, even by a little bit, the calculation gets spicy.

The Standard Deduction Surprise

The increase to ₹75,000 for salaried individuals is only for the New Regime. If you stay in the Old Regime, you’re stuck at the old ₹50,000. It feels like the government is gently nudging—okay, maybe shoving—everyone toward the New Regime. Even the family pension deduction went up to ₹25,000. It's clear where the wind is blowing.

Common Mistakes When Using a Tax Calculator

I see this all the time. People open an income tax calculator fy 2024-25, put in their base pay, and call it a day.

Stop.

Your "Gross Salary" isn't what you take home. You have to account for HRA, LTA, and professional tax. If you’re using the Old Regime, you need to be meticulous. Did you include your medical insurance premium under 80D? What about the interest on your savings account under 80TTA? If you miss these, the calculator will give you a "tax due" amount that's way higher than it should be.

Another thing? Surcharge. If you're a high net-worth individual earning over ₹50 lakh, the surcharge kicks in. The New Regime has a capped surcharge of 25% for those earning over ₹5 crore, whereas the Old Regime could potentially sting more. Most of us don't have that problem, but for the top 1%, it’s a huge factor in the calculation.

📖 Related: 60 Pounds to USD: Why the Rate You See Isn't Always the Rate You Get

Real-World Example: The ₹15 Lakh Salary Scuffle

Let’s imagine "Rohan." He earns ₹15 lakh a year.

In the New Regime, with the new ₹75,000 standard deduction, his taxable income is ₹14.25 lakh. Using the income tax calculator fy 2024-25 slabs, his tax comes out to roughly ₹1,05,000 (plus 4% cess).

Now, if Rohan switches to the Old Regime, he can claim ₹1.5 lakh under 80C, ₹50k under NPS (80CCD(1B)), ₹25k for health insurance, and maybe ₹2 lakh for home loan interest. Suddenly, his taxable income drops to around ₹10.25 lakh. But even with all those "investments," he might find the tax amount is surprisingly close to the New Regime's simple calculation.

Is it worth locking up ₹4 lakh in investments just to save ₹5,000 in tax? Probably not. That's the nuance people miss. Liquidity matters.

Marginal Relief: The Savior You Didn't Know You Needed

There’s this weird thing called Marginal Relief. It’s basically a safety net.

Suppose you earn just a few rupees over a tax threshold (like ₹7 lakh in the New Regime). Without marginal relief, earning one extra rupee could technically cost you thousands in tax. The tax department isn't that cruel. The law ensures that the increase in income tax isn't more than the increase in the income itself. If your calculator doesn't show marginal relief, it's not a very good calculator.

How to Handle Capital Gains This Year

This is where it gets messy. The 2024 Budget changed Capital Gains tax too.

👉 See also: Manufacturing Companies CFO Challenges: Why the Old Playbook is Failing

Short-term capital gains (STCG) on listed equity went up to 20%. Long-term capital gains (LTCG) hit 12.5%. While your standard income tax calculator fy 2024-25 usually focuses on salary, you cannot ignore your stock market wins. You get an exemption of ₹1.25 lakh on LTCG now, up from ₹1 lakh.

So, if you sold some stocks to fund a vacation, make sure you factor that in. Your salary tax and your capital gains tax are two different beasts that live in the same house.

Steps to Take Right Now

Don't wait for your company to ask for "Investment Proofs" in January. By then, your monthly take-home pay will drop significantly if you haven't planned.

First, get your latest salary slip. Look at the "Gross" amount. Second, list out your definite investments—the stuff you're already paying, like life insurance or your kid's tuition fees. Third, run those numbers through a reliable income tax calculator fy 2024-25.

Compare the two regimes side-by-side.

If the difference is less than ₹10,000, the New Regime is usually better because you keep your cash. You aren't forced to lock money in a 15-year PPF just to save a tiny bit of tax. If the Old Regime saves you ₹50,000 or more, then start gathering your HRA receipts and rent agreements now.

Check your Form 26AS and AIS (Annual Information Statement) regularly. The Income Tax Department is using AI to track everything from your credit card spends to your foreign trips. If your declared income doesn't match your lifestyle, a calculator will be the least of your worries.

Final Practical Checklist

- Confirm your regime: Decide by mid-year so your TDS is consistent.

- Standard Deduction: Remember it's ₹75,000 for the New Regime for FY 2024-25.

- NPS Advantage: Under the New Regime, employer contribution to NPS is still deductible.

- Review Slabs: The 10% and 15% brackets have shifted; make sure your math reflects the July 2024 update.

- Documentation: Even if the New Regime doesn't require "proofs," keep your records for any high-value transactions.

The goal isn't just to pay the least amount of tax. The goal is to maximize what stays in your pocket without breaking the law or losing access to your own money for decades. Use the calculator as a compass, not a map.