So, you finally ditched the 9-to-5. No more fluorescent lights. No more "per my last email." But then January rolls around—or worse, April—and you realize the terrifying reality of being your own payroll department.

How to pay taxes self employed isn't just one task. It’s a recurring nightmare if you don't have a system. When you're a W-2 employee, the government takes its cut before you even see your paycheck. It’s invisible. Now? You’re the one holding the scissors, and the IRS wants you to cut them a check every few months. It feels personal.

Honestly, most people mess this up the first year. They wait until April 15th to look at their bank account, only to find they owe $12,000 they already spent on a fancy espresso machine and rent. Don't be that person.

The "Sticker Shock" of the Self-Employment Tax

Here is the thing nobody tells you when you're dreaming about freelance life: you pay double the Social Security and Medicare taxes.

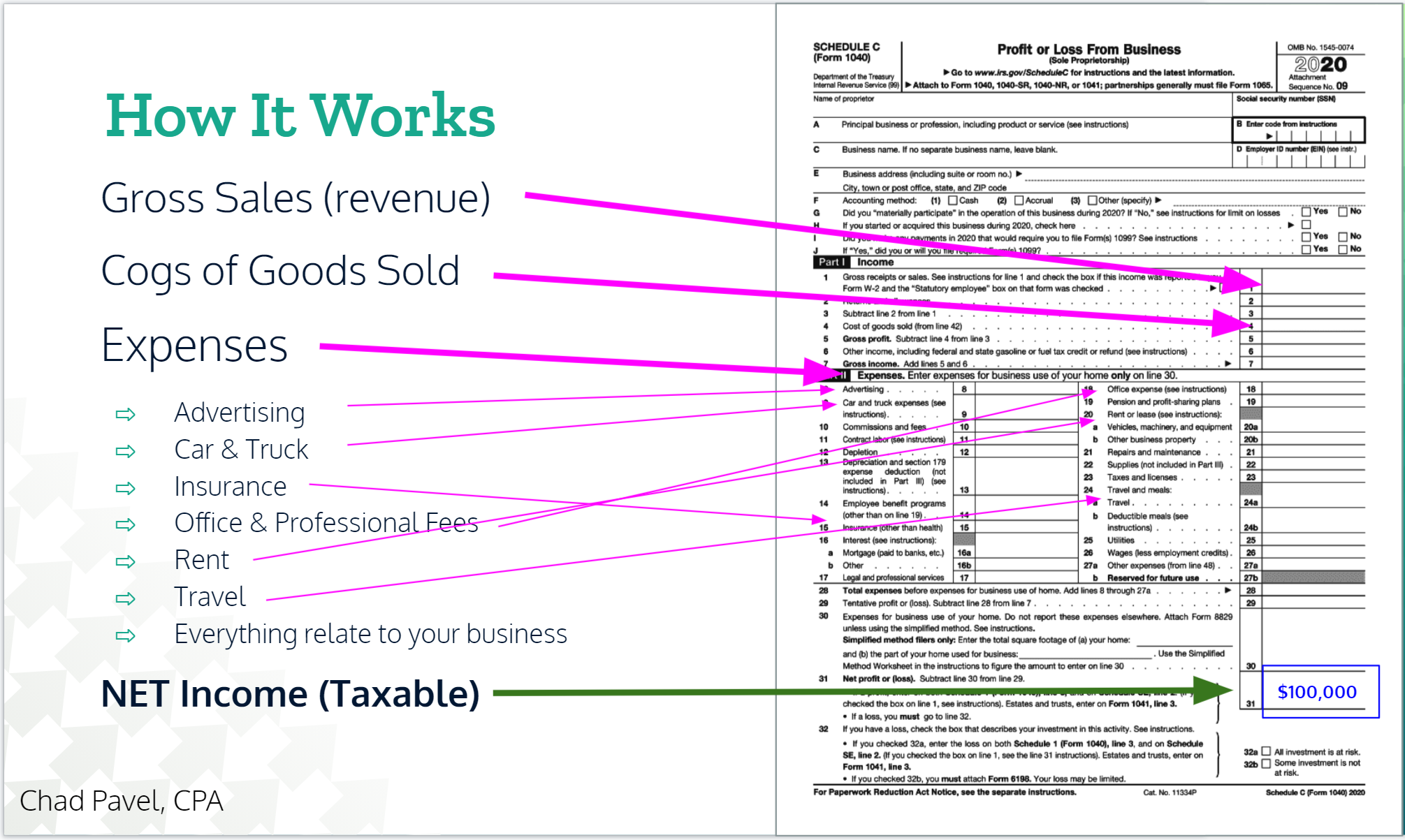

When you work for a boss, you pay 7.65%, and they match that 7.65%. It’s a split. When you are the boss, you’re on the hook for the full 15.3%. This is the Self-Employment Tax (SE tax). You calculate this on Schedule SE.

It’s a gut punch.

But it's not all bad news. You get to deduct the "employer" half of that tax from your gross income when calculating your adjusted gross income (AGI). It helps, but it doesn't take away the sting of writing that check. You also need to keep a close eye on the 1040-ES forms. These are your best friends—or your worst enemies—depending on how organized your spreadsheets are.

Estimated Quarterly Payments: Stop Waiting Until April

If you expect to owe more than $1,000 in taxes, the IRS doesn't want you to wait until the end of the year. They want their money in four installments.

📖 Related: Reading a Crude Oil Barrel Price Chart Without Losing Your Mind

- April 15 (Q1)

- June 15 (Q2)

- September 15 (Q3)

- January 15 (Q4 of the following year)

Notice that June 15th? That’s only two months after the first payment. It’s a trap for the unwary. If you miss these, the IRS will slap you with underpayment penalties. They aren't huge, but it's basically lighting money on fire.

How do you calculate these?

Most people use the "Safe Harbor" rule. Basically, if you pay 100% of what you owed last year (or 110% if your income is high), the IRS won't penalize you, even if you ended up making way more money this year. It’s a shield. Use it.

I’ve seen freelancers use separate high-yield savings accounts just for tax money. Every time a client pays an invoice, they move 25% to 30% into that "do not touch" bucket. It sounds extreme. It is. But it’s the only way to sleep at night.

How to Pay Taxes Self Employed Without Losing Your Mind Over Deductions

The magic word is "deductions."

Every dollar you deduct is a dollar you don't pay taxes on. But the IRS isn't stupid. They define a business expense as something both ordinary and necessary.

A new laptop for a graphic designer? Ordinary. A gold-plated stapler? Probably not.

👉 See also: Is US Stock Market Open Tomorrow? What to Know for the MLK Holiday Weekend

The Home Office Deduction Myth

People are terrified of the home office deduction. They think it’s an automatic audit trigger. While that may have been true in 1995, it’s much more common now. The key is "exclusive use." Your desk in the corner of the living room counts. Your dining room table where you also eat dinner? Techincally, no.

You can use the Simplified Method, which is $5 per square foot up to 300 square feet. It's easy. It's clean. Or you can do the "Actual Expenses" method where you calculate the percentage of your electricity, mortgage interest, and internet that goes toward the office. It’s a headache, but if you live in a high-cost city like San Francisco or New York, it usually saves you more money.

Health Insurance Premiums

This is a big one. If you’re self-employed and paying for your own health insurance, you can often deduct those premiums. This isn't an itemized deduction; it’s an "adjustment to income." That means it lowers your AGI regardless of whether you take the standard deduction or not.

The Paperwork Trail: 1099-NEC vs. 1099-K

You’re going to start seeing these forms hit your mailbox in late January.

The 1099-NEC is what clients send you if they paid you more than $600. The 1099-K is what payment processors like PayPal, Venmo, or Stripe send you.

There has been a lot of back-and-forth lately regarding the threshold for 1099-K reporting. The IRS keeps delaying the $600 threshold, often reverting to the old $20,000/200 transaction limit or a transitional $5,000 limit. Regardless of whether you get a form, you must report the income.

The IRS gets a copy of every 1099 sent to you. If your tax return doesn't match their records, a computer flag goes up. That’s a conversation you don't want to have.

✨ Don't miss: Big Lots in Potsdam NY: What Really Happened to Our Store

Real-World Nuance: The QBI Deduction

The Qualified Business Income (QBI) deduction is a gift from the 2017 Tax Cuts and Jobs Act. It basically lets many self-employed individuals deduct up to 20% of their business income right off the top.

There are income limits. There are phase-outs. If you’re a doctor, lawyer, or "specified service" business, it gets complicated once you hit certain income brackets. But for the average freelancer, it’s a massive win. You’re essentially being taxed on 80% of your profit instead of 100%.

What Most People Get Wrong

They forget about state taxes.

If you live in a state with income tax, like California or Massachusetts, you have to do this whole dance twice. Federal and State. Some states have different rules for estimated payments. Some don't have the same deduction rules as the federal government.

Also, don't forget city taxes. If you’re doing business in Philadelphia or Portland, they might want a piece of the pie too. It’s a lot of layers.

Actionable Next Steps for the Self-Employed

Stop treating your business bank account like a personal piggy bank.

- Open a dedicated business checking account today. Never mix your grocery money with your client payments. It makes the "accounting" part of taxes ten times easier.

- Download a mileage tracker. If you drive for work (not commuting to a regular office, but driving to clients or the post office), those miles are worth over 60 cents each. It adds up to thousands of dollars by December.

- Set a "Tax Date" once a month. Spend 30 minutes looking at your profit and loss. If you made a killing this month, move more money into savings.

- Use software. Whether it's QuickBooks, FreshBooks, or a simple spreadsheet, manual entry is where errors happen.

- Hire a CPA for a "Strategy Session." You don't necessarily need them to file your return, but paying for one hour of their time in October can save you five times that amount in April by finding deductions you missed.

The goal isn't just to pay the IRS. The goal is to pay them exactly what you owe and not a penny more. Being self-employed is hard enough; don't give away your profit because you were too busy to track your receipts. Keep your records, pay your quarterlies, and keep building.