You're sitting there, staring at your screen, and you've got your last paycheck of the year pulled up. You've seen those ads. "Get your max refund!" "Instant tax estimator!" So you start typing numbers into a how much taxes will i get back calculator hoping for a windfall. Maybe it tells you $3,000. You start dreaming of a vacation or finally paying off that credit card. Then, April rolls around, and the reality is a measly $400 check—or worse, a "payment due" notice.

Tax season is basically a giant game of "who keeps the money," and the house usually wins if you don't know the rules.

Most people treat these online calculators like a magic crystal ball. They aren't. Honestly, most of them are just lead-generation tools for big tax software companies. They give you a rough "back of the napkin" guess based on standard deductions, but they often miss the nuance of your actual life. If you've got a side hustle, a kid in daycare, or you traded a bunch of crypto last year, a basic calculator is going to be wrong. Like, wildly wrong.

Why Your How Much Taxes Will I Get Back Calculator Is Probably Wrong

The math behind a tax refund is actually pretty simple on the surface: (Total Tax Owed) minus (Total Tax Already Paid). If that number is negative, you get a refund. Simple, right? Except the IRS code is thousands of pages of "except when" and "unless you qualify for."

Let's talk about the Standard Deduction. For the 2025 tax year (the ones you're likely filing in early 2026), it's $15,000 for singles and $30,000 for married couples filing jointly. Most calculators just bake that in. But what if you’re a teacher who spent $300 of your own money on classroom supplies? Or what if you live in a state like California or New York where your state and local taxes (SALT) might actually make itemizing worth it despite the $10,000 cap?

Most basic web tools don't ask about the "above-the-line" deductions. These are the gold mines. Student loan interest? That’s up to $2,500 you can shave off your taxable income without even itemizing. If the how much taxes will i get back calculator you're using doesn't ask for your 1098-E info, it’s already failing you.

The Hidden Trap of the W-4

Your refund is just a 0% interest loan you gave the government. If you get back $5,000, that’s roughly $416 a month you could have had in your paycheck to cover groceries or rent. People love the "windfall" feeling, but from a purely financial standpoint, a big refund means you messed up your withholding.

✨ Don't miss: Cox Tech Support Business Needs: What Actually Happens When the Internet Quits

Since the IRS redesigned the W-4 form a few years ago, the "allowances" system is gone. Now it’s all about dollar amounts. If you didn't update your W-4 when you got a raise or when your spouse started a new job, your calculator estimate is going to be a total fantasy. Two-income households are notoriously difficult for these calculators to predict because the "stacking" of income often pushes a couple into a higher tax bracket than they expected.

The Credits That Actually Change the Game

Deductions are cool because they lower the income you're taxed on. But tax credits? Those are the heavy hitters. A credit reduces your tax bill dollar-for-dollar.

Take the Child Tax Credit (CTC). It’s been a political football lately. For the 2025 tax year, it generally sits at $2,000 per qualifying child. But there's a catch: only a portion of it is "refundable." This means if you owe zero taxes, the government will only send you a check for a specific amount (the "Additional Child Tax Credit"). If your how much taxes will i get back calculator doesn't distinguish between refundable and non-refundable credits, you're looking at a ghost number.

- Earned Income Tax Credit (EITC): This is for lower-to-moderate-income working individuals and couples. It’s huge. It can be worth over $7,000 depending on how many kids you have.

- The "Hidden" Energy Credits: Did you put in a heat pump? Solar panels? New windows? The Inflation Reduction Act (IRA) created some massive credits that are still active. We're talking 30% of the cost of certain home improvements.

- EV Tax Credits: This is where it gets messy. Whether you get that $7,500 depends on where the battery was made and your Adjusted Gross Income (AGI). Most quick calculators just ask "Did you buy an EV?" and add $7,500. Real life is rarely that generous.

Don't Forget the Side Hustle Tax

Did you drive for Uber? Sell stuff on Etsy? If you made more than $600, the platform is sending a 1099-K to the IRS.

Here is what many people miss: you have to pay the "employer" half of Social Security and Medicare taxes. That's the self-employment tax. It’s roughly 15.3%. A generic how much taxes will i get back calculator often forgets that you owe this on top of your regular income tax. You might see a "refund" of $1,000 on a calculator, but once you plug in that $5,000 you made on the side, you suddenly owe $700. It’s a gut punch.

How to Get an Accurate Estimate (The Hard Way)

If you want a number you can actually take to the bank, stop using the 30-second "EZ" calculators. You need to do a "dry run."

🔗 Read more: Canada Tariffs on US Goods Before Trump: What Most People Get Wrong

- Gather your last paystubs. Look for the "Year-to-Date" (YTD) Federal Tax Withheld. This is the only number that matters for the "paid" side of the equation.

- Estimate your AGI. Take your total salary, subtract your 401(k) contributions (if they're traditional, not Roth), and add in any interest from your savings accounts. High-yield savings accounts are actually paying decent interest now, and that's all taxable.

- Check for "Adjustments to Income." Did you put money into a traditional IRA? Did you pay alimony? These come off before you even get to the standard deduction.

- Use the IRS Tax Withholding Estimator. Honestly, if you want the most accurate how much taxes will i get back calculator, use the one on IRS.gov. It’s clunky. It looks like it was designed in 2005. But it uses the actual logic the IRS uses to process your return.

Real World Example: The "Surprise" Tax Bill

Let's look at Sarah. Sarah is a graphic designer making $70,000. She uses a basic online calculator that says she'll get back $1,200.

But Sarah forgot two things. First, she sold some stocks in February to help with a down payment. Those are capital gains. Second, she received a $5,000 bonus in December. Her company withheld tax on that bonus at a flat 22% rate. However, that bonus pushed her total income into a bracket where some of her money is taxed at 24%.

When she finally sits down with a real pro, that $1,200 refund evaporates. She ends up owing $150.

The lesson? A calculator is only as good as the data you give it. If you "forget" your Robinhood account or your gambling winnings from that weekend in Vegas, the calculator isn't the one lying to you—you're lying to yourself.

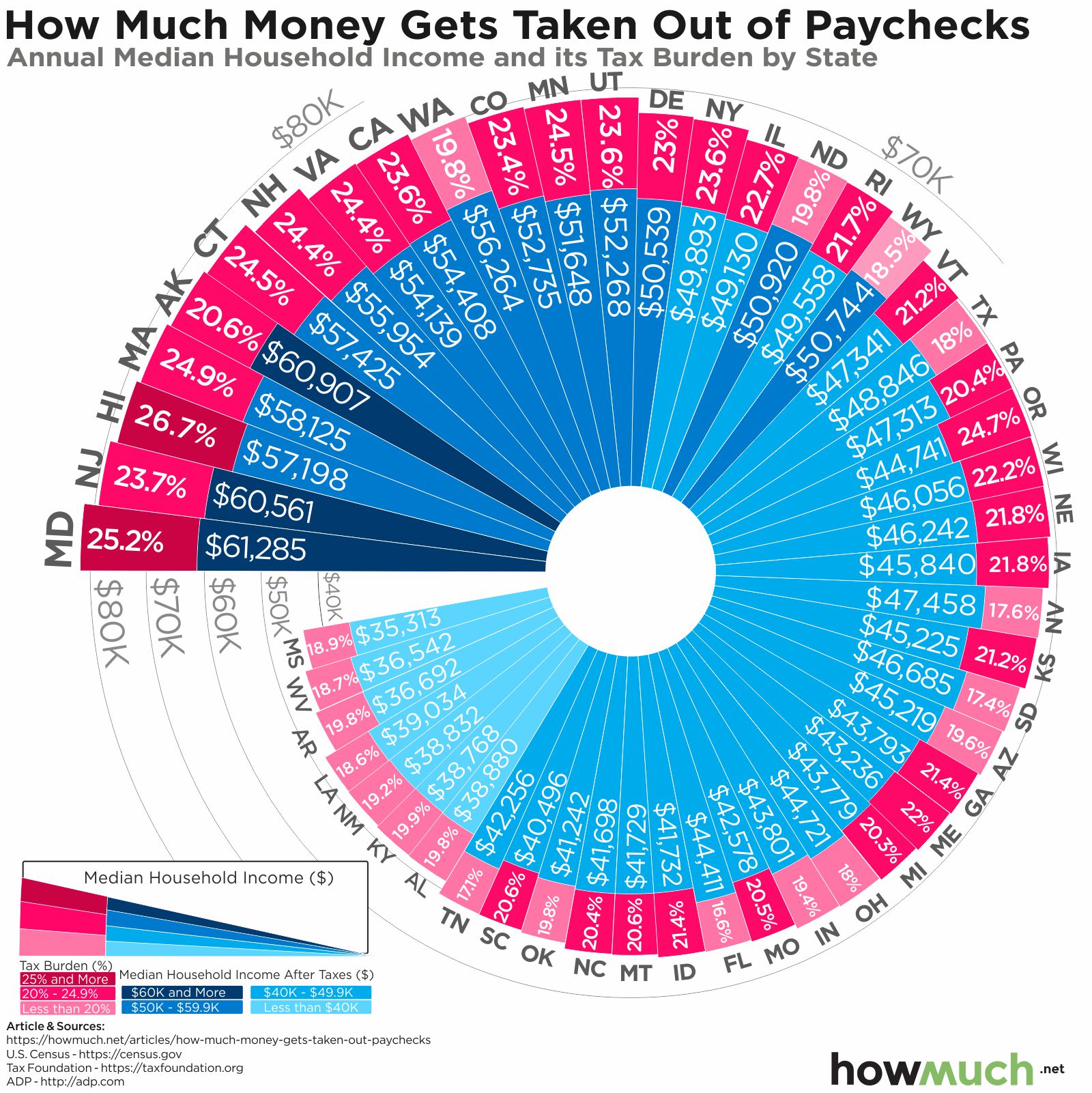

State Taxes: The Forgotten Variable

Most of the time, when people search for a how much taxes will i get back calculator, they’re thinking about the federal government. But unless you live in a state like Florida, Texas, or Washington, you’ve got a state return to deal with too.

State tax laws don't always follow federal laws. Some states don't tax Social Security. Some have their own version of the Earned Income Tax Credit. Some, like Pennsylvania, have a flat tax rate. If your calculator doesn't ask for your zip code, it's only giving you half the story.

💡 You might also like: Bank of America Orland Park IL: What Most People Get Wrong About Local Banking

Moving Forward: Actionable Steps for a Better Refund

Instead of just Refreshing a calculator page, take control of the math.

Review your withholding right now. Don't wait until December. If you're seeing a massive refund estimate, go to your HR portal and decrease your withholding. Get that money in your paycheck every month instead of waiting for the IRS to send it back a year later.

Max out your HSA. If you have a high-deductible health plan, the Health Savings Account is the "triple tax threat." The money goes in tax-free, grows tax-free, and comes out tax-free for medical expenses. If you find out via a calculator that you're going to owe money, you often have until the April filing deadline to contribute to an HSA or a Traditional IRA to lower your previous year's tax bill.

Track your receipts if you're 1099. If you're a freelancer, the how much taxes will i get back calculator is useless without your expense total. Every mile driven, every portion of your internet bill used for work, and every piece of software you bought reduces that "self-employment" tax burden.

Audit your life changes. Did you get married? Have a baby? Buy a house? These aren't just life milestones; they are massive tax triggers. A simple calculator can't capture the nuance of a "mid-year marriage" where two high earners suddenly find themselves in a higher combined bracket.

The bottom line is that the government isn't in the business of giving you money for free. A refund is your own money coming back to you. Use the calculators as a rough guide, but keep a healthy dose of skepticism. The closer you get to a $0 refund—meaning you paid exactly what you owed and not a penny more—the better you’ve managed your finances for the year.

Next Steps to Take:

- Download your most recent paystub and find the YTD Federal Tax Withholding.

- Log into your bank or brokerage and look at the "Tax Documents" or "Year-to-Date Interest" section to see how much "unearned income" you'll need to report.

- Compare your total projected income against the 2025 tax brackets to see if you've crossed a threshold that might change your effective tax rate.

- If the estimate shows you owe money, calculate how much you can contribute to a 401(k) or IRA before December 31st to drop your taxable income.